Solar Panel Recycling Centre Financial Model

This 20-Year, 3-Statement Excel Solar Panel Recycling Centre Financial Model includes revenue streams from the sale of 10 products from your renewable resources centre. Including Glass, Silicon, Aluminum / Aluminium, Copper, Silver, etc, cost structures, and financial statements to forecast the financial health of your recycling centre. User Guide.

Financial Model for a 20 Year Solar Panel Recycling Centre

This very extensive 20 Year Recycling Centre Model involves detailed revenue projections, cost structures, capital expenditures, and financing needs. This model provides a thorough understanding of the financial viability, profitability, and cash flow position of the centre. Including: 20x Income Statements, Cash Flow Statements, Balance Sheets, CAPEX sheets, OPEX Sheets, Statement Summary Sheets, and Revenue Forecasting Charts with the specified revenue streams, BEA charts, sales summary charts, employee salary tabs and expenses sheets. Over 130 Excel Spreadsheets of financial data to monitor.

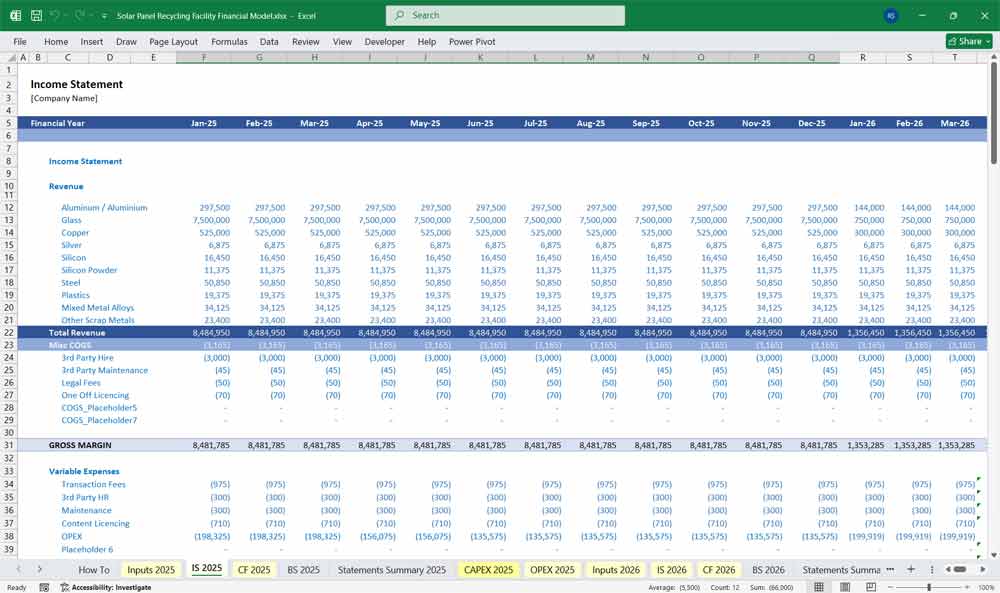

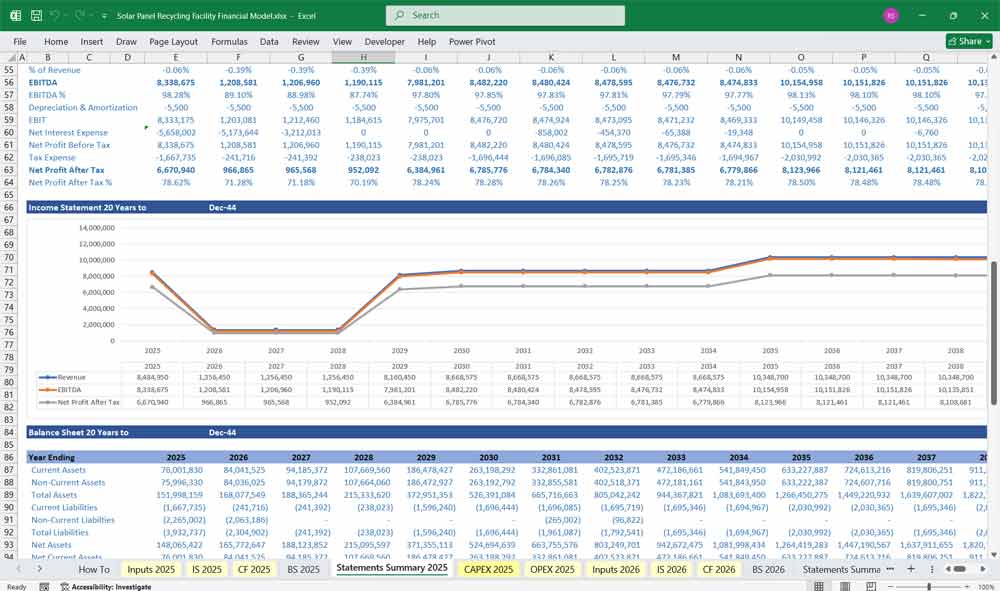

Income Statement (Profit & Loss Statement)

The Income Statement summarizes revenues and expenses to calculate net profit (or loss) over time.

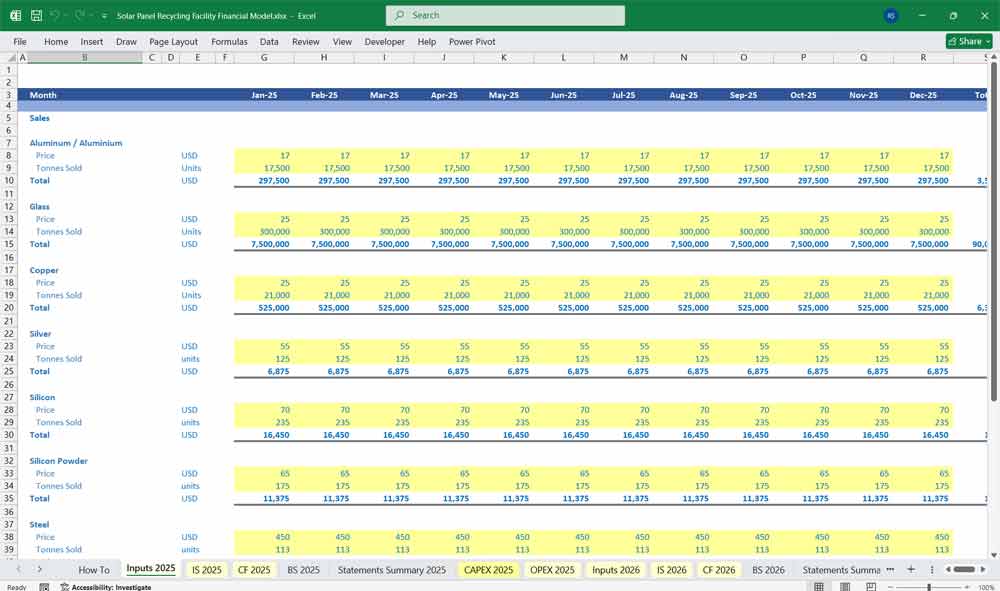

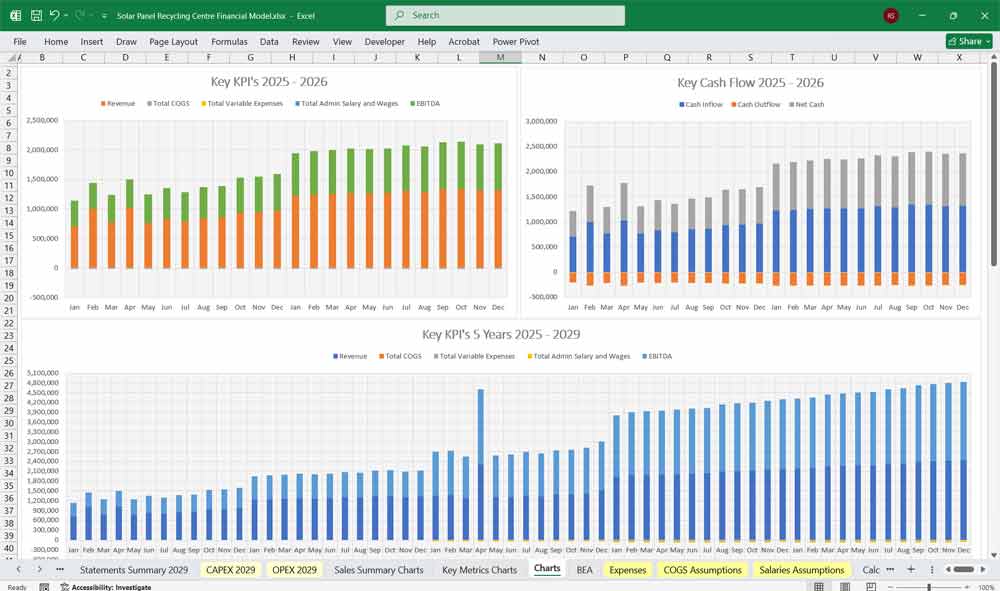

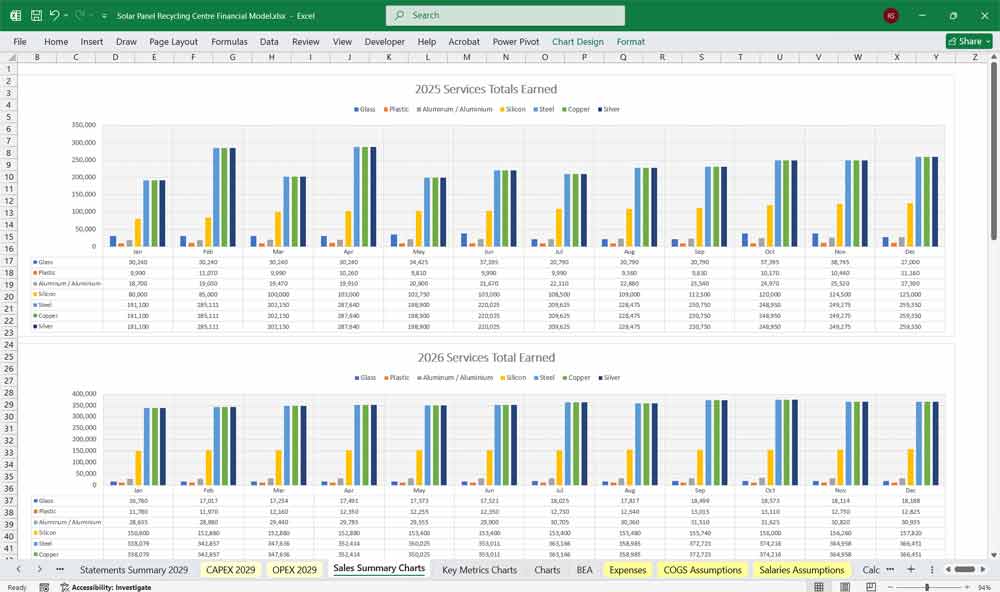

A. Revenue Streams

Recycling Fees (Tipping Fees):

Charged per ton or per panel accepted from solar farms, installers, or manufacturers.

Example: $150 per ton × 5,000 tons per year = $750,000.

Recovered Material Sales:

Glass (~70–80% of panel mass),

Aluminum frames,

Silicon wafers,

Silver, copper, or rare metals.

Example: $1.5M per year initially, increasing with throughput.

Government Incentives / Carbon Credits:

Subsidies or green credits per ton of waste recycled.

Other Revenue:

Consultancy or certification services (e.g., EPR compliance),

Sale of refurbished panels.

Total Revenue = Recycling Fees + Material Sales + Incentives + Other

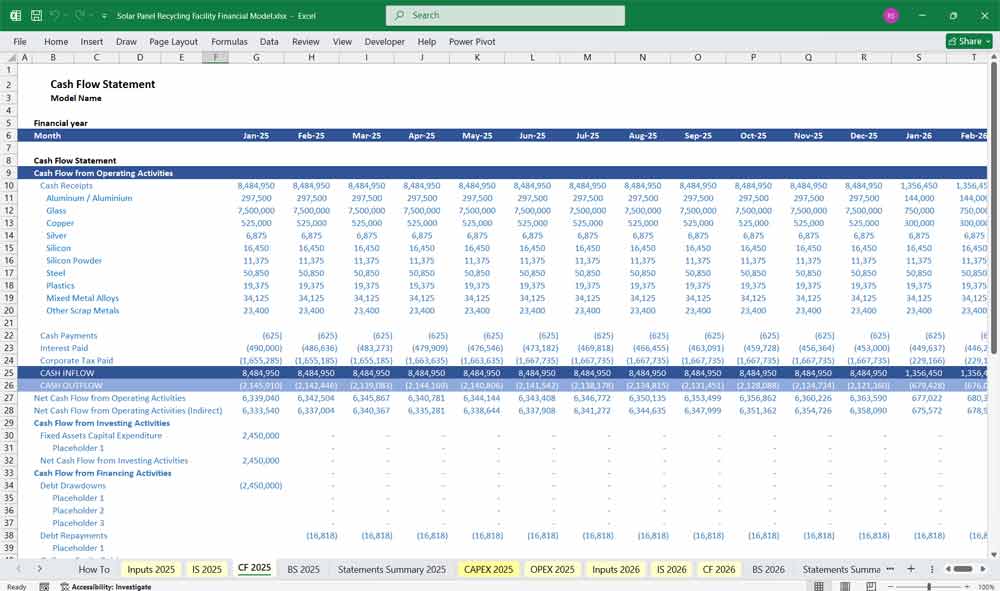

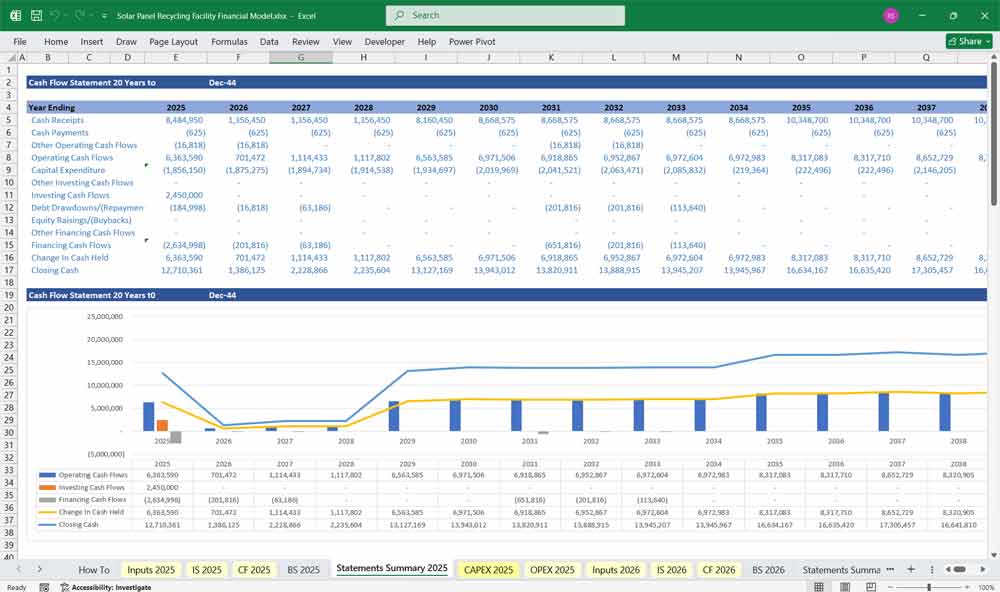

Solar Panel Recycling Centre Cash Flow Statement

The Cash Flow Statement shows how cash moves in and out of the business, divided into Operating, Investing, and Financing activities.

A. Cash Flow from Operating Activities

Inflows:

Cash receipts from recycling fees,

Material sales,

Incentive payments.

Outflows:

Operating expenses (labor, utilities, supplies),

Taxes,

Working capital changes (inventory, receivables, payables).

→ Net Operating Cash Flow = Inflows – Outflows

Cash Flow from Investing Activities

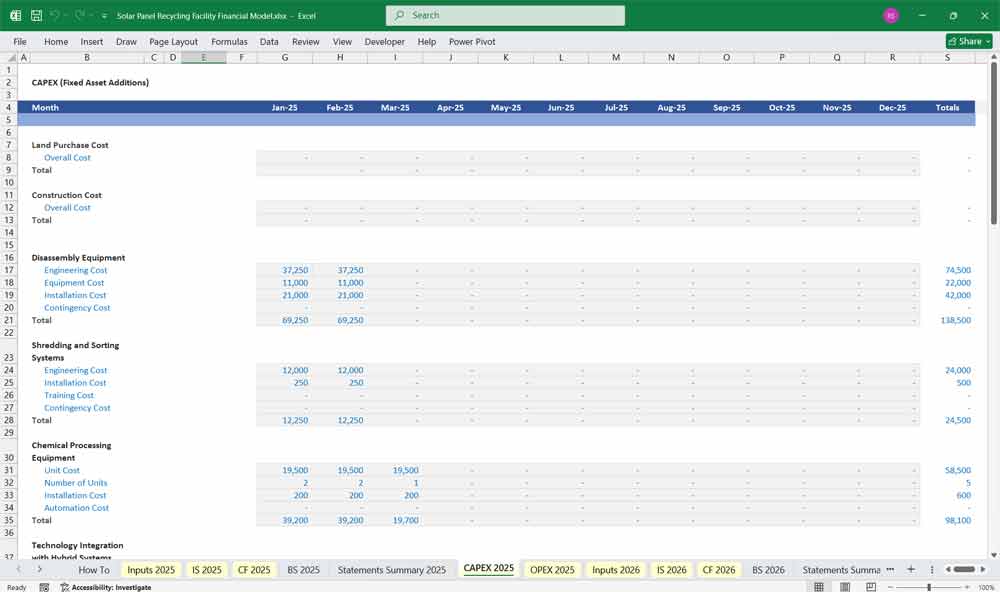

Capital Expenditures (CAPEX):

Land purchase or leasehold improvements,

Facility construction,

Recycling equipment and processing lines,

Vehicles and collection infrastructure,

IT systems and lab testing equipment.

Asset Disposals or Salvage:

Sale of obsolete equipment or land.

→ Typically large outflows in early years (Years 0–2).

Cash Flow from Financing Activities

Inflows:

Equity capital contributions,

Debt drawdowns (bank loans, green bonds, grants).

Outflows:

Loan repayments (principal),

Interest payments,

Dividend distributions.

Cash Position

Net Cash Flow = Operating + Investing + Financing

Closing Cash Balance = Opening Balance + Net Cash Flow

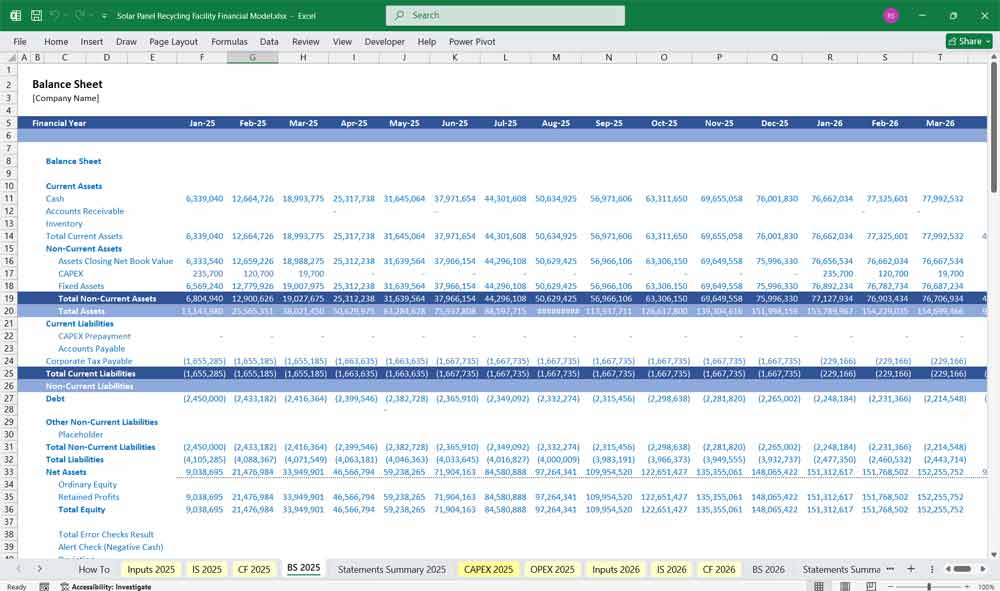

Solar Panel Recycling Centre Balance Sheet

The Balance Sheet provides a snapshot of the Centre’s financial position at a given point — assets, liabilities, and equity.

A. Assets

Current Assets:

Cash & bank balances,

Accounts receivable (clients, governments),

Inventory (recovered materials awaiting sale),

Prepaid expenses.

Non-Current Assets:

Property, plant & equipment (land, buildings, recycling lines, vehicles),

Intangible assets (licenses, patents, recycling process IP),

Accumulated depreciation (contra-asset).

Total Assets = Current + Non-Current Assets

Liabilities

Current Liabilities:

Accounts payable (suppliers, maintenance contracts),

Accrued expenses (utilities, wages),

Short-term debt and interest payable.

Long-Term Liabilities:

Long-term loans or bonds,

Lease obligations,

Decommissioning/reserve funds (for facility closure and environmental compliance).

Total Liabilities = Current + Long-Term Liabilities

Equity

Share Capital: Paid-in equity by founders or investors.

Retained Earnings: Accumulated profits reinvested.

Reserves: For maintenance, environmental obligations, or R&D.

Equity = Assets – Liabilities

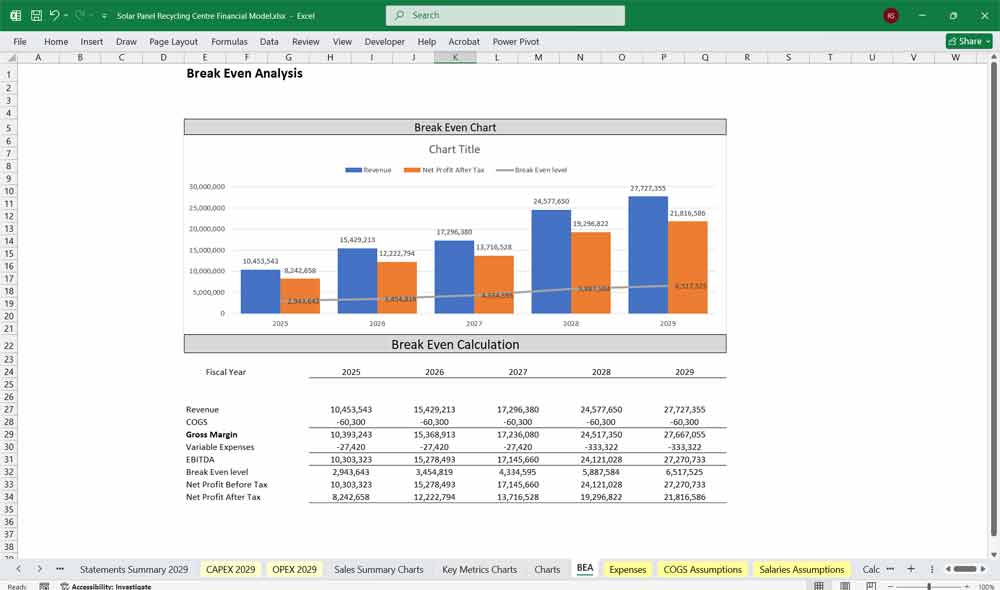

Key Financial Metrics

To assess the project’s performance, the model typically includes:

EBITDA Margin (% of revenue)

Net Profit Margin

Payback Period

Internal Rate of Return (IRR)

Net Present Value (NPV)

Debt Service Coverage Ratio (DSCR)

Break-even Volume (tons/year)

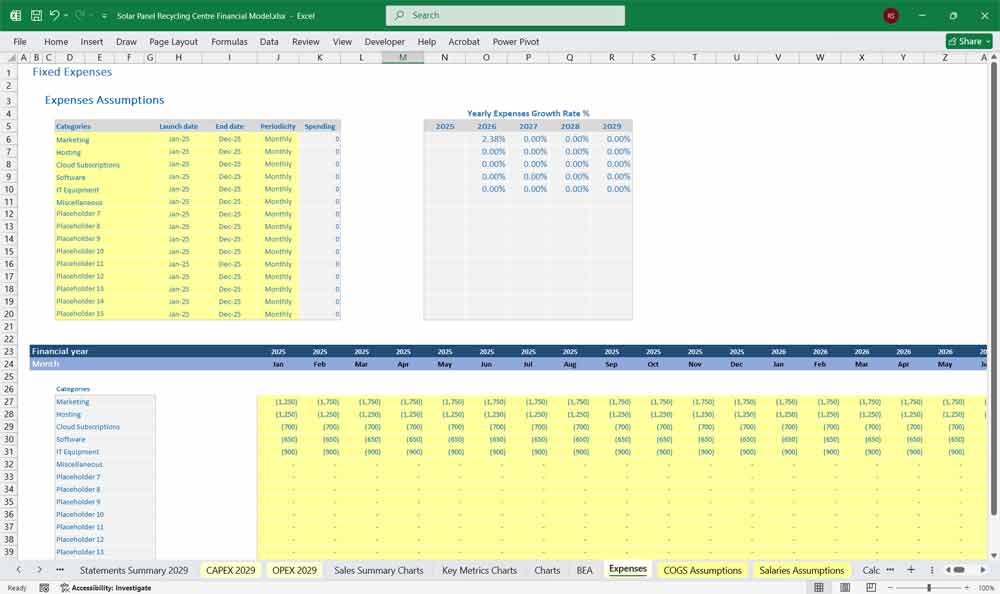

Operating Expenses

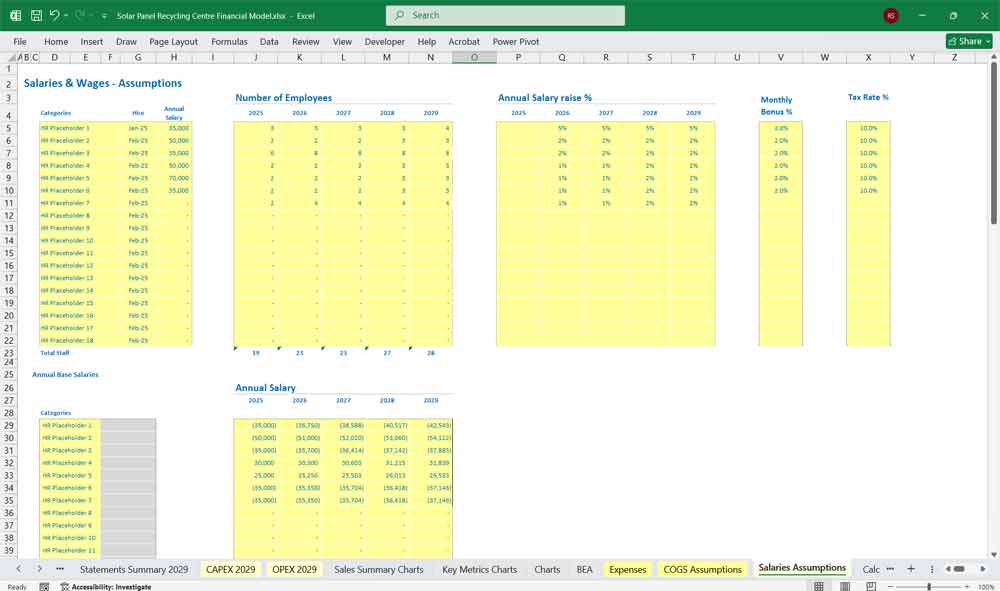

Direct Costs (Cost of Goods Sold):

Labor (sorting, handling, technical staff),

Consumables (chemicals, abrasives),

Maintenance and spare parts,

Energy consumption,

Waste disposal and hazardous material handling.

Operating Expenses (OPEX):

Rent or land lease,

Administrative and management salaries,

Insurance, marketing, IT systems,

Quality assurance and certification costs.

Depreciation and Amortization:

Based on equipment, machinery, and building value.

Straight-line over 10–15 years.

Interest Expense:

From debt financing (bank loans or green bonds).

Taxes:

Corporate tax rate applied to EBT (Earnings Before Tax).

Key Profit Metrics

Gross Profit = Revenue – Direct Costs

EBITDA = Gross Profit – OPEX

EBIT = EBITDA – Depreciation & Amortization

Net Income = EBIT – Interest – Taxes

Final Notes on the Financial Model

This 20 Year Solar Panel Recycling Centre Financial Model must focus on balancing capital expenditures with steady revenue growth from diversified services. By optimizing operational costs, and power efficiency, and maximizing high-margin services, the model ensures sustainable profitability and cash flow stability.

Download Link On Next Page