Sawmill Financial Model

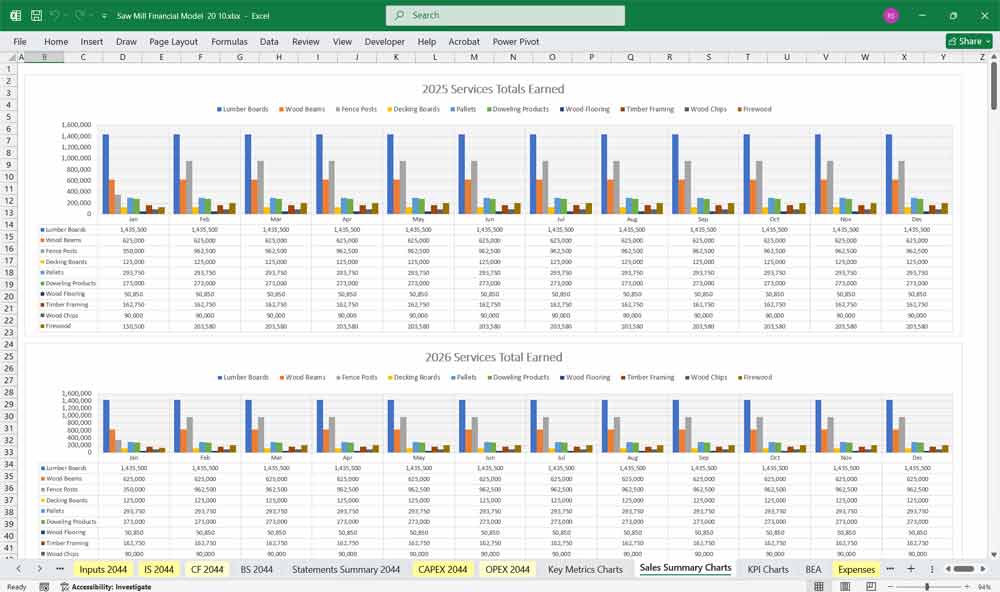

A comprehensive 20-Year, 3-Statement Excel Sawmill Financial Model includes revenue streams from sales of Lumber Boards, Wood Beams, Fence Posts, Decking Boards, etc and an 80 product version. Cost structures, and financial statements to forecast the financial health of your Mill.

20 Year Financial Model Bundle for a Sawmill

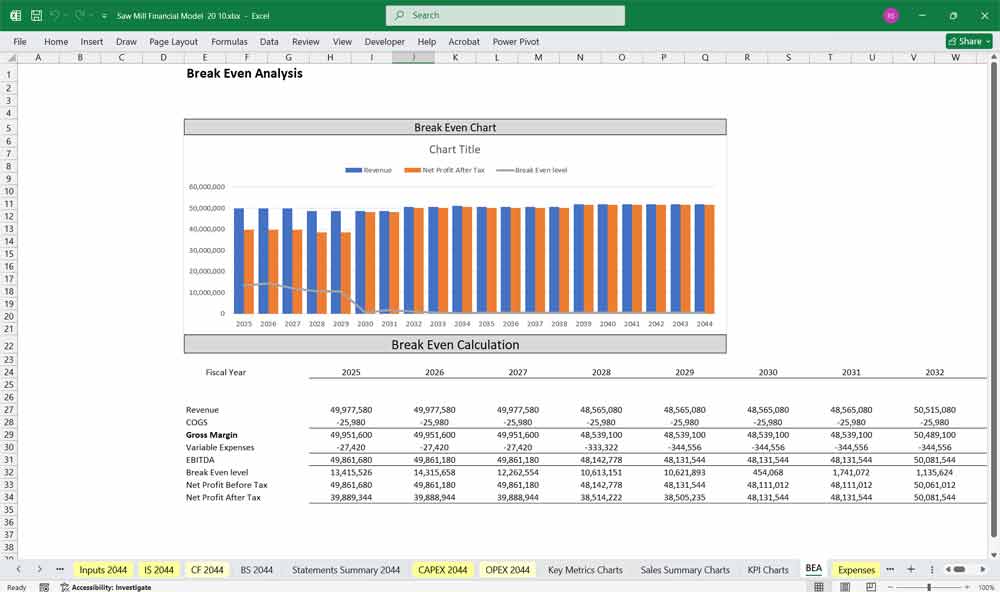

This comprehensive 20 Year Sawmill Model encompasses detailed revenue projections, cost structures, capital expenditures, and financing needs. This model provides a thorough understanding of the financial viability, profitability, and cash flow position of the centre. Both versions include 20x Income Statements, Cash Flow Statements, Balance Sheets, CAPEX sheets, OPEX Sheets, Statement Summary Sheets, and Revenue Forecasting Charts with the specified revenue streams, BEA charts, sales summary charts, employee salary tabs and expenses sheets. Over 120 spreadsheets each.

In the 2 versions.

Version 1: contains 10 editable inputs for the sales of Lumber Boards, Wood Beams, Fence Posts, Decking Boards, etc.

Version 2: has up to 80 product lines for you to list your individual wood products by item.

You get both versions in 1 zip file so you can decide which one is best for your company.

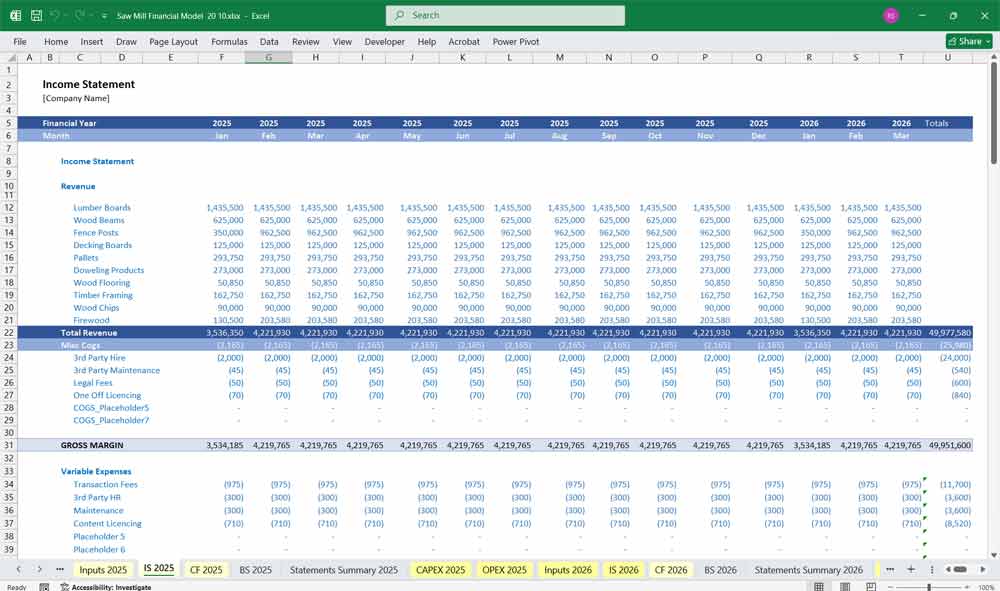

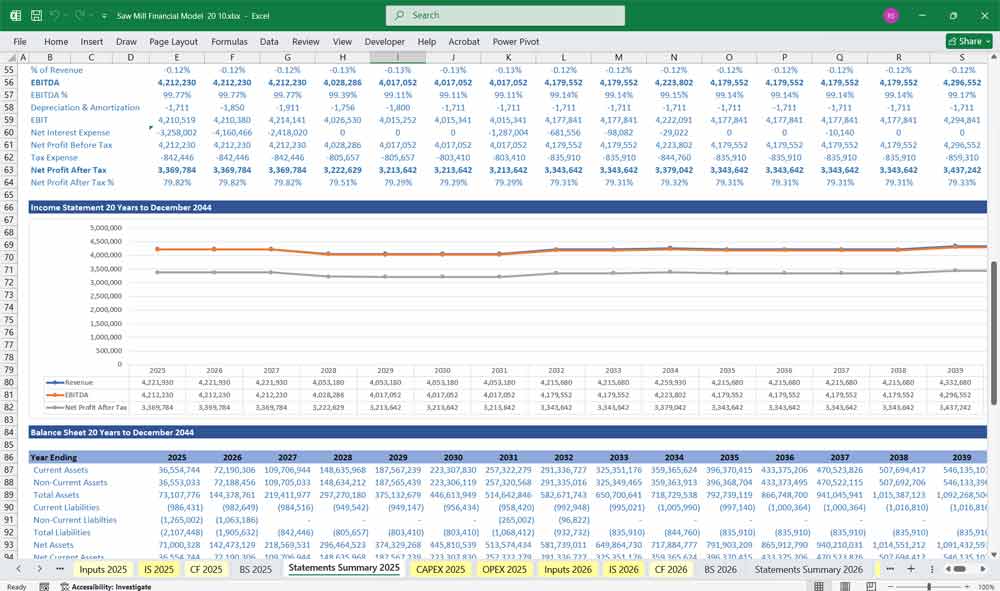

Income Statement (Profit & Loss Statement)

This projects revenues, costs, and net profitability over time (monthly, quarterly, annually).

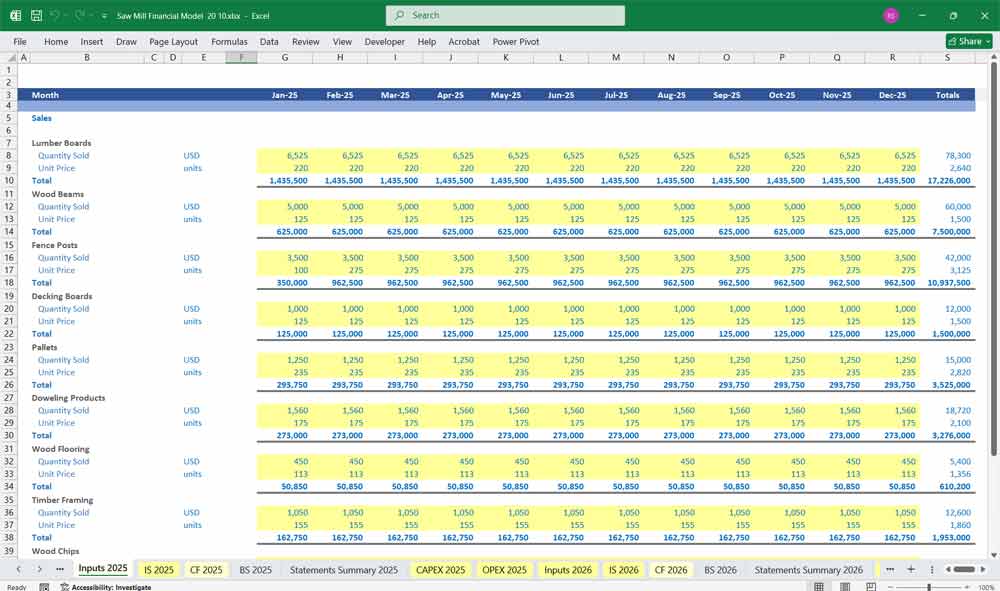

Revenue

Primary Lumber Sales

Volume of logs processed (m³ or board feet).

Yield (usable lumber %).

Average selling price per unit (varies by grade/species).

Byproduct Revenue

Wood chips (sold to paper mills/biomass plants).

Sawdust/shavings (pellets, animal bedding).

Bark/mulch sales.

Value-added Products (if applicable)

Kiln-dried lumber.

Treated wood products.

Custom cutting/planing services.

Cost of Goods Sold (COGS)

Raw Material Costs

Log purchases (primary cost driver).

Transportation/handling of logs.

Processing Costs

Direct labor (mill operators, sawyers, loaders).

Power/fuel (very energy-intensive process).

Equipment wear & tear (blades, lubricants).

Kiln drying/treatment chemicals (if applicable).

Packaging & Shipping

Gross Profit = Revenue – COGS

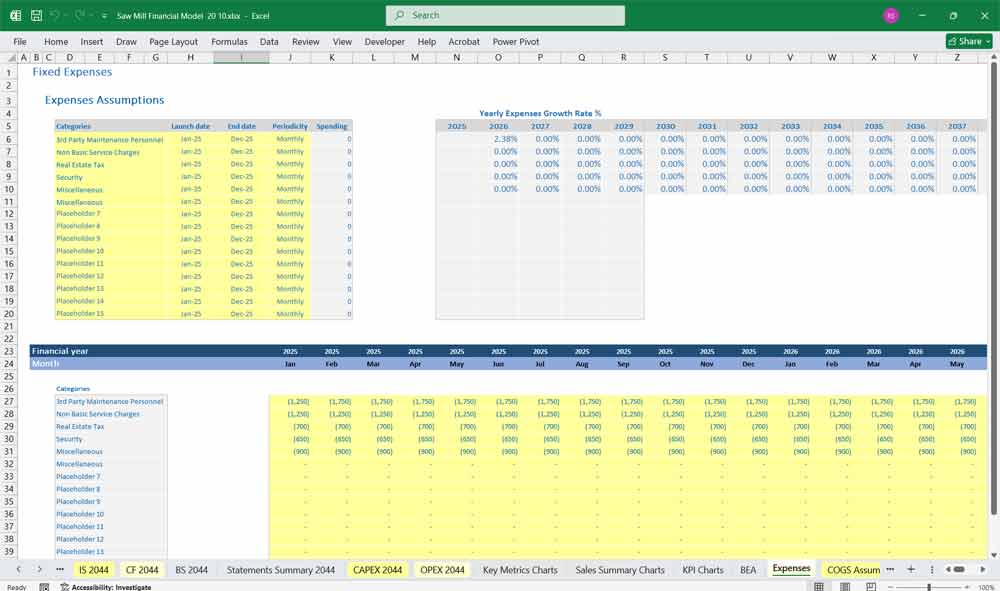

Operating Expenses

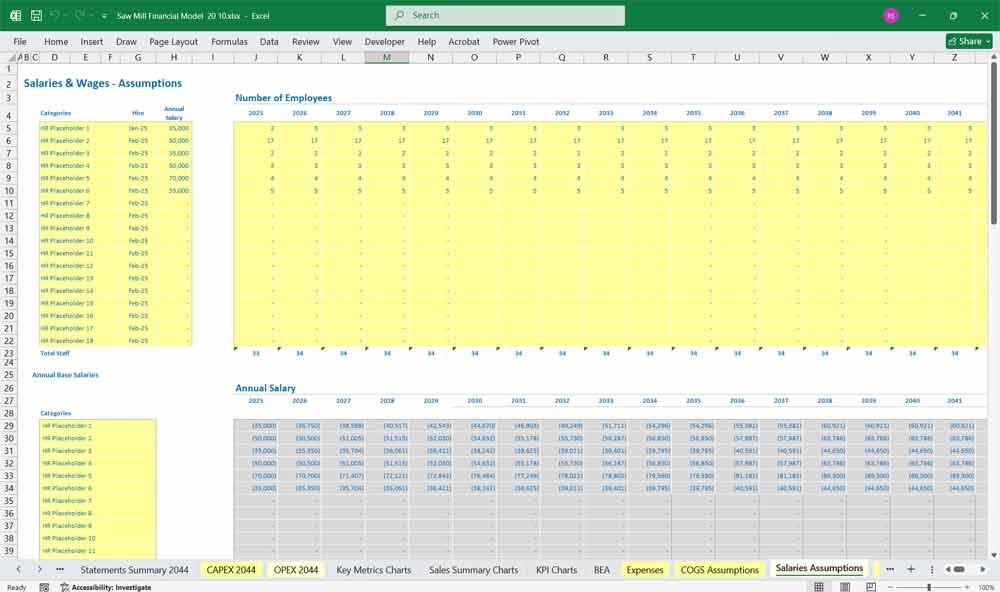

Labor Overheads

Salaries (management, admin, maintenance).

Benefits/payroll taxes.

Maintenance & Repairs

Equipment upkeep.

Depreciation & Amortization

Sawmill machinery.

Kilns/dryers.

Buildings.

Insurance

Property, liability, workers’ comp.

General & Administrative (G&A)

Office expenses, IT, accounting, legal.

Marketing & Sales

Customer acquisition, distributors, trade shows.

Operating Income (EBIT)

Other Items

Interest Expense

On loans for equipment/working capital.

Taxes

Corporate tax rate applied to pre-tax income.

Net Income

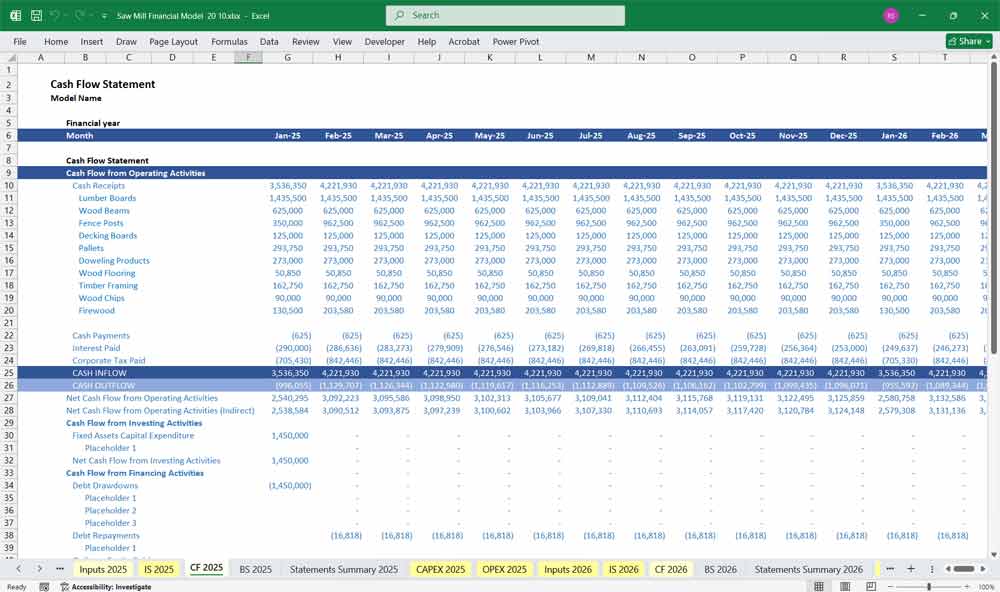

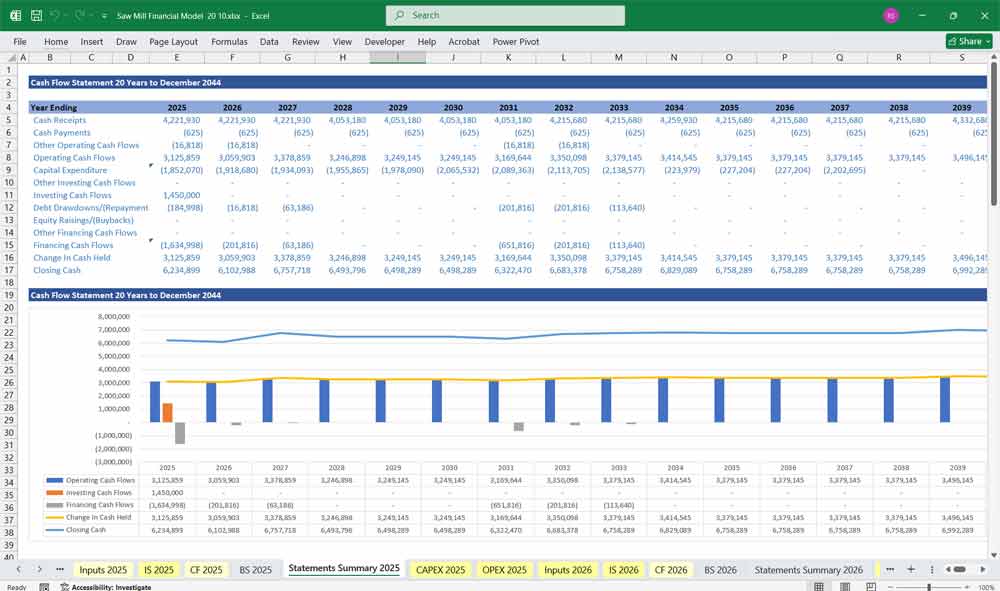

Sawmill Cash Flow Statement

Tracks actual cash inflows/outflows. For a sawmill, working capital swings and capex are critical.

Operating Cash Flow

Cash Inflows

Customer payments (may involve trade credit).

Cash Outflows

Payments to log suppliers (often upfront or short terms).

Payroll, energy, repairs.

Inventory build (logs and finished lumber).

Accounts receivable/payable management.

Adjustments:

Add back depreciation & amortization (non-cash).

Adjust for changes in working capital (inventory, AR, AP).

Investing Cash Flow

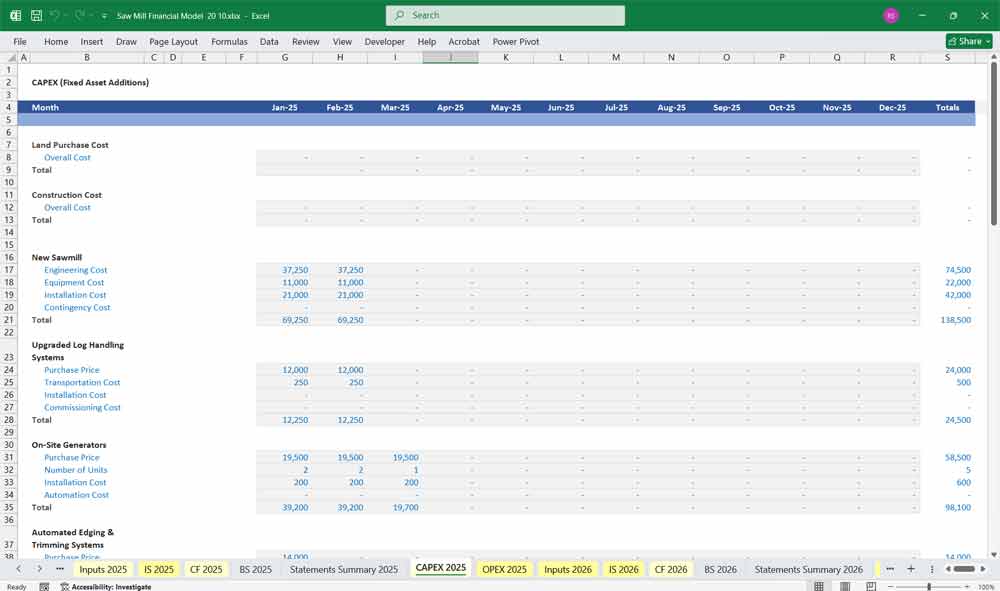

Capital Expenditures (CapEx)

Sawmill machinery (saws, debarkers, conveyors).

Kiln dryers, planers, loaders, forklifts.

Land, buildings, expansion.

Asset Disposals

Sale of old machinery/equipment.

Financing Cash Flow

Debt Financing

Bank loans, credit lines, equipment financing.

Equity Financing

Shareholder contributions.

Debt Service

Principal repayments.

Dividends (if applicable).

Net Cash Flow & Ending Balance

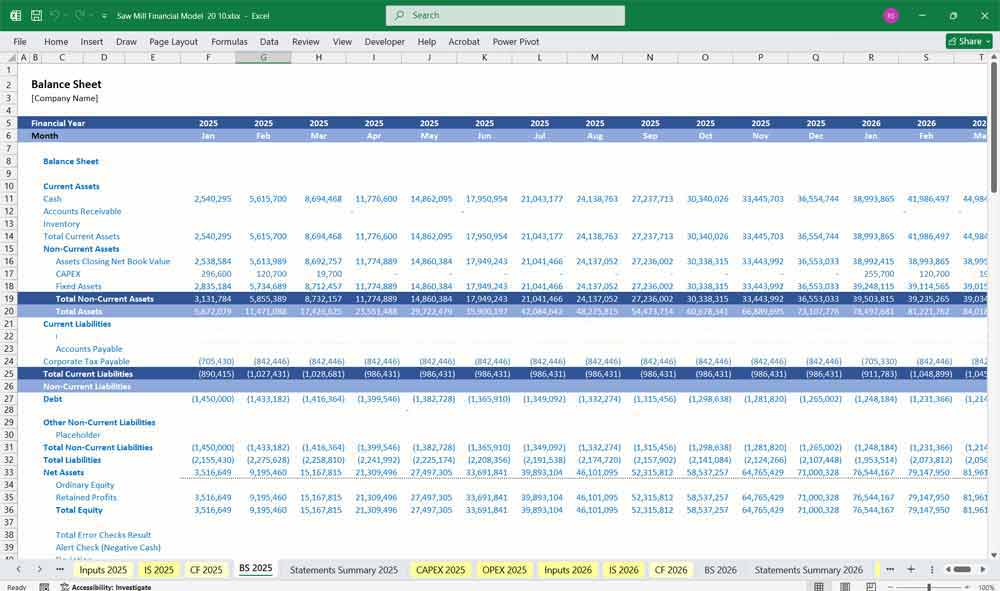

Sawmill Balance Sheet

Snapshot of financial position at period end.

Assets

Current Assets

Cash & cash equivalents.

Accounts receivable (customers).

Inventory:

Logs (raw materials).

Work-in-progress (partially processed wood).

Finished lumber & byproducts.

Non-Current Assets

Property, Plant, and Equipment (PP&E):

Sawmill machinery, kilns, forklifts.

Buildings & land.

Less: Accumulated Depreciation.

Other Assets

Security deposits, long-term investments.

CAPEX (10 Editable)

Log Handling Systems.

- Automated Edging & Trimming Systems.

- Kilns.

- Waste Timber Recycling Systems.

Liabilities

Current Liabilities

Accounts payable (to log suppliers, utilities).

Accrued wages, taxes payable.

Short-term debt (working capital lines).

Non-Current Liabilities

Long-term debt (equipment loans, mortgages).

Lease obligations.

OPEX (10 Editable)

Personnel Costs.

- Log Purchase Costs.

- Blades & Saw Teeth.

- Lubricants & Coolants.

Equity

Share Capital / Owner’s Equity

Retained Earnings

Additional Paid-in Capital (if external investors).

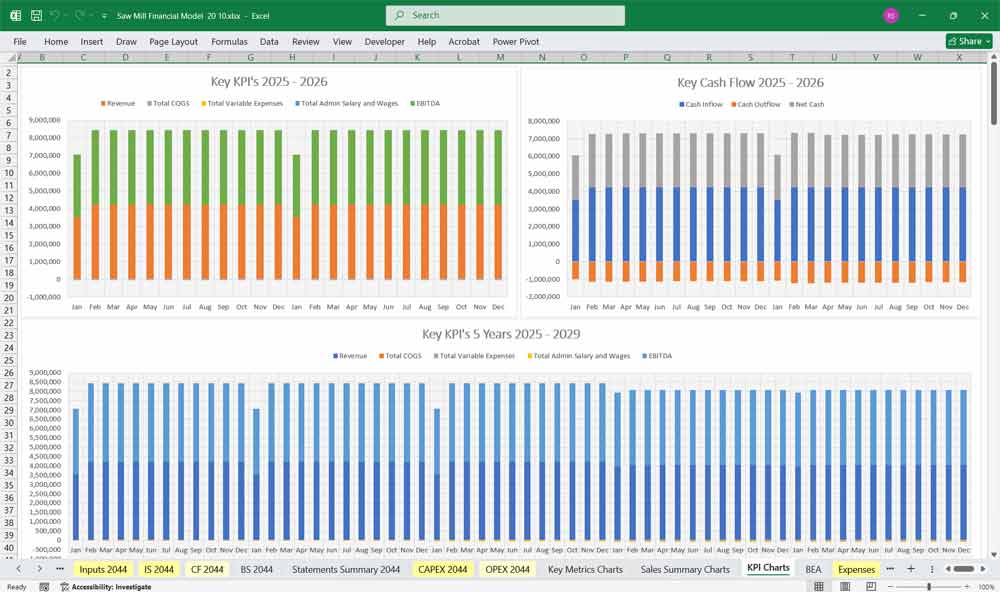

Key Financial Metrics for a Sawmill

Key Ratios & Metrics (For Sawmill Analysis)

Gross Margin % (lumber yields vs log costs).

EBITDA Margin (core profitability).

Inventory Turnover (logs/lumber).

Working Capital Cycle (days inventory + receivable – payable).

Debt Service Coverage Ratio (DSCR) (important for financing).

Capacity Utilization % (actual vs potential mill throughput).

20-Year Model Sawmill Benefits

A 20-year financial model provides long-term visibility into the sawmill’s operations, helping owners and investors assess sustainability in a highly cyclical industry. Lumber prices, raw log costs, and demand for byproducts like chips and sawdust often fluctuate with housing markets and economic cycles. By projecting over two decades, management can stress-test assumptions and prepare for both high and low market conditions.

Better Capital Planning For Your Sawmill

Such a model is also essential for capital planning. Sawmills are capital-intensive businesses, requiring large investments in machinery, kilns, and facilities that often have useful lives spanning decades. A 20-year view allows operators to schedule equipment replacement, plan for modernization, and evaluate the return on capital projects. This reduces the risk of unexpected breakdowns or underinvestment.

20 Years Of Sawmill Evaluations

From a financing perspective, lenders and investors prefer long-term models to evaluate repayment capacity and risk. A detailed projection of cash flows over 20 years shows how the business can service debt, reinvest profits, and maintain working capital. This can strengthen the sawmill’s case when negotiating loans or attracting outside investment.

Sawmill Expansion Planning

A long-term model also supports strategic decision-making. It allows management to analyze scenarios such as expanding into value-added products, diversifying revenue through biomass energy sales, or acquiring additional land for raw material supply. By seeing how these strategies impact revenues, costs, and cash flow over two decades, leadership can make informed, evidence-based choices.

20 Years of Sawmill Stability Planning

Finally, a 20-year financial model provides stability and confidence in planning succession or exit strategies. Whether the owners plan to sell, pass the business to the next generation, or bring in new partners, a robust financial roadmap demonstrates the company’s resilience and long-term value. This can significantly increase credibility with buyers, heirs, and stakeholders.

Final Notes on the Financial Model

This 20 Year Sawmill Financial Model must focus on balancing capital expenditures with steady revenue growth from diversified services. By optimizing operational costs, and power efficiency, and maximizing high-margin services, the model ensures sustainable profitability and cash flow stability.

Download Link On Next Page