Quantum Computing DCF Financial Model Excel Template

20-Year Financial Model for a Quantum Computing Company

This very extensive 20 Year DCF Quantum Computing Excel Template includes detailed revenue projections, cost structures, capital expenditures, and financing needs. These models provide a thorough understanding of the financial viability, profitability, and cash flow position of your manufacturing company. Includes: 20x Income Statements, Cash Flow Statements, Balance Sheets, CAPEX sheets, OPEX Sheets, Statement Summary Sheets, and Revenue Forecasting Charts, with the revenue streams, BEA charts, sales summary charts, employee salary tabs and expenses sheets.

This financial model is designed for a company operating in five core segments: However all are editable.

- Quantum-as-a-Service (QaaS)

- Consulting and Proofs of Concept (PoCs)

- Hardware and Components Sales

- Software and Algorithm Development

- Research Grants and Strategic Partnerships (optional but common)

Quantum-as-a-Service (QaaS)

QaaS provides customers remote access to quantum computers through cloud APIs.

Revenue Streams

- Subscription plans

- Pay-per-shot / pay-per-circuit execution

- Reserved capacity contracts

- Premium SLA and support

- Hybrid quantum-classical workflow orchestration

Key Drivers

- Number of enterprise customers

- Number of active users

- Average monthly recurring revenue (MRR)

- Quantum processing units (QPUs) utilization

- Gross margin per compute hour

- Churn rate

- Revenue retention

Consulting and Proofs of Concept (PoCs)

Professional services to identify use cases and demonstrate quantum advantage.

Services

- Quantum readiness assessments

- Industry workshops

- Pilot projects

- Algorithm design

- Benchmarking studies

Drivers

- Number of consulting projects

- Average project value

- Number of PoCs

- Conversion rate from PoC to recurring QaaS contracts

Hardware and Components Sales

Sales of specialized, high-end components to labs, universities, and other quantum companies.

Products

- Dilution refrigerators

- Control electronics

- Microwave generators

- Quantum interconnects

- Cryogenic amplifiers

- Photonic modules

- Superconducting chips

- Trapped-ion components

Drivers

- Units sold by component type

- Average selling price (ASP)

- Manufacturing yield

- Warranty reserve

Software and Algorithm Development

Commercial software tools and custom algorithms.

Offerings

- Quantum software development kits (SDKs)

- Optimization libraries

- Error mitigation software

- Compiler and transpiler tools

- Industry-specific algorithms

- Licensing of patented methods

Revenue Models

- Annual licenses

- Subscription SaaS

- Per-seat pricing

- Royalty arrangements

Drivers

- Number of licenses

- Average annual contract value (ACV)

- Renewal rates

Research Grants and Strategic Partnerships

Often significant in early stages.

Sources

- Government grants

- Defense contracts

- University collaborations

- Joint development agreements

Accounting Considerations

- Recognized as other revenue or offset against R&D depending on accounting policy.

Income Statement (P&L)

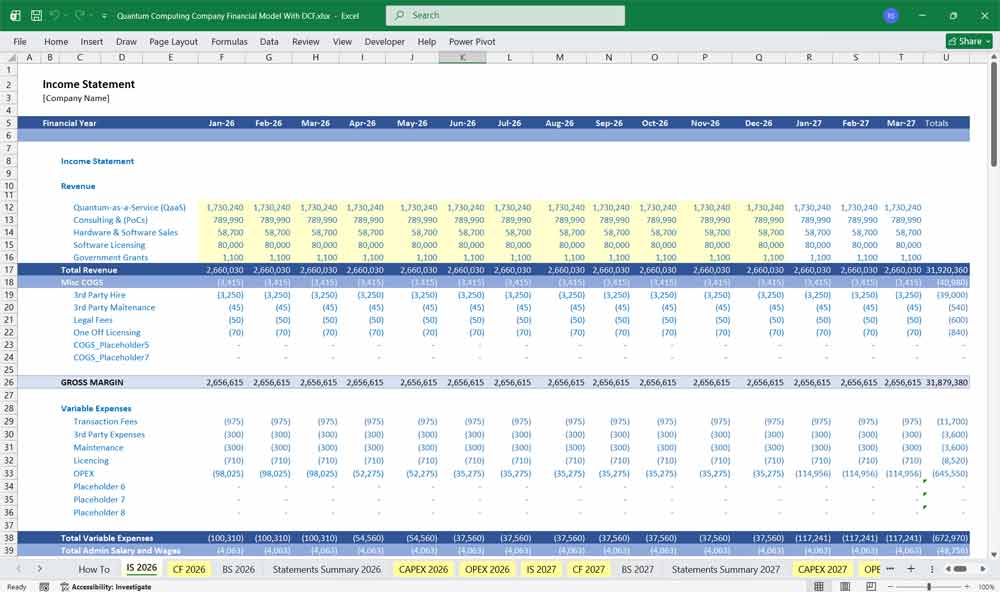

The Income Statement reflects the transition from R&D-heavy beginnings to a diversified service and product mix.

Revenue Streams

Quantum-as-a-Service (QaaS): Modeled on “Compute Seconds” or “Circuit Shots.”

Calculation: (Number of Qubits Available / Capacity Utilization) × Price per Shot.

Consulting & PoCs: High-touch, high-margin human capital revenue.

Calculation: (Number of Quantum Engineers) × (Billable Rate) × (Utilization Rate).

Hardware & Component Sales: Lumpy, high-ticket sales of dilution refrigerators, ion traps, or control electronics.

Calculation: Units Sold × ASP (Average Selling Price).

Software & Algorithm Licensing: Annual Recurring Revenue (ARR) for middleware or specialized solvers.

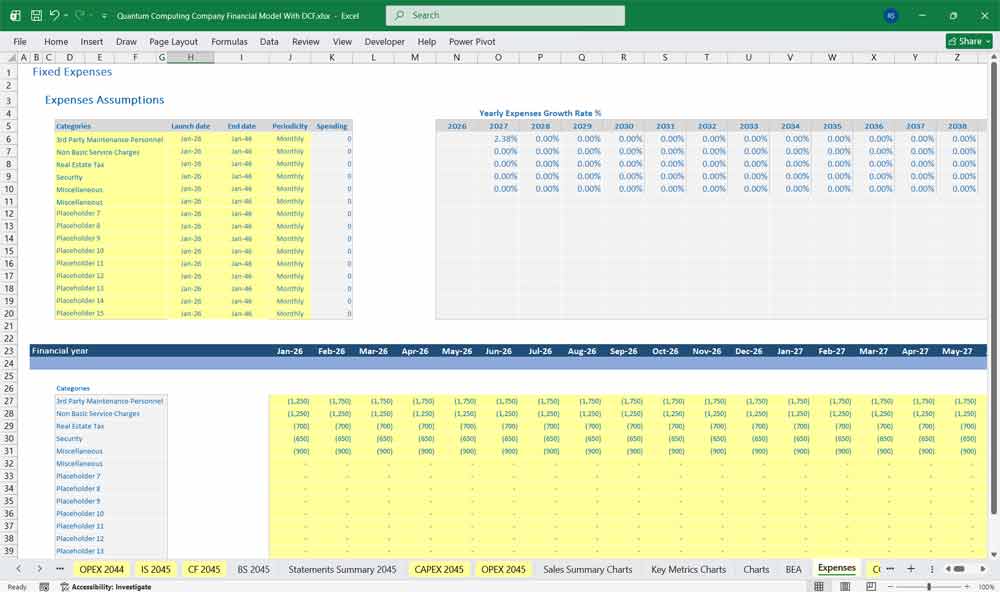

Expenses & Margins

Cost of Goods Sold (COGS): Includes electricity for cooling, cloud infrastructure overhead, and raw materials for hardware (gold, specialized silicates).

Operating Expenses (OpEx):

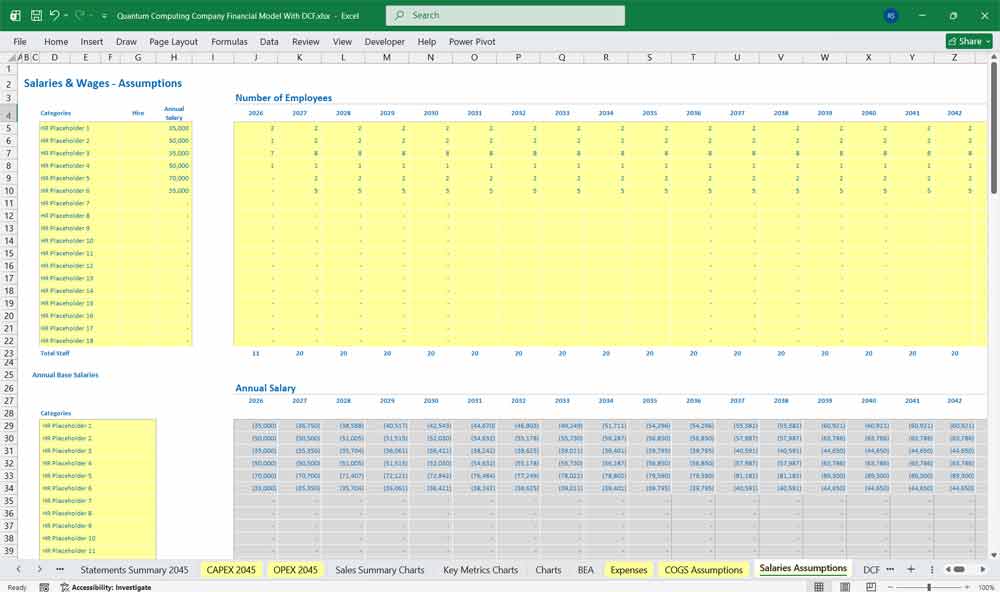

R&D: The largest line item (often 60–80% of spend). Includes salaries for PhD-level physicists and cryogenic engineers.

S&M: Sales cycles for quantum are long (12–18 months), requiring technical sales teams.

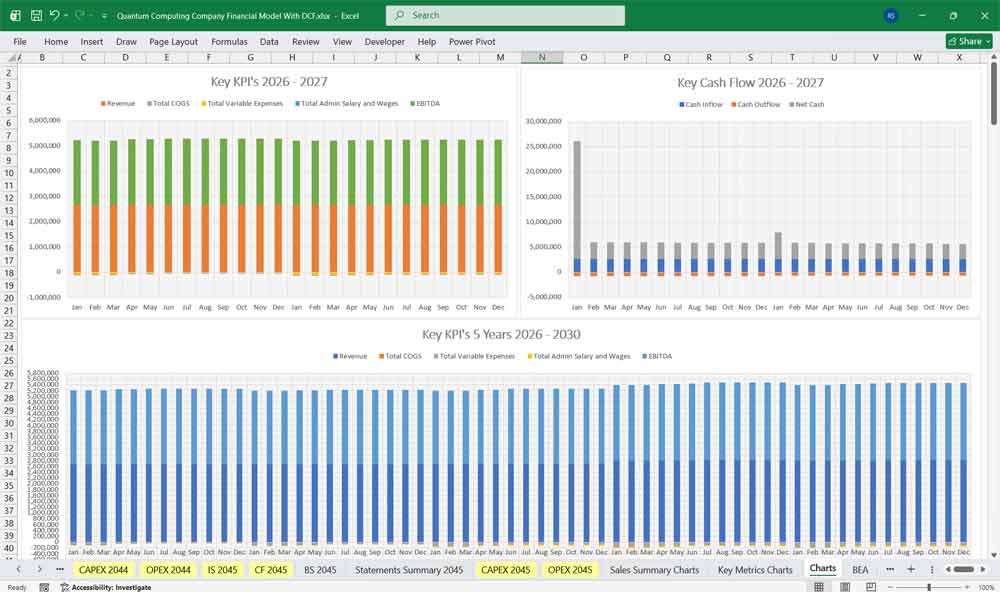

EBITDA: Likely negative for the first 3–5 years until QaaS scaling offsets the high R&D “burn.”

QaaS COGS

- Data center hosting

- Electricity

- Cryogens

- Equipment maintenance

- Quantum control systems

- Customer support

- Depreciation of QPUs

Consulting COGS

- Consultant salaries

- Travel

- Project software costs

Hardware COGS

- Raw materials

- Semiconductor fabrication

- Assembly and testing

- Freight

- Warranty reserves

Software COGS

- Cloud hosting

- Technical support

- Third-party licensing

Operating Expenses

Research and Development (largest cost center)

- Quantum physicists

- Hardware engineers

- Software developers

- Lab consumables

- Fabrication runs

- Patent filing

- University collaborations

Sales and Marketing

- Enterprise sales teams

- Industry conferences

- Business development

- Marketing content

General and Administrative

- Executive salaries

- Finance and legal

- Insurance

- Rent

- HR

Depreciation and Amortization

- Laboratory equipment

- Capitalized software

- Acquired IP

Quantum Computing Company Cash Flow Statement

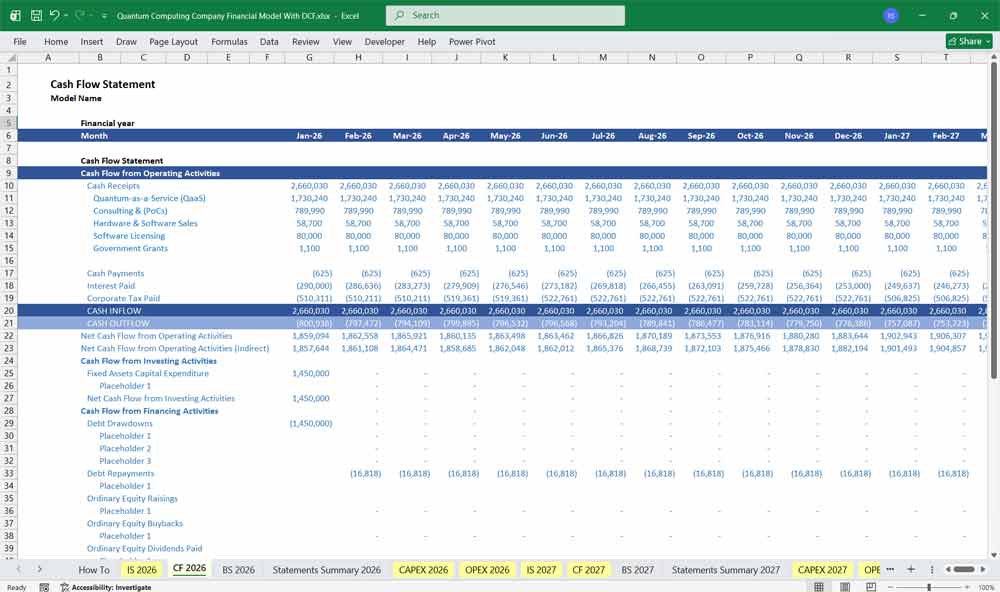

This is the most critical document for a quantum startup, as it tracks the “Runway” before the next funding round.

Operating Activities: * Adjusts Net Income for non-cash items like Depreciation (quantum computers have a short functional life of 3–5 years due to rapid obsolescence).

Tracks the high “Burn Rate” necessary to maintain talent.

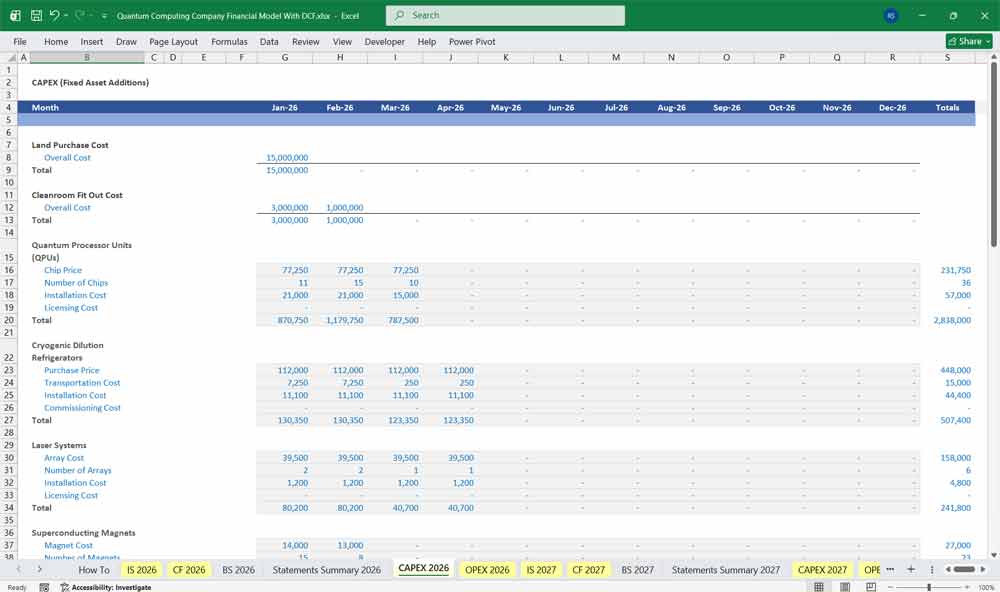

Investing Activities (CapEx): * Massive cash outflows for Lab Infrastructure, cleanrooms, and the fabrication of the quantum processors themselves.

Unlike SaaS, a quantum company must “build the factory” before it can sell the service.

Financing Activities: * Inflows from Venture Capital (Series A/B/C) or Government Grants (e.g., DARPA, Horizon Europe).

These must be timed to ensure the cash balance never hits zero before “Quantum Advantage” is reached.

Operating Cash Flow

Start with Net Income

Adjust for:

- Depreciation & amortization

- Stock-based compensation

- Deferred revenue

- Working capital changes

- Grant receivables

Working Capital Components

- Accounts receivable

- Inventory

- Prepaids

- Accounts payable

- Deferred revenue

- Accrued expenses

Investing Cash Flow

Capital Expenditures

- Quantum processors

- Cryogenic systems

- Clean room equipment

- Test and measurement instruments

- Office infrastructure

Capitalized Development Costs

- Software development

- Patents and IP acquisition

Quantum Computing Company Balance Sheet

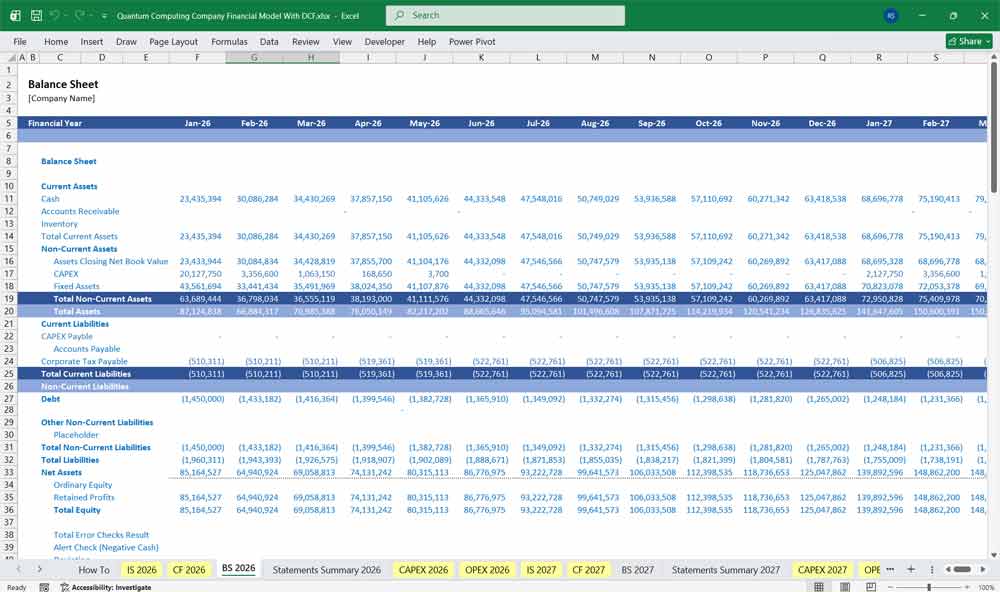

The Balance Sheet for a quantum firm is unique due to the high value of Intellectual Property and specialized physical assets.

Assets

Current Assets: Cash and cash equivalents (highly liquid to cover burn), plus inventory of specialized components (lasers, wiring).

Fixed Assets (PP&E): The actual quantum computers and cryostats. These are high-value but depreciate quickly as qubit counts double.

Intangible Assets: Capitalized R&D and a massive Patent Portfolio. In quantum, your “moat” is your IP.

Liabilities & Equity

Deferred Revenue: Cash received upfront for multi-year QaaS or consulting contracts that hasn’t been “earned” yet.

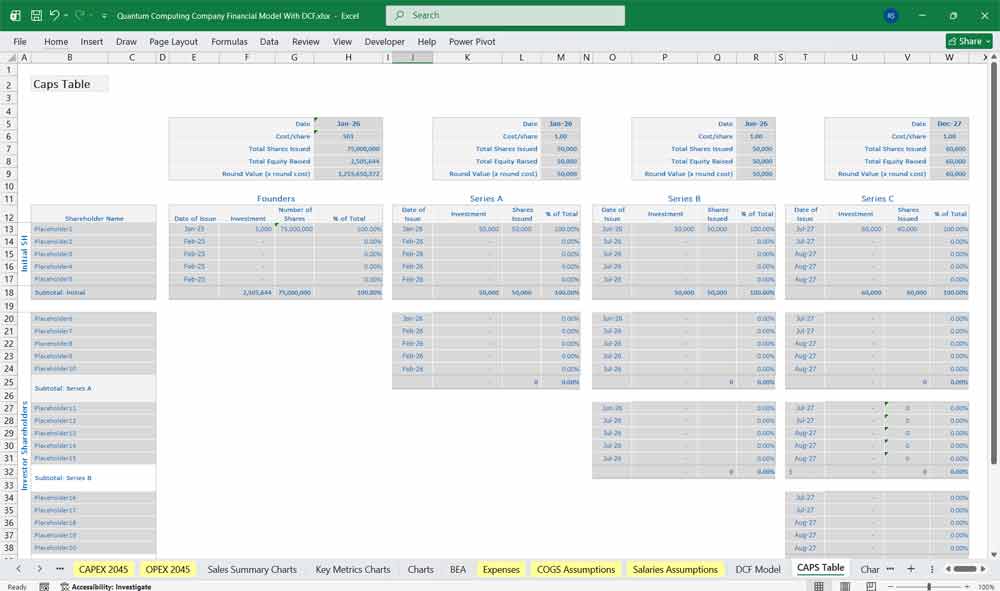

Equity: Significant Paid-in Capital from investors. Early-stage quantum firms rarely carry long-term debt because they lack the predictable cash flow to service interest payments.

Assets

Current Assets

- Cash and equivalents

- Accounts receivable

- Inventory

- Grants receivable

- Prepaid expenses

Non-Current Assets

- Property, plant and equipment (PP&E)

- Capitalized software

- Patents and IP

- Security deposits

- Right-of-use assets

Liabilities

Current Liabilities

- Accounts payable

- Accrued payroll

- Deferred revenue

- Short-term debt

- Lease liabilities

Long-Term Liabilities

- Venture debt

- Convertible notes

- Deferred tax liabilities

- Long-term lease liabilities

Key Quantum Computing Specific Considerations

Technology Metrics

- Number of logical qubits

- Gate fidelity

- Error rate

- Quantum volume

- Coherence time

- System uptime

Commercial Metrics

- ARR

- NPV

- Customer count

- Net revenue retention

- Backlog

- Pipeline

Manufacturing Metrics

- Yield

- Scrap rate

- Lead time

Valuation Approaches

Revenue Multiples

Comparable to deep tech and infrastructure software companies.

Discounted Cash Flow (DCF)

Useful when long-term margins become meaningful.

Probability-Weighted Scenarios

- Base case

- Breakthrough case

- Delayed commercialization case

Scenario Analysis

Important sensitivities:

- Time to fault-tolerant quantum systems

- Customer adoption rate

- QPU utilization

- Hardware yields

- Average contract values

- Fundraising availability

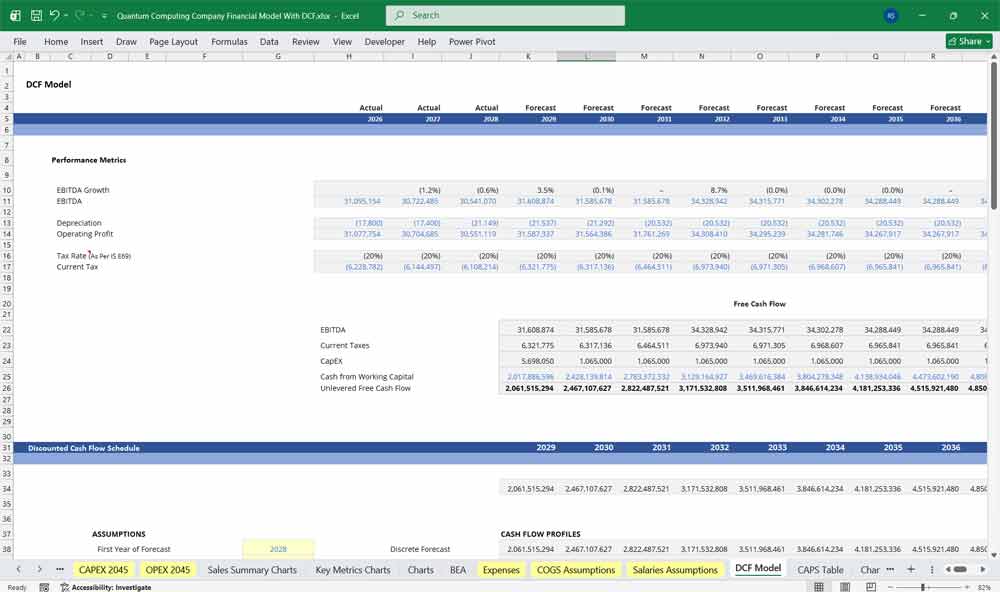

Valuing Your Quantum Computing Company With A DCF

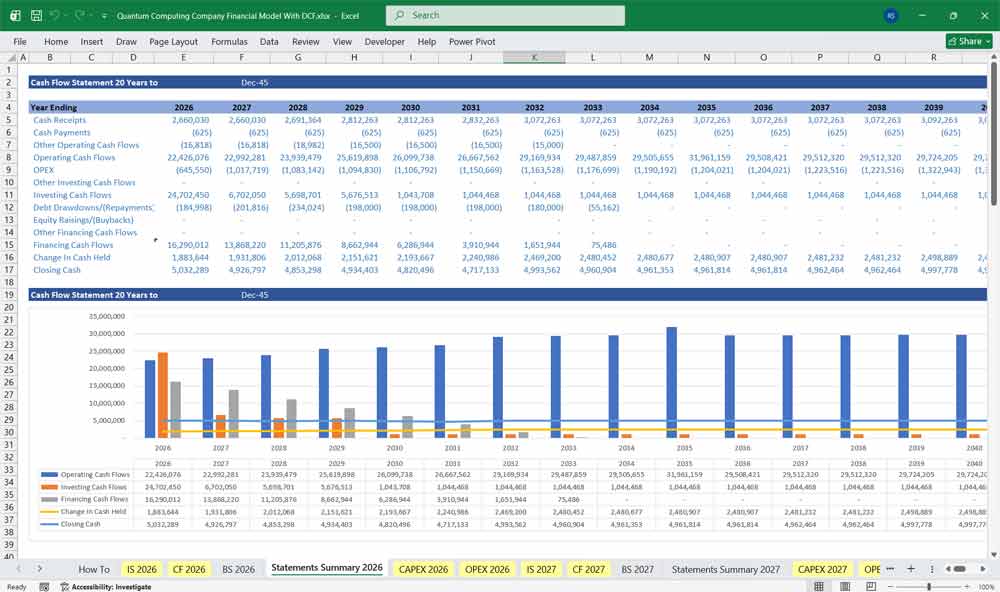

DCF: Valuing the “Superposition” of Future Cash

This 20-year Discounted Cash Flow (DCF) analysis for a quantum computing company estimates the firm’s value based on projected future cash flows generated from quantum hardware sales, cloud-based quantum access, software licensing, research contracts, and strategic partnerships. Revenue forecasts are driven by technological milestones, commercial adoption, government funding, and enterprise demand, while costs include research and development, specialized talent, laboratory infrastructure, and capital expenditures for advanced equipment. Because many quantum computing companies are in early commercialization stages, the DCF model often incorporates a longer forecast period and significant upfront investment before stable cash flows emerge.

WACC: Pricing “Existential Beta” and the Survival Premium

The Weighted Average Cost of Capital (WACC) for a quantum firm typically sits in a stratospheric range of 18% to 25%, reflecting its status as a high-stakes venture bet rather than a traditional business. Because these companies lack the stable cash flows or physical collateral to attract traditional debt, their capital structure is almost exclusively Cost of Equity. In the 2026 market, the discount rate must price in “Decoherence Risk”—the very real possibility that a competitor’s architectural breakthrough or a “Quantum Winter” (where funding dries up before commercialization) renders the company’s tech obsolete. This high hurdle rate ensures that future trillions are appropriately “punished” for the extreme uncertainty of the timeline and the high probability of total capital loss.

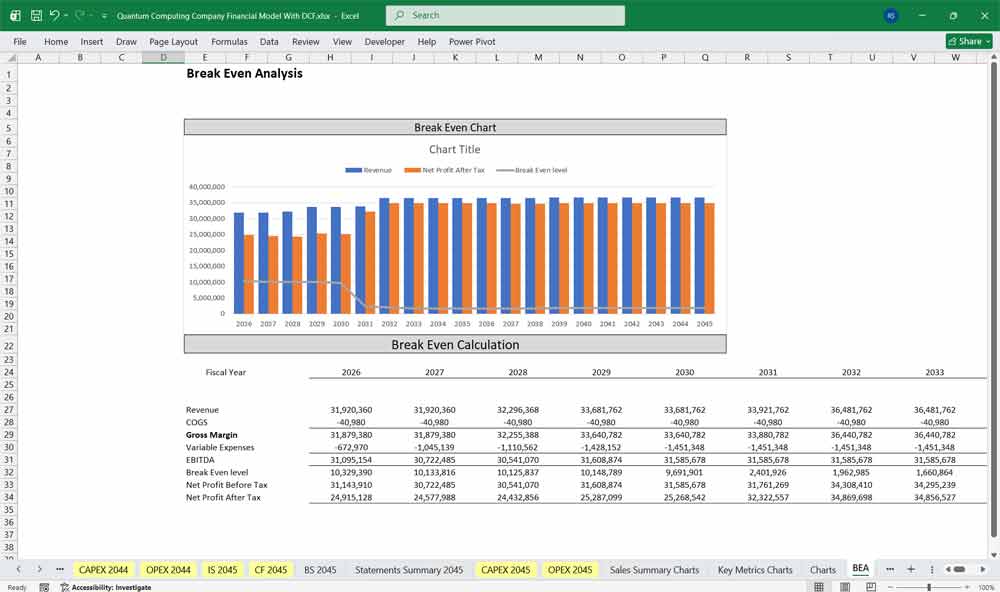

Sensitivity Analysis: Stress-Testing the “Time-to-Fault-Tolerance”

Sensitivity analysis is critical in valuing a quantum computing company due to uncertainty in commercialization timing, customer adoption, pricing, operating margins, and capital requirements. Analysts typically test changes in key assumptions such as revenue growth, probability of technical success, research spending, time to profitability, and WACC. By evaluating how variations in these inputs affect the DCF valuation, sensitivity analysis highlights the most influential value drivers and provides a range of potential outcomes to support strategic and investment decisions.

Final Notes on the Financial Model

This 20 Year Quantum Computing DCF Financial Model Excel Template focuses on balancing capital expenditures with steady revenue growth from a diversified product line. By optimizing operational costs, and power efficiency, and maximizing high-margin services, the models ensure sustainable profitability and cash flow stability.

Download Link On Next Page