PVC Manufacturing Financial Model

Financial Model Overview For PVC Manufacturing

The financial model captures the economics of producing and selling PVC products, projecting revenues, costs, investments, and financing needs over a 20-year horizon.

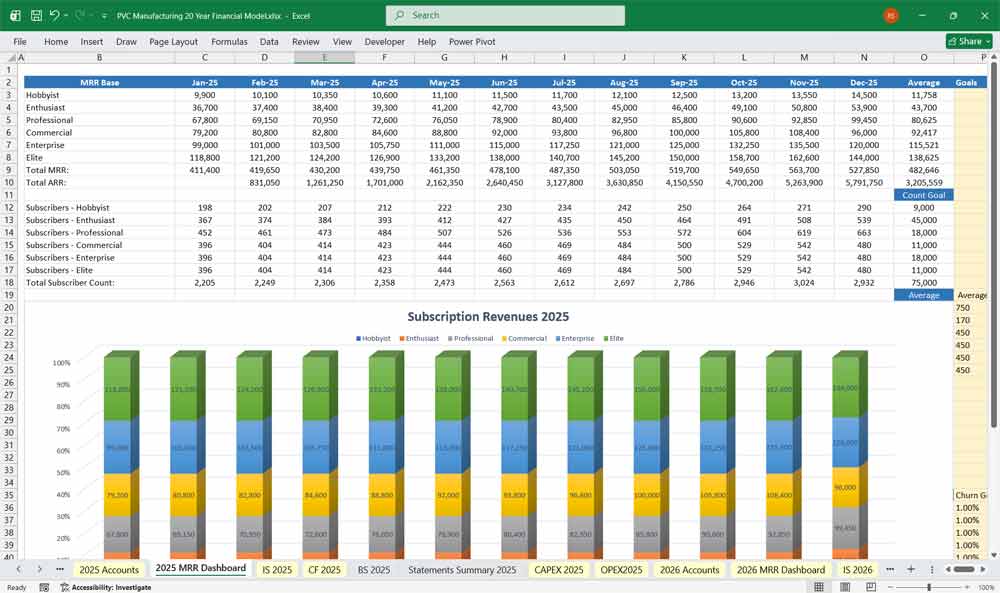

80 Product lines and a 6-tier subscription add-on for your repeat customer sales. It combines:

Operational assumptions (production capacity, utilization, raw material costs, pricing, etc.)

Capital structure assumptions (debt, equity, interest rates)

Financial statements (Income Statement, Balance Sheet, Cash Flow)

Valuation and performance metrics (EBITDA, NPV, IRR, Payback Period)

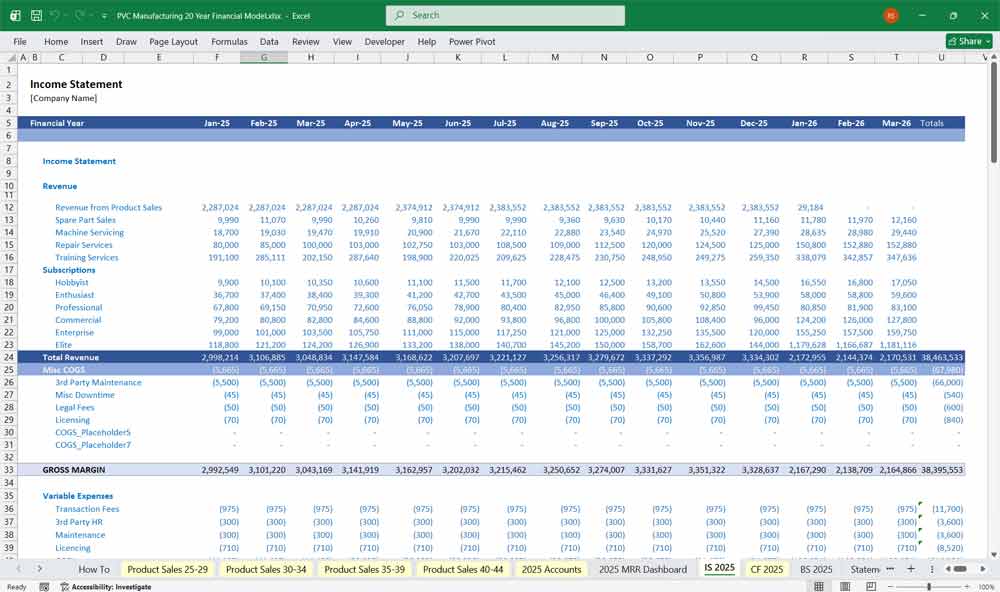

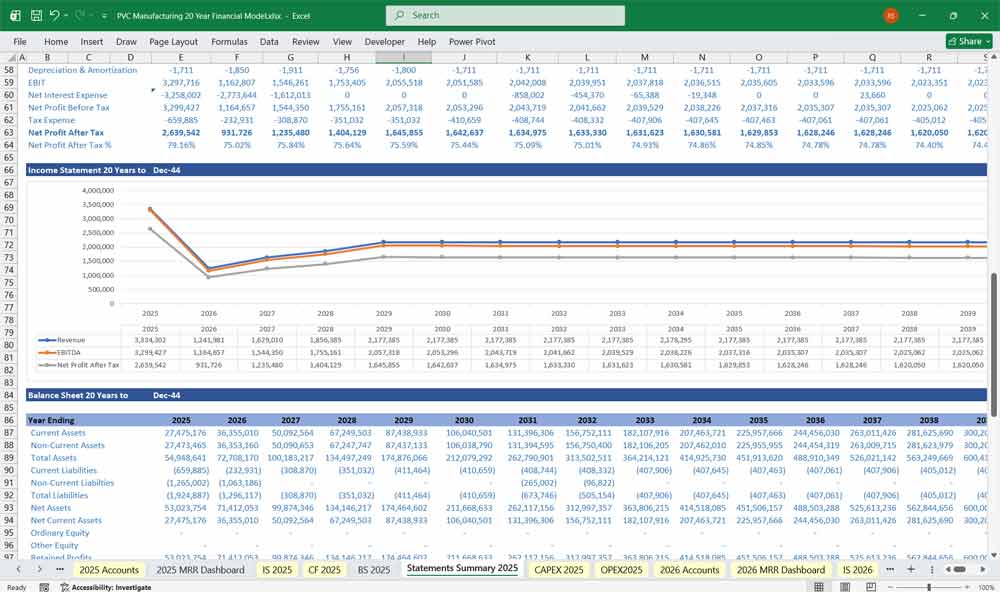

Income Statement (Profit and Loss Statement)

The Income Statement projects the profitability of the PVC manufacturing business over time.

1. Revenue Section

Production Capacity: Total annual production capacity (e.g., in metric tons or units).

Capacity Utilization: Starts lower (e.g., 60–70%) and ramps up as operations stabilize.

Sales Volume: = Production × Utilization Rate.

Selling Price per Unit: Based on market benchmarks and inflationary trends.

Total Revenue: = Sales Volume × Selling Price.

You can segment revenue by product line (e.g., PVC pipes, sheets, fittings) or customer type (wholesale vs. retail).

2. Cost of Goods Sold (COGS)

COGS includes all direct manufacturing costs:

Raw Materials: Mainly PVC resin, plasticizers, stabilizers, lubricants, pigments. Calculated as per-unit material consumption × unit price.

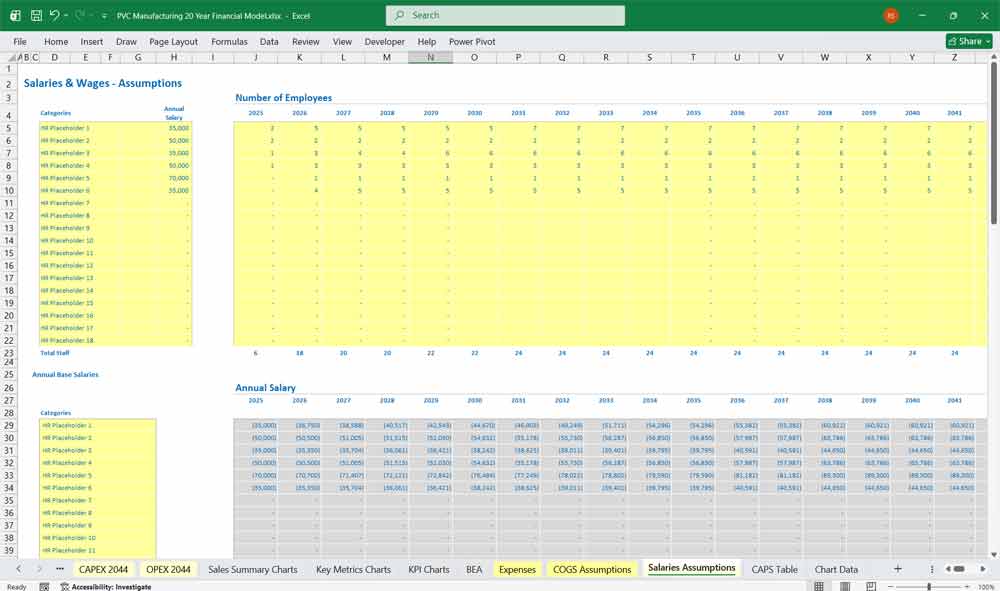

Direct Labor: Plant workers’ wages, supervisors, shift engineers.

Utilities: Electricity (extrusion and molding), water, compressed air, maintenance energy use.

Factory Overheads: Maintenance, spare parts, indirect materials.

Depreciation (Production Equipment): Based on useful lives (usually 10–15 years).

Gross Profit = Revenue – COGS

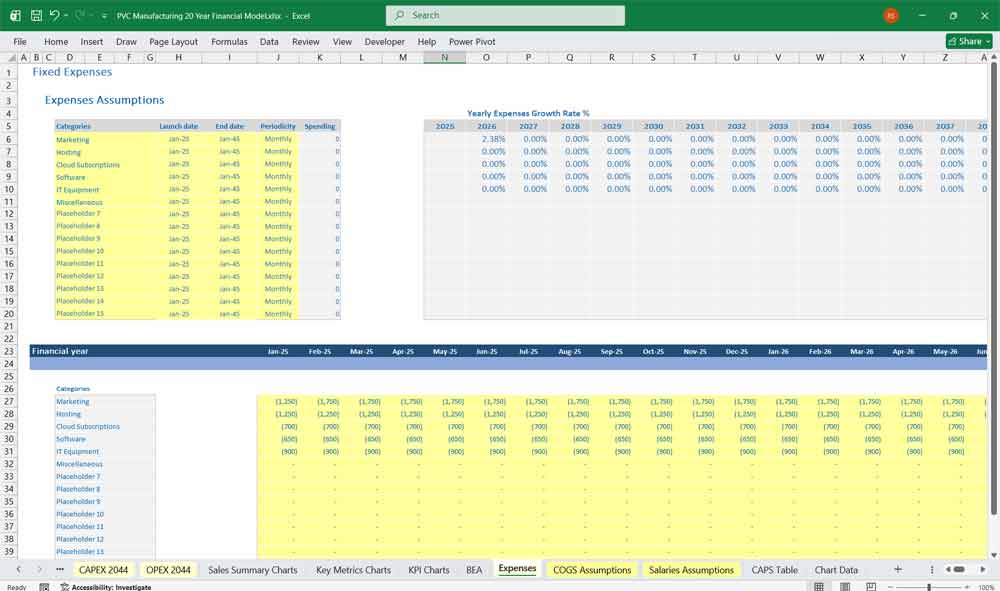

3. Operating Expenses (OPEX)

Selling & Distribution Expenses: Freight, packaging, marketing, dealer commissions.

Administrative Expenses: Office salaries, rent, insurance, IT systems.

Research & Development (optional): For product innovation or formulation optimization.

Depreciation (Administrative Assets): Office equipment, buildings, vehicles.

Operating Profit (EBIT) = Gross Profit – Operating Expenses

4. Financing and Tax

Interest Expense: Calculated on outstanding debt balances (term loans, working capital).

Interest Income: From short-term deposits or investments.

Profit Before Tax (PBT): EBIT – Net Interest Expense.

Tax Expense: Based on applicable corporate tax rate, adjusted for deferred taxes if needed.

Net Profit (EAT) = PBT – Tax

5. Key Ratios

Gross Margin, EBIT Margin, Net Profit Margin.

Return on Equity (ROE), Return on Assets (ROA).

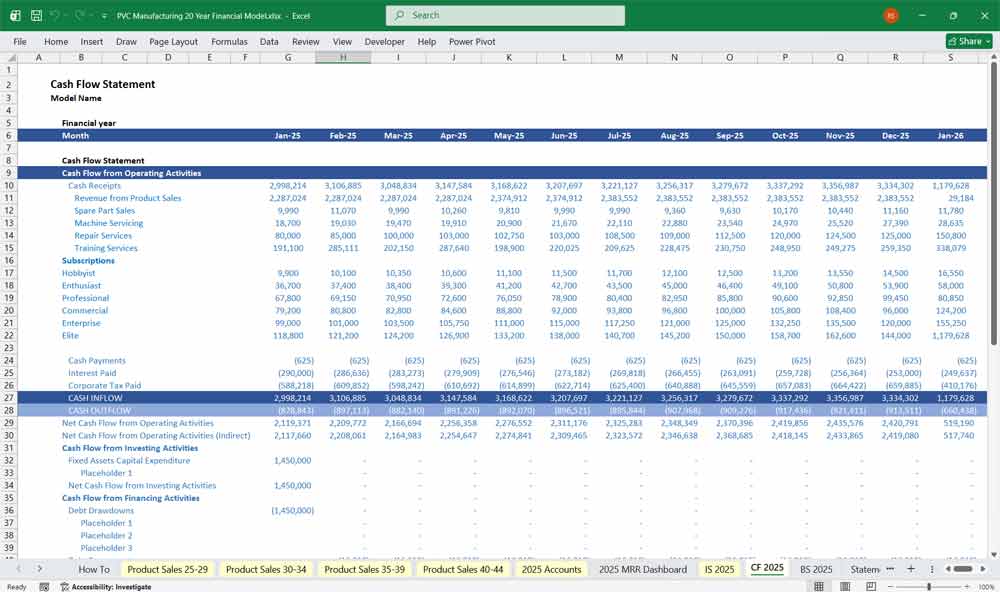

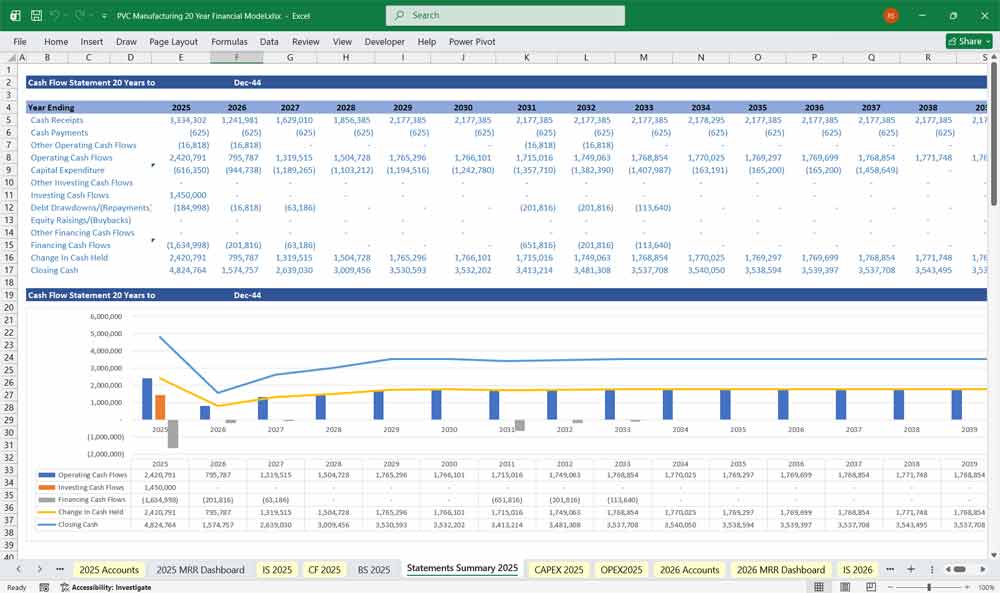

PVC Manufacturing Cash Flow Statement

The Cash Flow Statement reconciles the change in cash from all sources and uses of funds across three main sections: Operating, Investing, and Financing Activities.

1. Cash Flow from Operating Activities

Derived from the Income Statement but adjusted for non-cash items and changes in working capital.

a. Net Profit After Tax (from the Income Statement).

b. Non-Cash Adjustments:

Add back Depreciation.

Adjust for Deferred Taxes, Provisions, etc.

c. Changes in Working Capital:

Increase in Inventory (uses cash).

Increase in Accounts Receivable (uses cash).

Increase in Accounts Payable / Accrued Expenses (sources of cash).

Net Operating Cash Flow = (a + b ± c)

This measures the cash generated by the core manufacturing operations.

2. Cash Flow from Investing Activities

Covers capital expenditures and asset disposals:

Capital Expenditures (CAPEX):

Initial plant construction and machinery.

Periodic equipment replacement or expansion.

Purchase of Land or Buildings.

Sale of Old Equipment or Assets.

Investments in Subsidiaries or Market Securities.

Net Investing Cash Flow = Inflows – Outflows

PVC manufacturing tends to be CAPEX-intensive at the beginning, leading to large negative cash flow in the early years.

3. Cash Flow from Financing Activities

Tracks how the business is funded and how it repays investors:

Equity Infusion: Paid-in capital, new shares, or investor contributions.

Debt Drawdown: Bank loans, project financing.

Loan Repayments: Principal payments reducing outstanding balance.

Interest Payments: Outflow based on loan terms.

Dividends Paid: Once the company achieves profitability.

Net Financing Cash Flow = Inflows – Outflows

4. Net Change in Cash and Closing Balance

Net Cash Flow = Operating + Investing + Financing Cash Flow

Opening Cash Balance: Carried forward from prior period.

Closing Cash Balance: Opening + Net Cash Flow.

This ending cash balance links directly to the Balance Sheet’s cash line item.

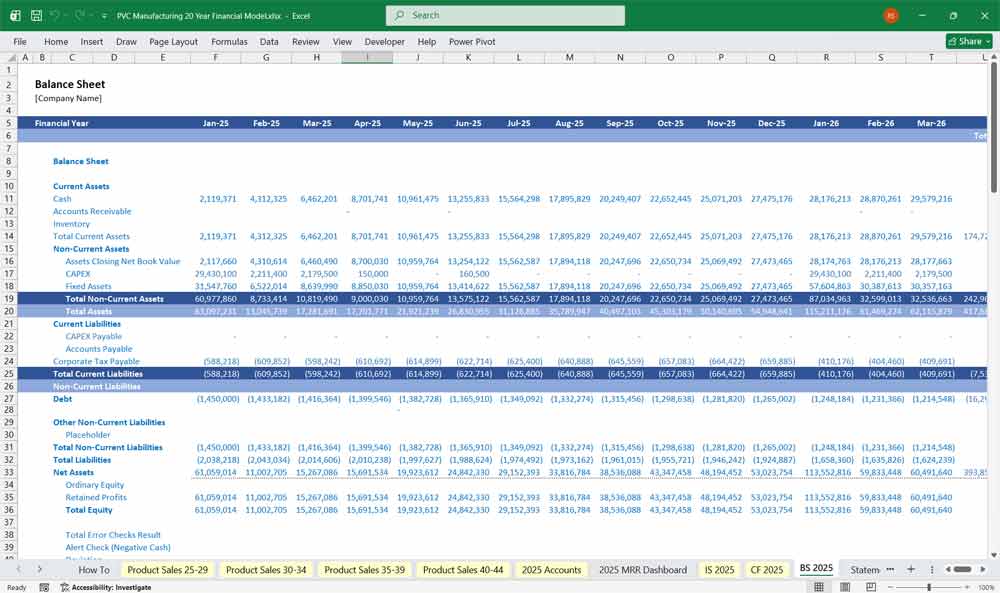

PVC Manufacturing Balance Sheet

The Balance Sheet presents the financial position of the PVC manufacturing company at a specific date, showing what it owns (Assets) and what it owes (Liabilities and Equity).

1. Assets

a. Current Assets

Cash and Cash Equivalents: From the Cash Flow closing balance.

Accounts Receivable: Credit sales outstanding; linked to revenue assumptions.

Inventory: Raw materials, work-in-progress, finished goods.

Prepaid Expenses and Other Current Assets.

b. Non-Current Assets

Property, Plant & Equipment (PPE):

Land (non-depreciable)

Buildings

Machinery (extruders, molds, cutters, mixing units)

Vehicles and Office Equipment

(Depreciation reduces book value annually.)

Intangible Assets: Licenses, patents, or proprietary formulations.

Capital Work-in-Progress: For ongoing plant expansions.

Total Assets = Current Assets + Non-Current Assets

Liabilities

a. Current Liabilities

Accounts Payable: Outstanding to raw material suppliers.

Short-Term Borrowings: Working capital lines or overdrafts.

Accrued Expenses and Taxes Payable.

b. Non-Current Liabilities

Long-Term Debt: Term loans, equipment financing.

Deferred Tax Liabilities: From timing differences in depreciation.

Lease Obligations: If applicable under IFRS/GAAP rules.

Total Liabilities = Current + Non-Current Liabilities

Shareholders’ Equity

Share Capital: Paid-in equity from founders or investors.

Share Premium / Additional Paid-In Capital: Excess over par value.

Retained Earnings: Cumulative net profits retained in the business.

Reserves: General, revaluation, or capital reserves.

Total Equity = Share Capital + Reserves + Retained Earnings

Key Financial Metrics for PVC Manufacturing

- Gross Profit Margin = (Gross Profit / Revenue) × 100

- Operating Profit Margin (EBIT Margin) = (EBIT / Revenue) × 100

- Net Profit Margin = (Net Income / Revenue) × 100

- Return on Assets (ROA) = (Net Income / Total Assets) × 100

- Return on Equity (ROE) = (Net Income / Shareholder Equity) × 100

- Debt-to-Equity Ratio = (Total Debt / Shareholder Equity)

- Inventory Turnover = (COGS / Average Inventory)

- Days Sales Outstanding (DSO) = (Accounts Receivable / Revenue) × 365

When structuring product lines for you PVC manufacturing, it’s important to organize them in a way that aligns with customer needs, market demand, and operational efficiency.

Supporting Schedules

A robust model also includes:

Depreciation Schedule: Per asset class, showing cost, life, accumulated depreciation.

Debt Schedule: Loan drawdowns, repayment, interest expense.

Working Capital Schedule: Movements in inventory, receivables, payables.

Tax Schedule: Current vs. deferred taxes.

CAPEX Schedule: Planned investments and asset commissioning timelines.

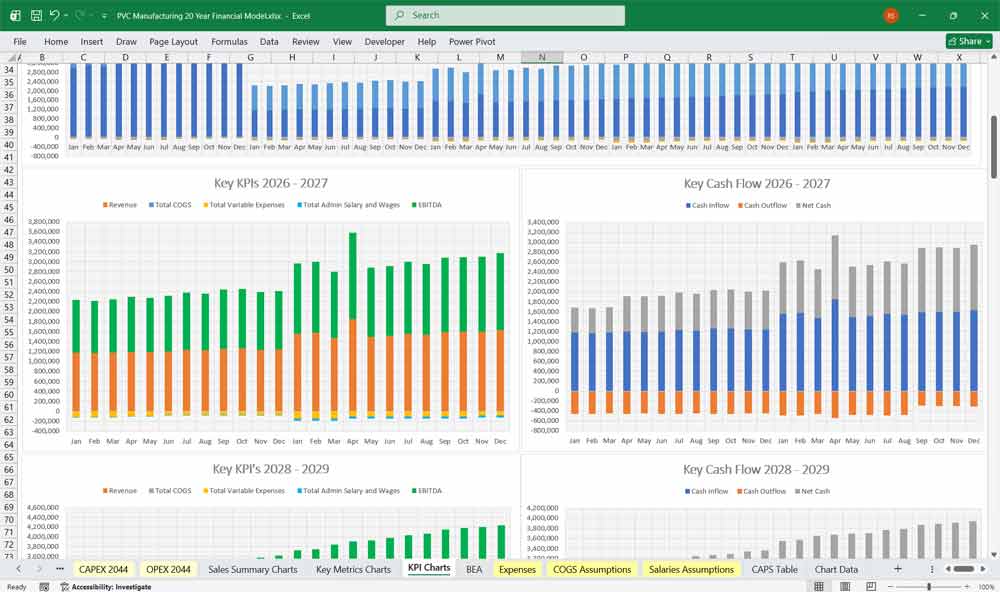

Key Outputs and Analysis

The final part of the financial model produces insights and metrics for decision-making:

EBITDA, EBIT, NOPAT

Free Cash Flow (FCFF and FCFE)

Payback Period, IRR, NPV

Debt Service Coverage Ratio (DSCR)

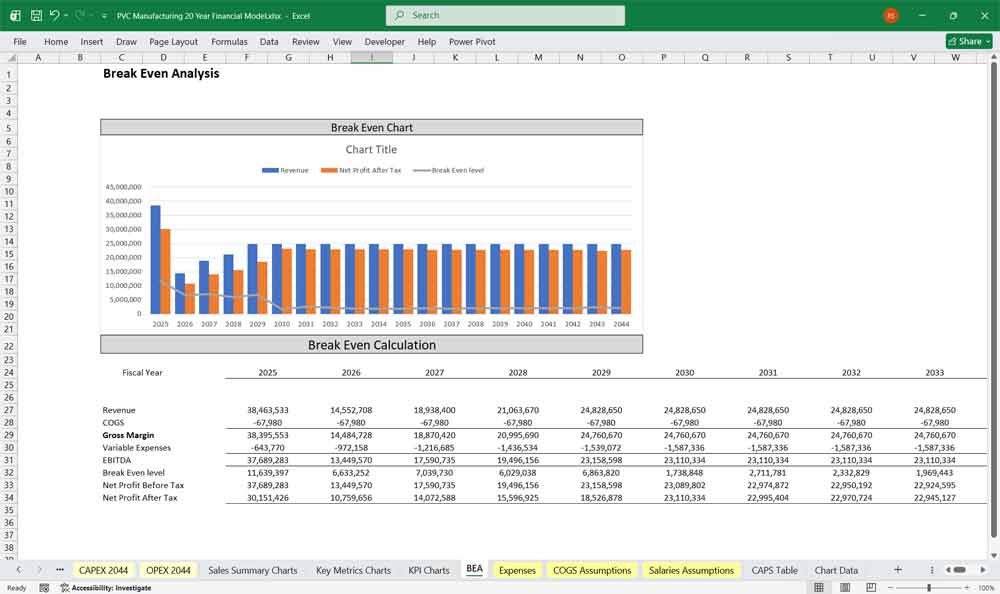

Break-even Analysis

Sensitivity Analysis: Impact of resin cost, selling price, or utilization changes.

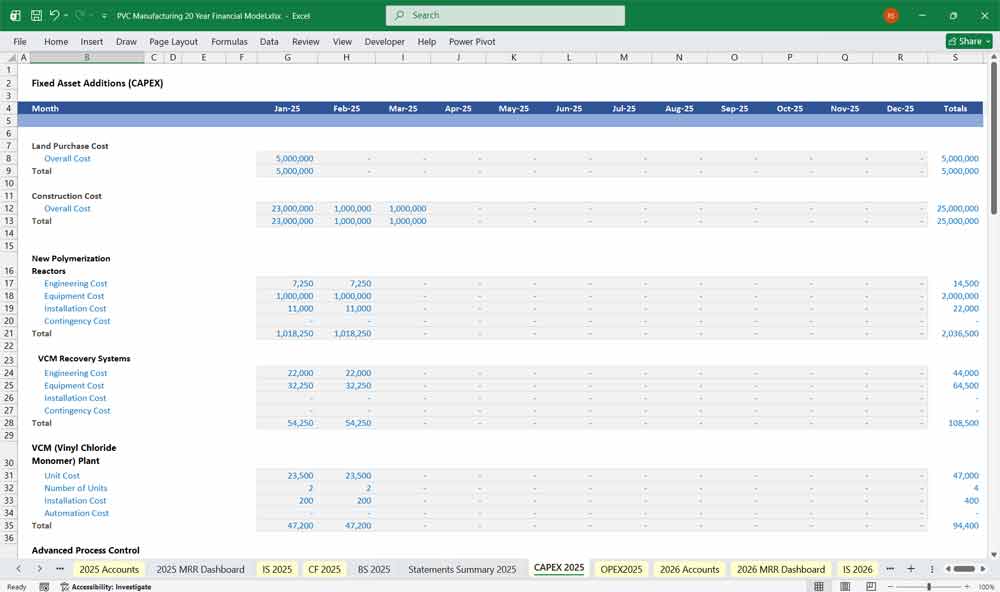

PVC Manufacturing CAPEX Examples In The Model (16 Editable In The Model)

The most significant CAPEX, involves the purchase and installation of an entire new line, including polymerization reactors, VCM recovery systems, and all associated controls to increase overall capacity.

VCM (Vinyl Chloride Monomer) Plant Expansion: Since VCM is the primary raw material, investing in expanding the capacity of the on-site VCM production facility is a major strategic CAPEX to secure supply and reduce costs.

Advanced Process Control (APC) System: Implementing sophisticated software and hardware to automate and optimize the polymerization process, leading to higher consistency, reduced energy consumption, and less raw material waste.

Energy-Efficient Chiller System: Replacing old refrigeration units with modern, high-efficiency chillers used to control the exothermic heat of the polymerization reaction, significantly reducing electricity costs.

Reactor Vessel Replacement/Relining: A major planned overhaul where a key polymerization reactor is either replaced or has its internal glass lining repaired/replaced to ensure integrity and prevent contamination.

PVC Manufacturing OPEX Examples In The Model (10 Editable In The Model)

Vinyl Chloride Monomer (VCM): The primary raw material for making PVC. This is typically the largest and most volatile operational cost, purchased on a continuous basis.

Additives and Compounding Ingredients: Costs for plasticizers (for flexible PVC), heat stabilizers, lubricants, pigments, and fillers that are blended with the PVC resin to create specific compound grades.

Direct Labor Wages & Benefits: Salaries, wages, overtime, and benefits (health insurance, pensions) for production operators, control room technicians, and maintenance crews directly involved in the manufacturing process.

Packaging & Logistics: Expenses for bags, bulk bags (FIBCs), drums, and pallets for finished products, as well as freight and transportation charges to ship products to customers.

Key Financial Ratios & Metrics

- Gross Profit Margin = (Revenue – COGS) / Revenue

- Operating Margin = Operating Profit / Revenue

- EBITDA Margin = (Earnings Before Interest, Taxes, Depreciation, and Amortization) / Revenue

- Current Ratio = Current Assets / Current Liabilities

- Debt-to-Equity Ratio = Total Debt / Shareholder’s Equity

- Return on Investment (ROI) = Net Profit / Investment Cost

Scenario Analysis

- Best Case: High subscription retention, strong retail demand, cost efficiency.

- Base Case: Steady sales growth with manageable costs.

- Worst Case: Supply chain disruptions, high churn, increased competition.

Conclusion

These Excel financial models for PVC manufacturing must balance product variety, cost structure, and revenue channels. By incorporating retail sales, bulk distribution, and a 6-tier subscription model, the business can stabilize cash flow and achieve long-term growth

Download Link On Next Page, view the full model description