Paper Mill Financial Model

Financial Model for a Paper Mill

This very extensive 20 Year Paper Mill Model involves detailed revenue projections, cost structures, capital expenditures, and financing requirements. This model provides a comprehensive understanding of the mill’s financial viability, profitability, and cash flow position. Includes: 20x Income Statements, Cash Flow Statements, Balance Sheets, CAPEX sheets, OPEX Sheets, Statement Summary Sheets, and Revenue Forecasting Charts with the specified revenue streams, BEA charts, sales summary charts, employee salary tabs and expenses sheets. Over 140 spreadsheets of financial data.

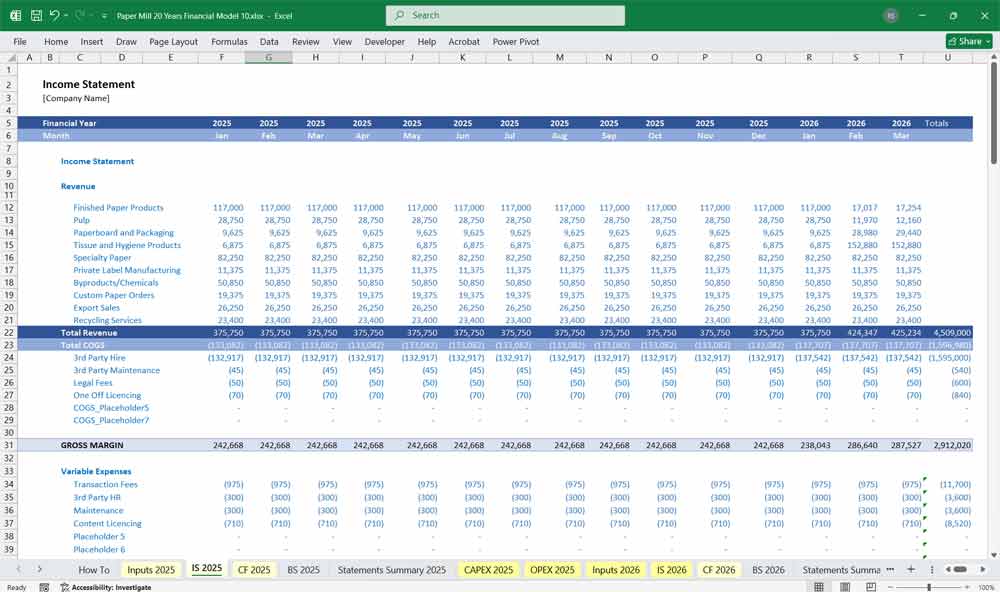

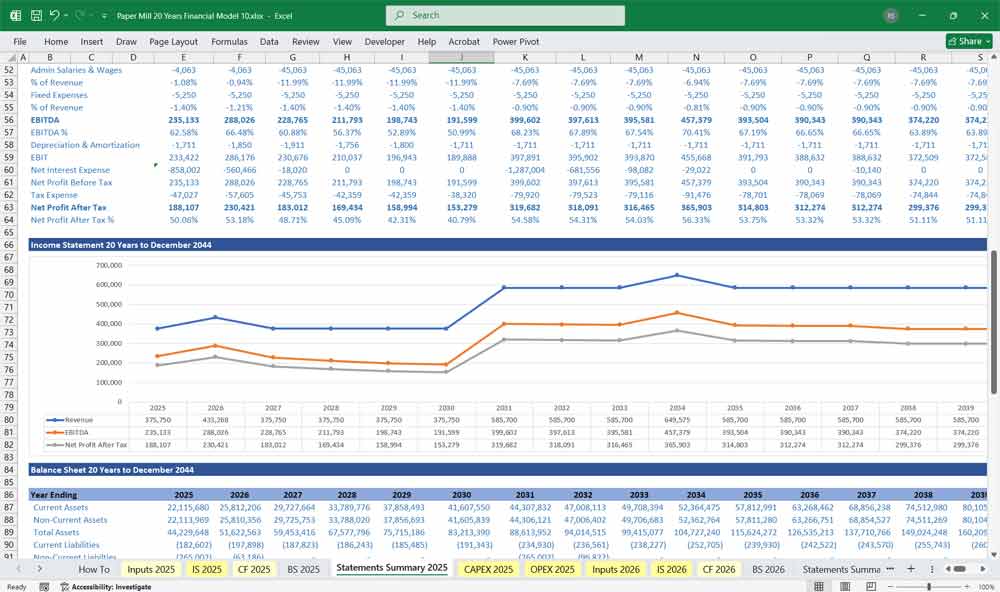

Income Statement

The Income Statement (also known as the Profit and Loss or P&L statement) shows the mill’s profitability over a specific period. It starts with revenue and subtracts expenses to arrive at net income.

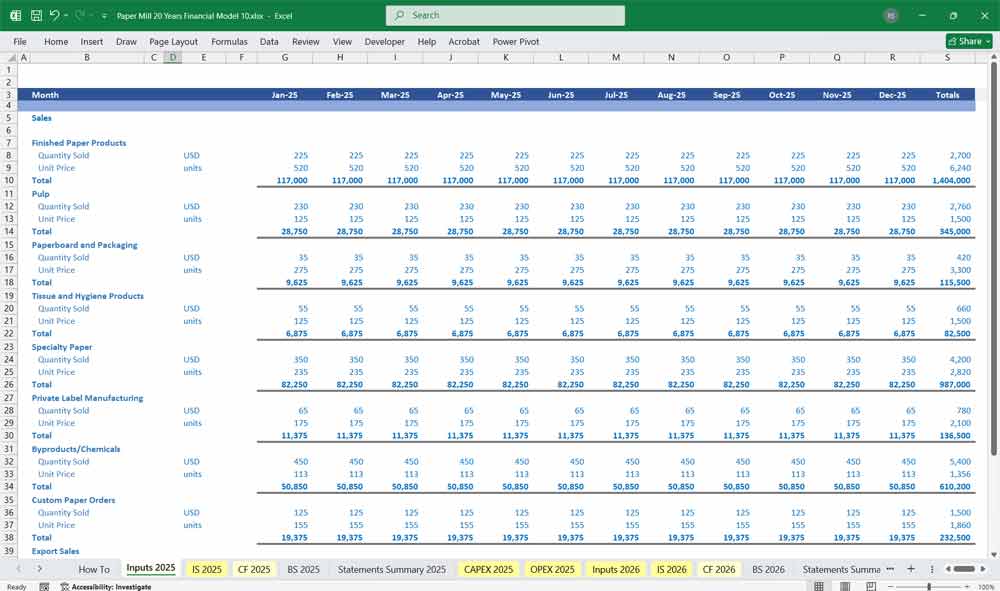

Revenue: This (10 editable sections) forecasts sales based on the mill’s production capacity, the price per ton of paper, and the mix of products (e.g., finished paper products, cardboard, newsprint, fine paper). Assumptions about market demand and pricing trends.

Cost of Goods Sold (COGS): This is the direct cost of producing the paper. It includes the cost of raw materials like wood pulp and recycled paper, chemicals, energy, and direct labor. The model will calculate COGS based on the production volume and the assumed cost per unit of input.

Gross Profit: This is calculated by subtracting COGS from revenue. It represents the profit the mill makes from its core production activities before considering operating expenses.

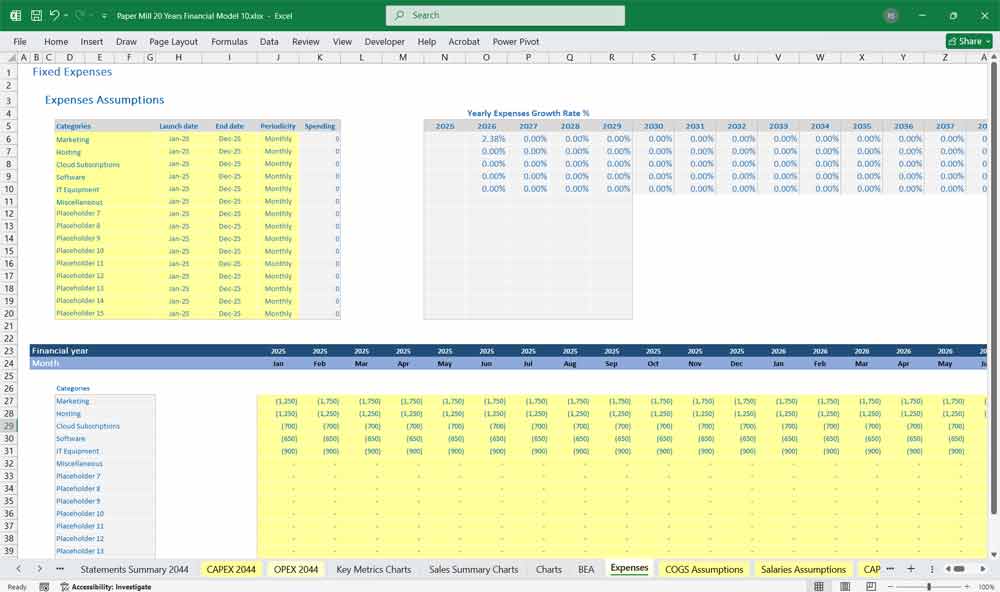

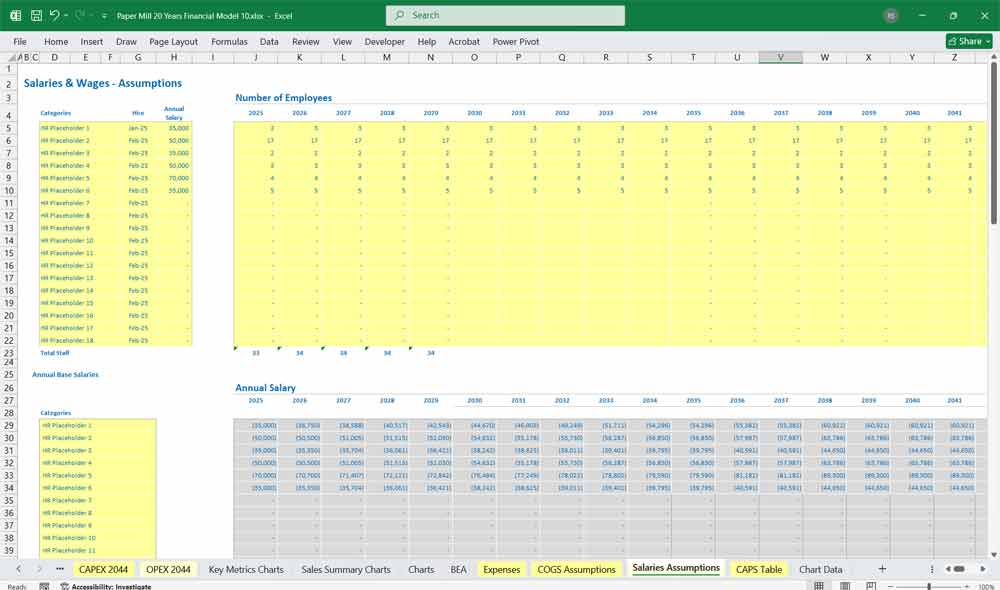

Operating Expenses: These are the costs not directly tied to production, such as selling, general, and administrative (SG&A) expenses. They include salaries for office staff, marketing costs, and rent. The model will often project these as a percentage of revenue or as fixed costs with an annual growth rate.

Depreciation and Amortization (D&A): This is a non-cash expense that accounts for the reduction in value of the mill’s assets, like machinery and buildings, over time. The model will have a separate schedule to calculate D&A based on the useful life of the assets.

Operating Income (EBIT): This is calculated by subtracting operating expenses and D&A from gross profit. It shows the profitability of the mill’s core operations.

Interest Expense/Income: This accounts for the interest paid on debt or earned from investments. The model will have a debt schedule to forecast interest payments.

Taxes: This is the income tax the mill must pay. The model will apply a corporate tax rate to the mill’s earnings before tax.

Net Income: This is the final line on the income statement, representing the mill’s total profit after all expenses and taxes have been deducted.

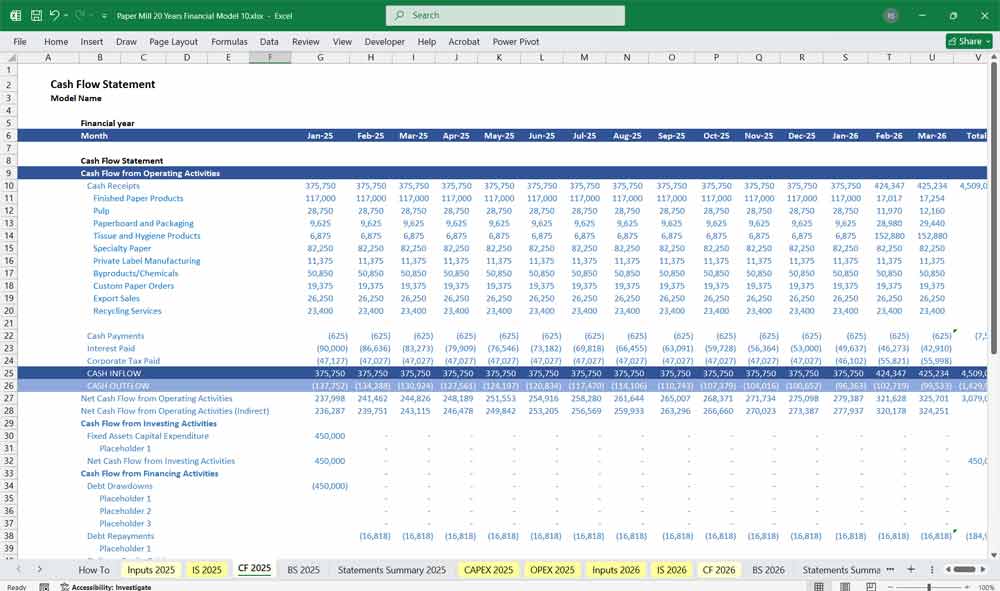

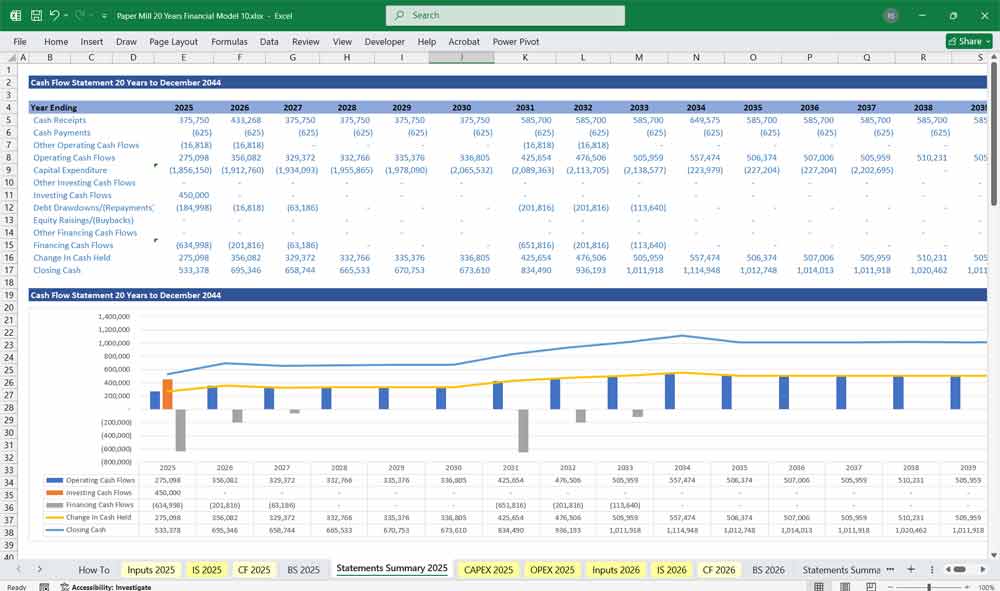

Paper Mill Cash Flow Statement

The Cash Flow Statement tracks the movement of cash into and out of the business. It is crucial for understanding the mill’s liquidity. The statement is divided into three sections: operating, investing, and financing activities.

Cash Flow from Operating Activities: This section begins with net income and adds back non-cash expenses like depreciation and amortization. It also accounts for changes in working capital (e.g., changes in accounts receivable, inventory, and accounts payable). For a paper mill, a significant change in inventory levels can have a big impact on cash flow.

Cash Flow from Investing Activities: This section details the cash spent on or received from investments. For a paper mill, this typically includes capital expenditures (CapEx) for new machinery, building expansions, or asset replacements. The model will have a CapEx schedule based on the mill’s strategic plans.

Cash Flow from Financing Activities: This section covers cash flows related to debt and equity. It includes cash raised from issuing debt or new shares, cash used to repay debt, and cash paid out as dividends to shareholders. The model’s debt schedule and dividend policy will drive these figures.

Net Change in Cash: This is the sum of the cash flows from all three sections. It shows the overall increase or decrease in the mill’s cash balance during the period. The beginning cash balance plus the net change in cash equals the ending cash balance, which flows to the Balance Sheet.

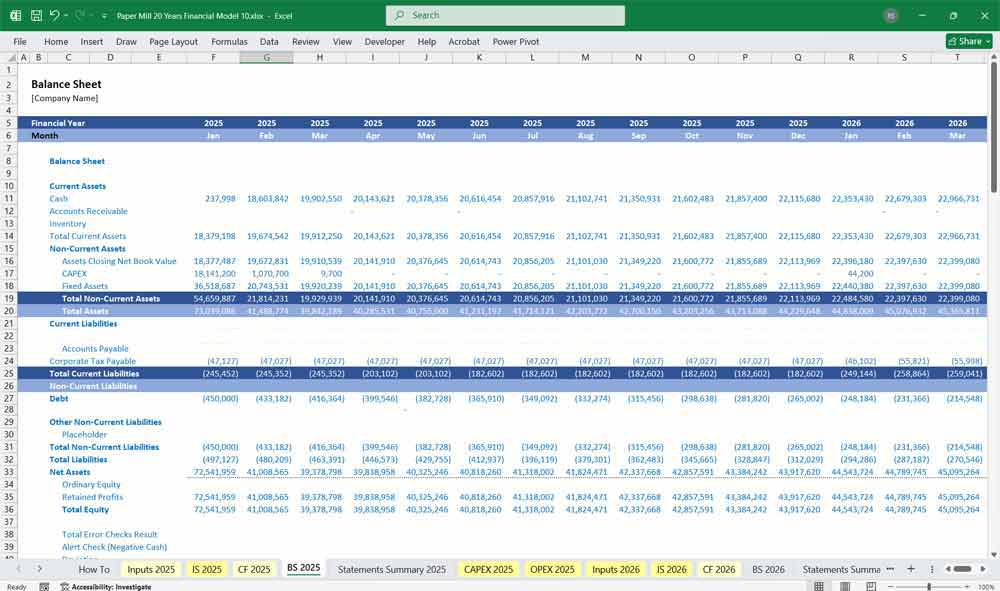

Paper Mill Balance Sheet

The Balance Sheet provides a snapshot of the mill’s financial position at a specific point in time. It follows the fundamental accounting equation: Assets = Liabilities + Equity.

Assets: These are what the mill owns.

Current Assets: These are assets expected to be converted to cash within one year. They include cash, accounts receivable (money owed to the mill by customers), and inventory (raw materials, work-in-progress, and finished paper).

Non-Current Assets: These are long-term assets. For a paper mill, this includes property, plant, and equipment (PP&E), such as the mill building, machinery, and land. The model will track the value of PP&E, accounting for depreciation.

Liabilities: These are what the mill owes to others.

Current Liabilities: These are obligations due within one year, such as accounts payable (money the mill owes to suppliers) and short-term debt.

Non-Current Liabilities: These are long-term obligations, primarily long-term debt used to finance the mill’s operations and expansion.

Equity: This represents the owners’ stake in the mill.

Common Stock: The value of shares issued to investors.

Retained Earnings: This is the accumulated net income of the mill that has not been paid out as dividends. The model updates retained earnings each period by adding net income and subtracting dividends.

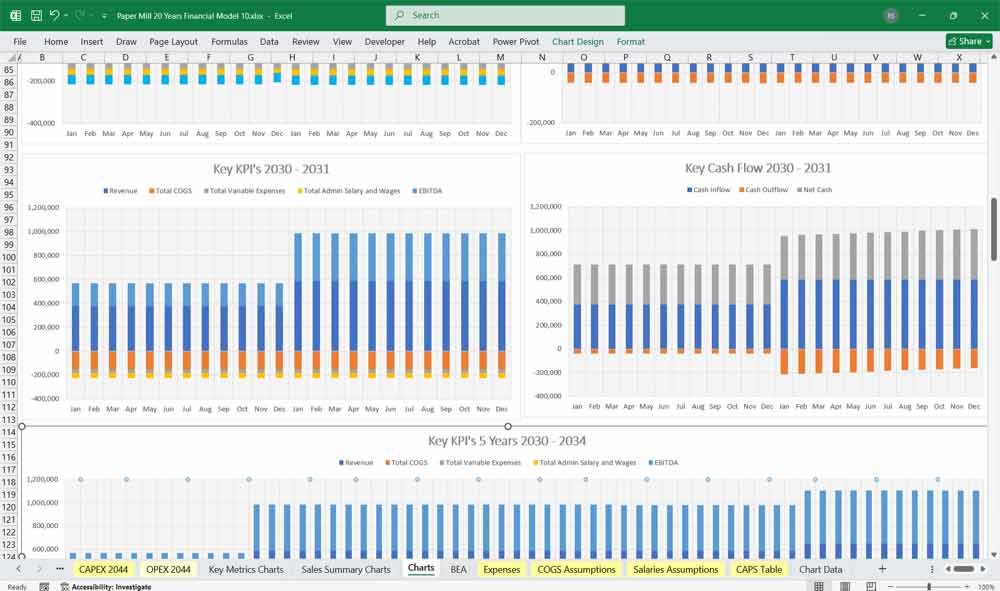

Key Financial Metrics for a Paper Mill

Revenue Metrics

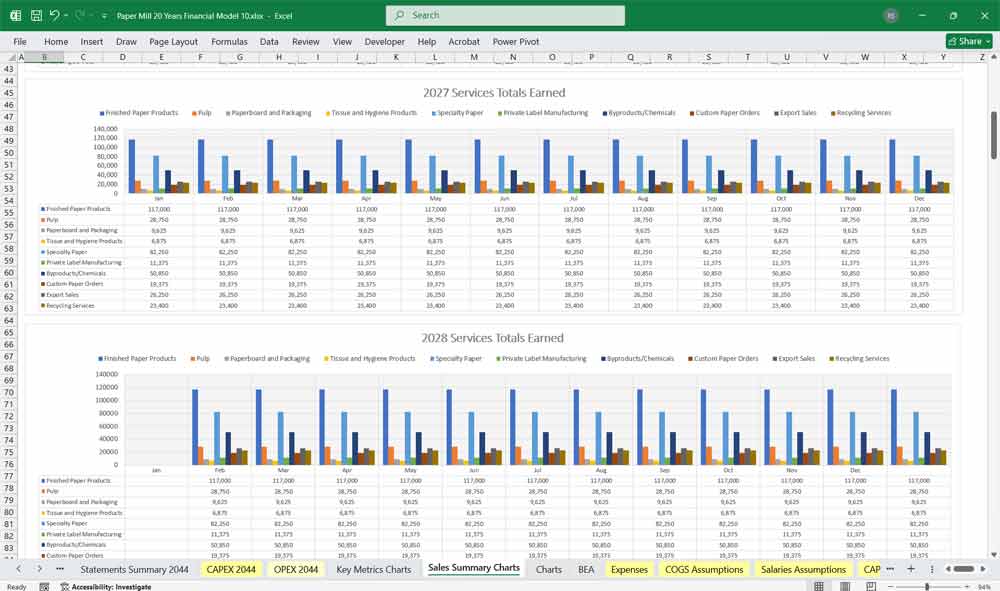

Predictable income from ongoing products like Finished Paper Products, Pulp, Cardboard and Custom Paper Orders.

20 Years provides a long-term revenue outlook.

Income generated per ton, indicating revenue efficiency.

Income generated per quantity, indicating facility efficiency.

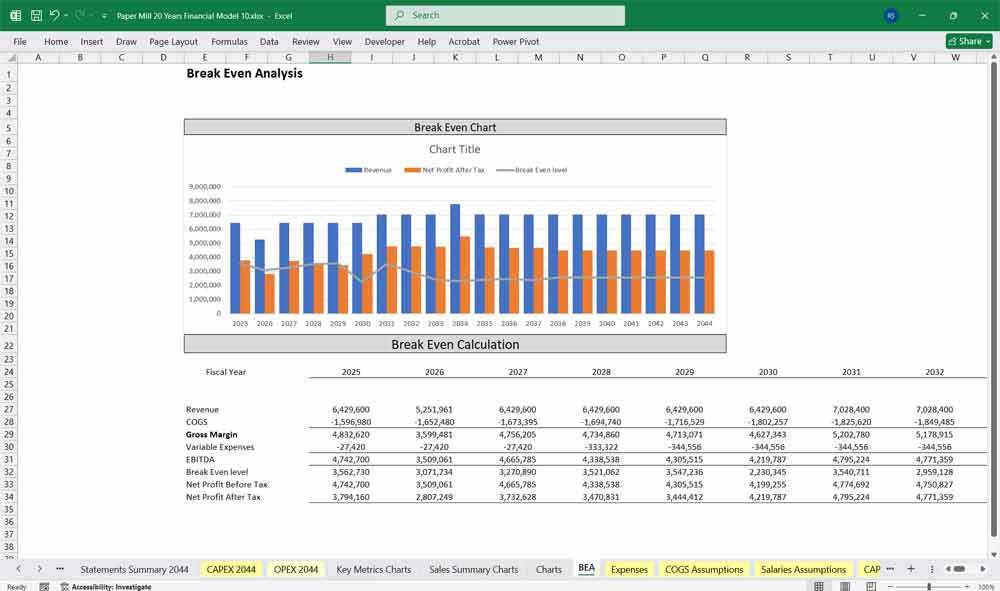

Cost Metrics

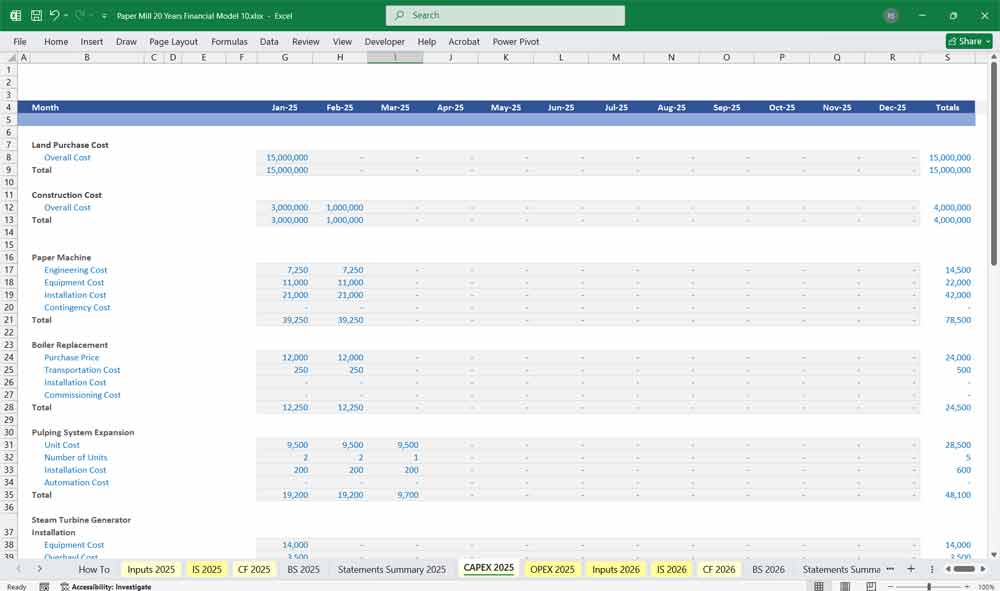

Capital Expenditure (CapEx): Initial investment in infrastructure, machinery, and construction.

Operational Expenditure (OpEx): Ongoing costs for maintenance, utilities, staffing, and logistics.

Power Usage Effectiveness (PUE): Ratio of total energy used to energy delivered to mill equipment (lower PUE = better efficiency).

Benefits of Using a 20-year Paper Mill Financial Model

A 20-year financial model for a paper mill offers several key benefits, primarily because of the long-term nature of the industry’s assets and market cycles. First, it enables long-range strategic planning. A mill’s assets, like machinery and buildings, have a very long useful life, often exceeding two decades. A 20-year model allows management to plan for major capital expenditures, like a new paper machine or a plant expansion, and understand the long-term impact on profitability and cash flow. It helps them to visualize and prepare for the financial implications of their strategic vision far into the future.

Paper Mill and Budget Planning

Second, it’s crucial for capital budgeting and investment analysis. Paper mills are highly capital-intensive, requiring significant upfront investment. A 20-year model allows for a detailed Net Present Value (NPV) and Internal Rate of Return (IRR) analysis of large projects, such as a new pulping line or a modernization program. By forecasting cash flows over the entire project lifecycle, the model helps determine if the investment is financially viable and will generate an adequate return for shareholders.

Dept Financing For Your Paper Mill

Third, a long-term model is essential for long-term debt financing. Lenders and investors need to see a detailed forecast of the mill’s ability to service its debt over the life of the loan. Since paper mill debt can have terms of 10 to 20 years, a short-term model is insufficient. The 20-year model demonstrates a clear plan for cash flow generation, a stable balance sheet, and the ability to meet all interest and principal payments, which is vital for securing favorable financing terms.

20-year Risk Assessment For Your Paper Mill

A thorough risk assessment and sensitivity analysis. The paper industry is subject to cyclical fluctuations in demand and volatile input costs (e.g., wood pulp, energy). A 20-year model allows management to run various scenarios, such as a prolonged market downturn, a significant increase in energy prices, or a change in environmental regulations. By understanding the potential impact of these risks on the mill’s financials, management can develop contingency plans and build a more resilient business.

20-year Valuation Of The Paper Mill

When a potential buyer or investor is assessing a paper mill, they need to understand its long-term earnings potential. A 20-year Discounted Cash Flow (DCF) model, built on the detailed financial forecast, provides a robust valuation of the business. It captures the value of the mill’s long-life assets and its ability to generate sustainable cash flows over an extended period, which is more accurate than a shorter-term valuation.

Paper Mill Succession

A 20-year model is an excellent tool for planning for retirement and succession. As the mill’s long-term liabilities, such as pension obligations and environmental cleanup costs, often span decades, the model helps management plan for these financial commitments. It also helps to project the value of the business for succession planning purposes, giving owners and key stakeholders a clear picture of what the business will be worth in the future.

Final Notes on the Financial Model

This 20 Year Paper Mill Financial Model must focus on balancing capital expenditures with steady revenue growth from reliable revenue-raising services. By optimizing operational costs, and power efficiency, and maximizing high-margin services like Finished Paper Products, Pulp, Cardboard and Custom Orders, this 20-year model ensures sustainable profitability and cash flow stability.

Download Link On Next Page