Mineral Water Company Financial Model

Financial Model For A Mineral Water Company

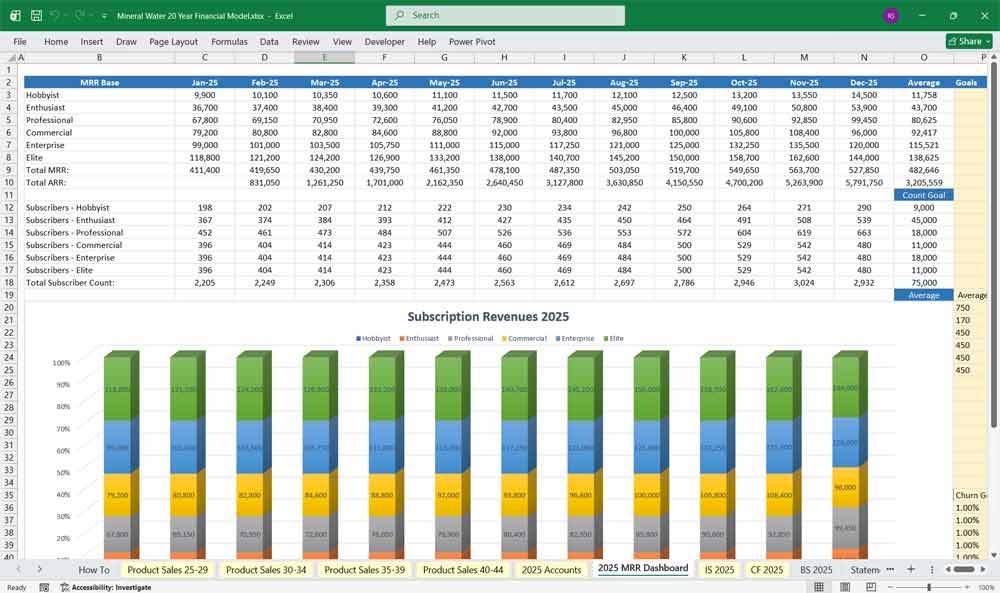

This financial model for a mineral (bottled water) company are built to assess profitability, cash flow, and financial health. It accounts for production costs, sales projections, operational expenses, capital investment, and financing. It includes detailed scenarios for two product line variations (80 SKUs) and a 6-tier subscription model Add-On.

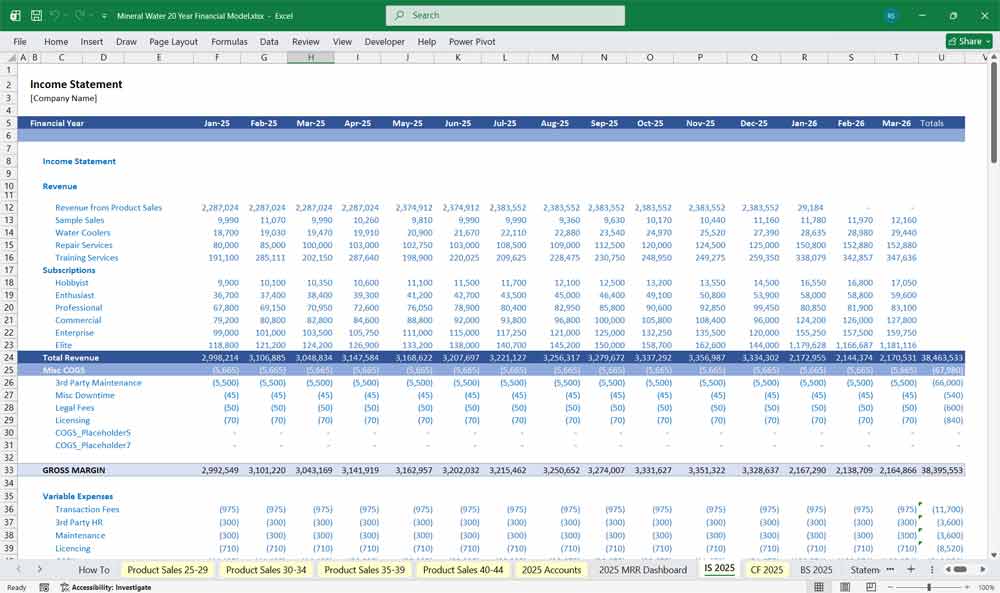

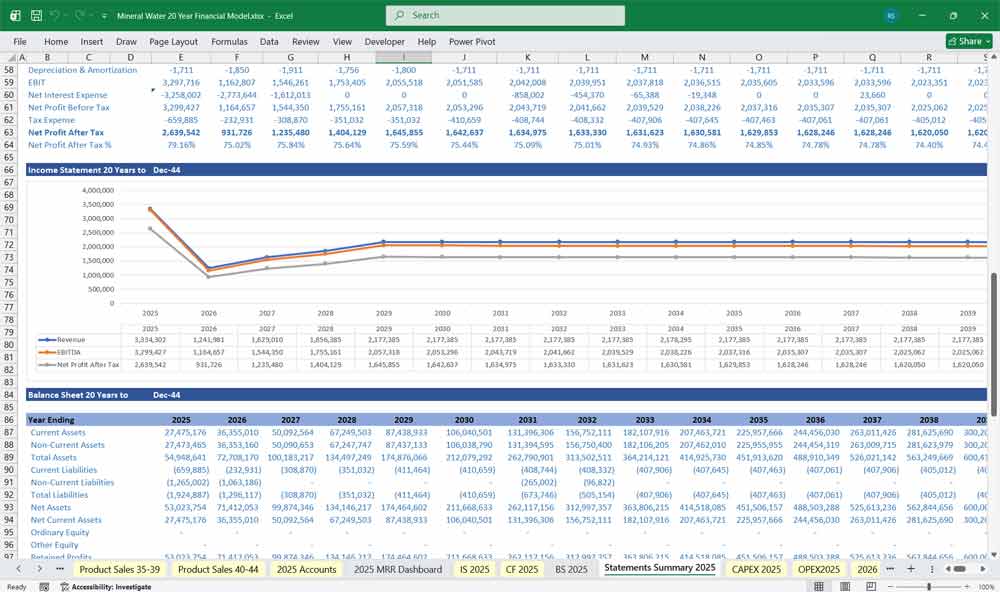

Income Statement (Profit & Loss Statement)

The income statement should reflect all revenue streams and all operating and non-operating costs. Include the following sections:

A. Revenue

For each product line:

Units sold per year

Price per unit

Total revenue per product line

Discounts, promotions, and trade marketing deductions

Net Revenue

Revenue should be driven by:

Market growth

Capacity constraints

Price adjustments due to inflation or positioning

Channel mix (retail, wholesale, horeca, exports)

B. Cost of Goods Sold (COGS)

Break COGS into detailed components:

Raw water extraction costs

Filtration and purification inputs

Plastic bottle or glass container costs

Caps, labels, and packaging materials

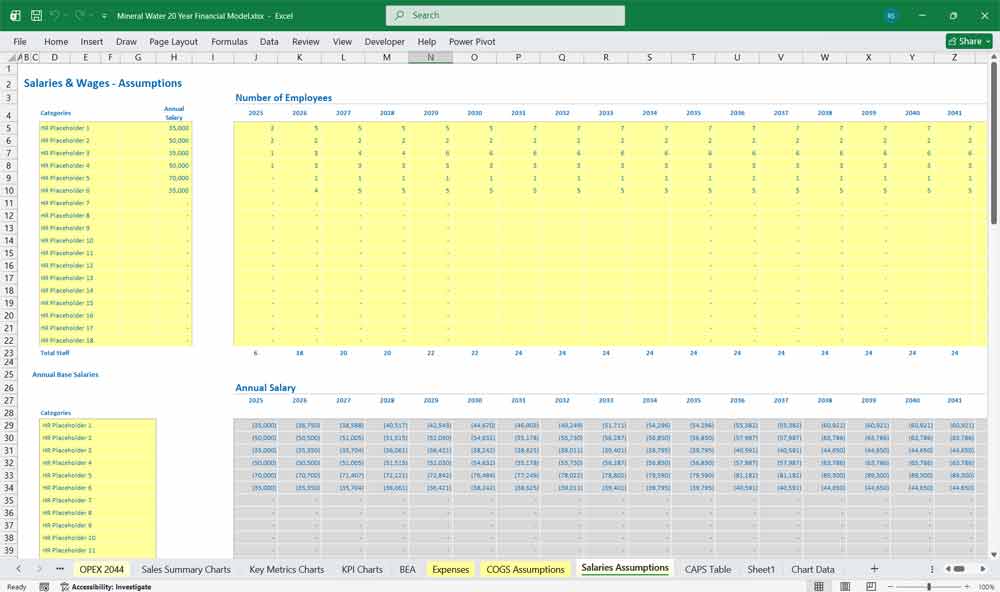

Direct labor (operators, supervisors)

Utilities (electricity for pumps, CO₂ for carbonation if applicable)

Maintenance and consumables

Factory overhead allocations

Gross Profit = Net Revenue – COGS

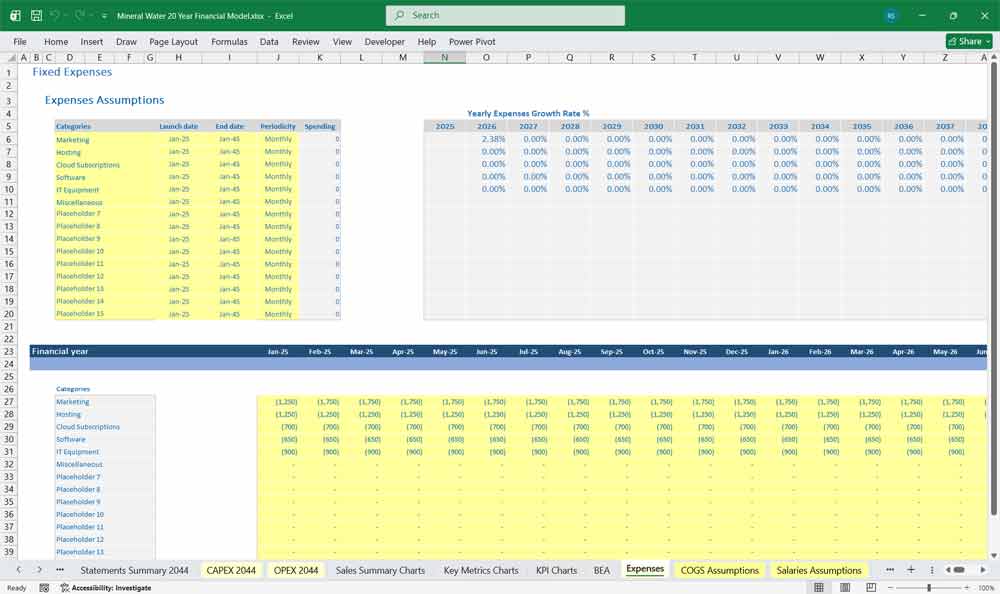

C. Operating Expenses

Selling & Distribution Expense

Marketing and advertising

Trade marketing and promotional allowances

Transportation, logistics, warehousing

Sales team salaries and commissions

General & Administrative Expenses

Salaries for back office

Professional fees

Office rent and utilities

IT, insurance, compliance

Research & Development (optional)

Operating Profit = Gross Profit – Operating Expenses

D. Depreciation & Amortization

Depreciation of bottling lines

Trucks, warehouse equipment

Buildings and improvements

Amortization of licenses or patents

E. Financial Expenses

Interest on debt

Bank charges

FX impact (if relevant)

F. Taxes

Corporate income tax based on taxable income

G. Net Income

Net Income = Operating Profit – Interest – Taxes

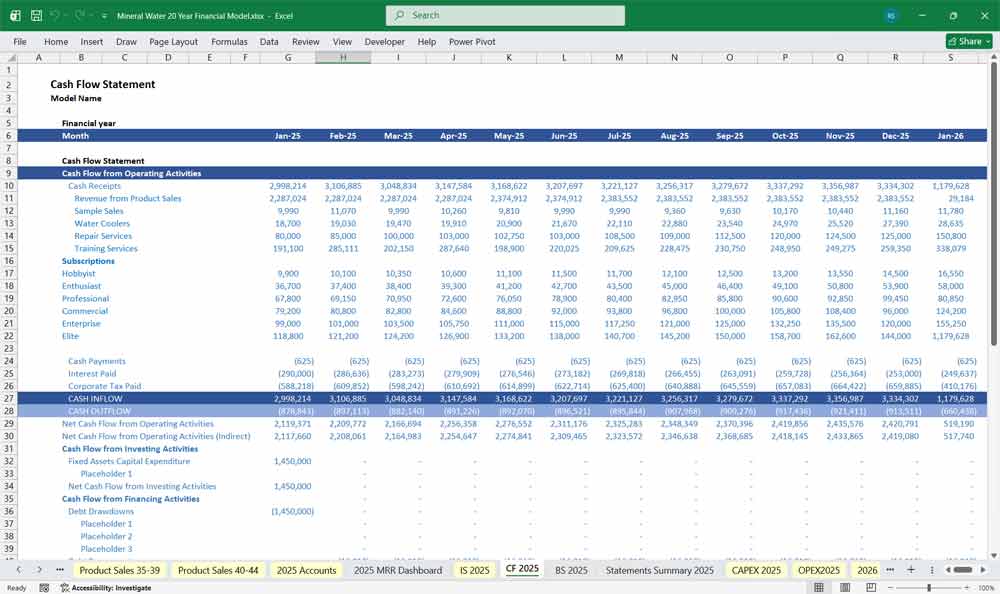

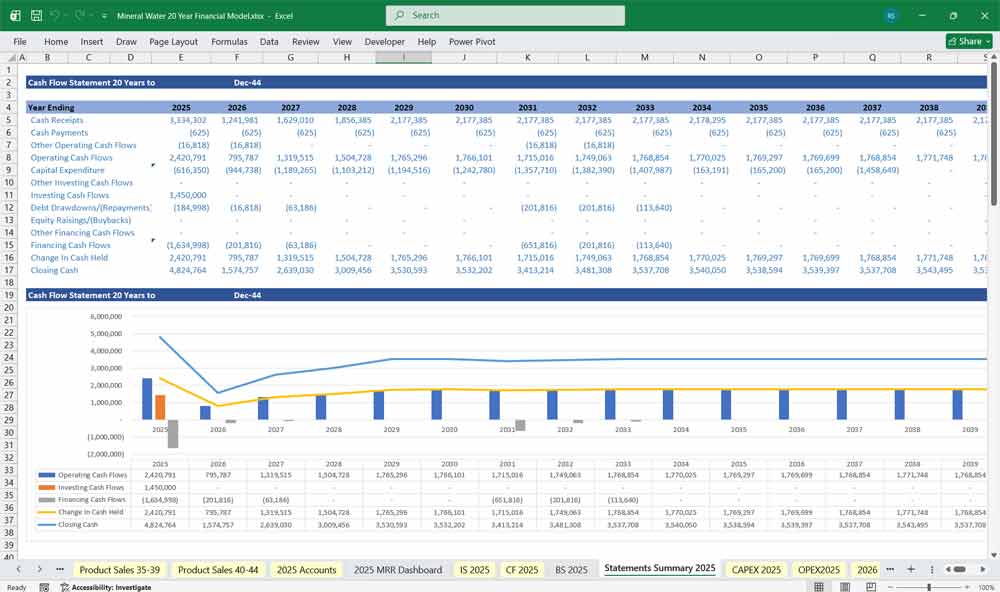

Mineral Water Company Cash Flow Statement

The cash flow statement should follow standard direct or indirect reporting. Recommended: Indirect method.

A. Cash Flow from Operating Activities

Start with Net Income

Add back non-cash charges (depreciation, amortization)

Adjust for working capital changes:

Increase or decrease in accounts receivable

Increase or decrease in inventory (raw materials, finished goods)

Increase or decrease in accounts payable

Other operating adjustments (warranty provisions, bad debt allowances)

Operating Cash Flow = Net Income + Non-Cash Charges + Working Capital Adjustments

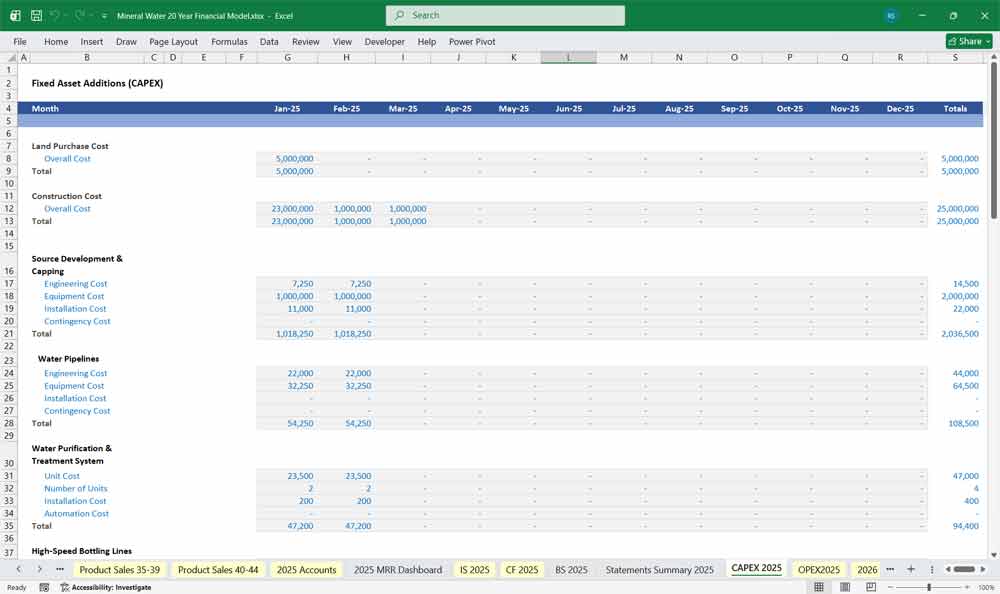

B. Cash Flow from Investing Activities

Capital expenditures:

New production lines

Additional storage tanks

New trucks or forklifts

Water source development (wells, pumps)

Purchase or disposal of fixed assets

Investing Cash Flow = Capital Expenditures – Proceeds from Asset Sales

C. Cash Flow from Financing Activities

New debt issuance

Debt repayments

Equity injections

Dividend payments

Financing Cash Flow = Net Borrowing + Equity Raised – Dividends

D. Net Cash Position

Opening cash balance

Net change in cash

Ending cash balance

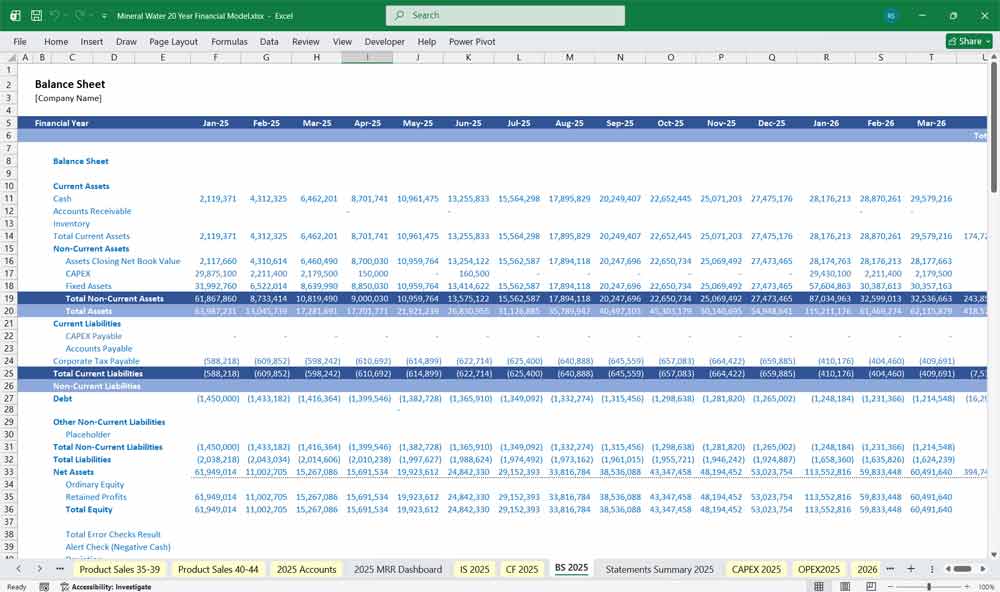

Mineral Water Company Balance Sheet

A. Assets

Current Assets

Cash

Accounts receivable (based on DSO)

Inventory:

Raw materials (bottles, labels, caps)

Finished goods (water bottles)

Spare parts and consumables

Prepaid expenses (insurance, rent)

Non-Current Assets

Property, plant & equipment (PP&E):

Water extraction equipment

Filtration and bottling lines

Warehouses and office buildings

Vehicles

Intangible assets:

Brand development

Permits and licenses

Accumulated depreciation

B. Liabilities

Current Liabilities

Accounts payable

Accrued expenses

Short-term debt or current portion of long-term debt

Taxes payable

Long-Term Liabilities

Bank loans

Bonds (if applicable)

Lease obligations

C. Equity

Owner’s equity

Retained earnings

Share capital

Additional paid-in capital

Balance Sheet equation:

Assets = Liabilities + Equity

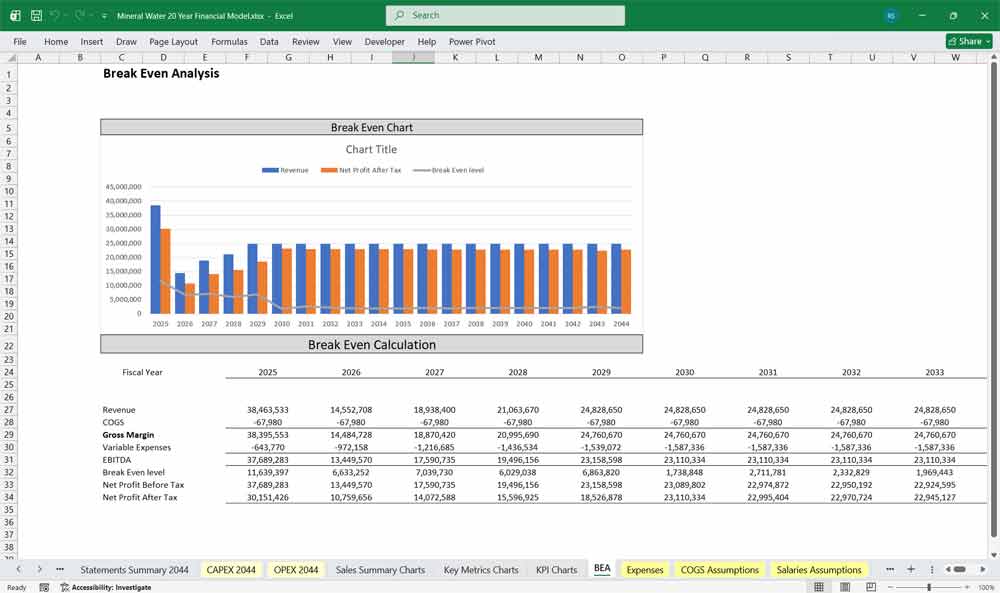

Key Financial Metrics for a Mineral Water Company

Core Model Structure

Assumptions & Drivers

Market demand growth rates

Production capacity by line and plant

Selling prices by product

Cost assumptions (raw materials, packaging, labor, utilities)

Distribution channel mix and logistics costs

Capital expenditure timeline

Depreciation method and useful life of assets

Working capital cycle (DSO, DPO, inventory days)

Financing terms (equity, debt, interest rate, repayment schedule)

Tax rate

Product Line Revenue Model

Production volume

Sales volume (after scrap, losses)

Pricing by SKU

Direct costs per SKU

Integrated Financial Statements

Income Statement

Cash Flow Statement

Balance Sheet

Valuation & Outputs (optional)

NPV, IRR

Payback period

Scenario & sensitivity analysis

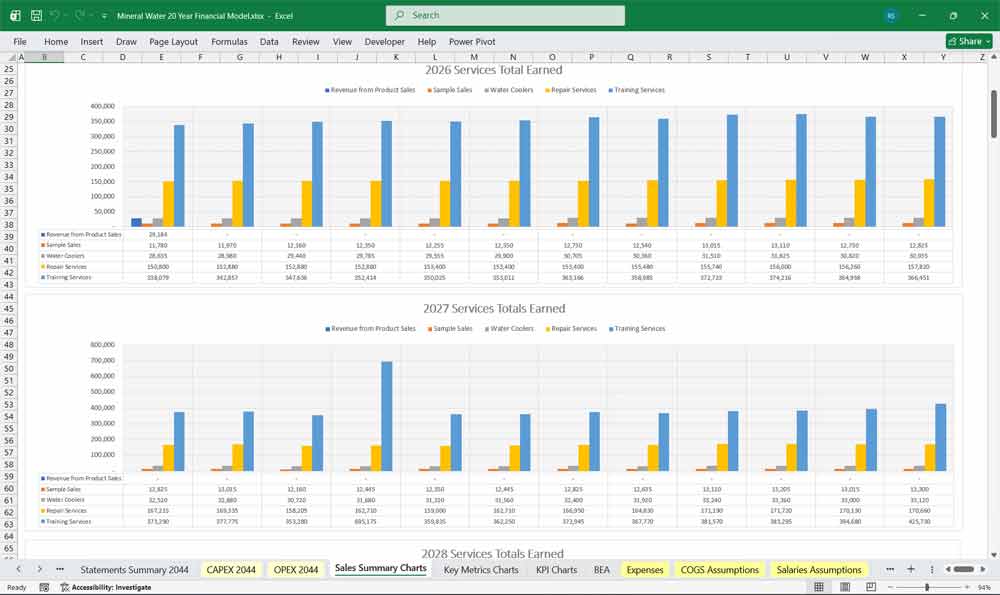

Mineral (Bottled Water) Company Product Line Section (80 Product Lines)

A mineral water company with extensive variety might have up to 80 SKUs. These can be grouped into categories:

A. Editable Product Line Structure Description

For each product line, describe the following:

Product Identification

SKU name (e.g., “Still Water 500ml”, “Sparkling Water 1L Premium Glass”, etc.)

SKU category (still, sparkling, flavored, vitamin-enhanced, premium glass, multipacks)

Packaging

Bottle material (PET or glass)

Bottle size (200ml–2L)

Cap type (screw, sport cap)

Label type (paper, shrink sleeve)

Pricing Strategy

Factory price

Retail recommended price

Channel-specific pricing

Production Details

Production line assigned

Production cost per unit (materials + labor + utilities)

Expected yield (accounting for losses)

Volume Forecast

Monthly and annual sales volume

Channel distribution mix

Revenue Contribution

Annual revenue per SKU

% of total revenue

Direct Costs Per SKU

Bottle cost

Cap cost

Label cost

Variable labor cost

Utilities cost per unit

Gross Margin Per SKU

B. Purpose of Product Line Section

Identifies high-margin vs low-margin SKUs

Supports strategic decisions: discontinuations, expansions, packaging redesign, or premium repositioning

Tracks capacity utilization by product type

C. Examples of SKU Categories (Total of 80)

You would structure the model so these 80 are represented individually. Typical categories include:

Still Water PET (20 SKUs across sizes)

Still Water Glass (10 SKUs)

Sparkling PET (10 SKUs)

Sparkling Glass Premium (15 SKUs)

Flavored Water PET (15 SKUs)

Enhanced/Vitamin Water (10 SKUs)

Each is modeled individually but rolled up into the revenue and COGS sections.

Key Financial Ratios & Metrics

- Gross Profit Margin = (Revenue – COGS) / Revenue

- Operating Margin = Operating Profit / Revenue

- EBITDA Margin = (Earnings Before Interest, Taxes, Depreciation, and Amortization) / Revenue

- Current Ratio = Current Assets / Current Liabilities

- Debt-to-Equity Ratio = Total Debt / Shareholder’s Equity

- Return on Investment (ROI) = Net Profit / Investment Cost

Scenario Analysis

- Best Case: High subscription retention, strong retail demand, cost efficiency.

- Base Case: Steady sales growth with manageable costs.

- Worst Case: Supply chain disruptions, high churn, increased competition.

Conclusion

This Excel financial model for a mineral (bottled water) company balances product variety, cost structure, and revenue channels. By incorporating retail sales, bulk distribution, and a 6-tier subscription model, your business can stabilize cash flow and achieve long-term growth

Download Link On Next Page, view the full model description