20 year Flour Mill Financial Model

20-Year Financial Model for a Flour Mill

A very extensive 20 Year Flour Mill Model involves detailed revenue projections, cost structures, capital expenditures, and financing needs. This model provides a thorough understanding of the financial viability, profitability, and cash flow position of you mill. Includes 20x Income Statements, Cash Flow Statements, Balance Sheets, CAPEX sheets, OPEX Sheets, Statement Summary Sheets, and Revenue Forecasting Charts with editable revenue streams, BEA charts, sales summary charts, employee salary tabs and expenses sheets. Over 140 spreadsheets of financial data to monitor.

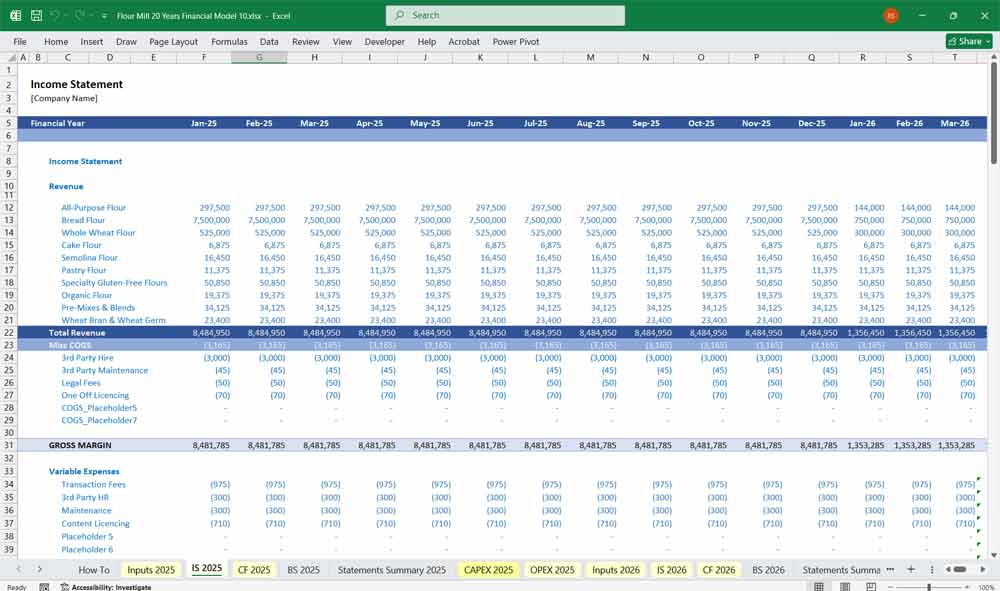

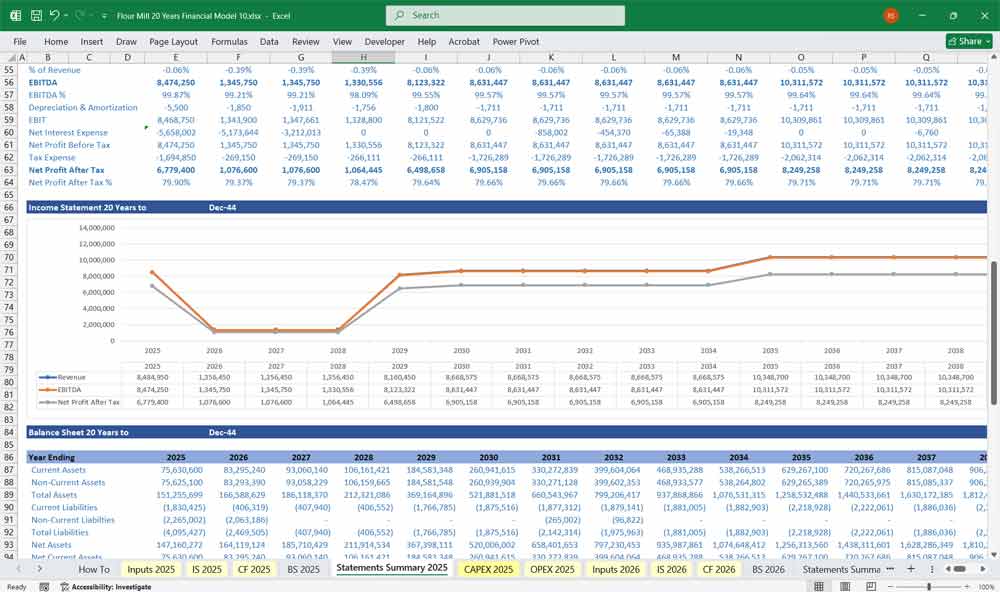

Income Statement (P&L)

This statement shows the profitability of the flour mill.

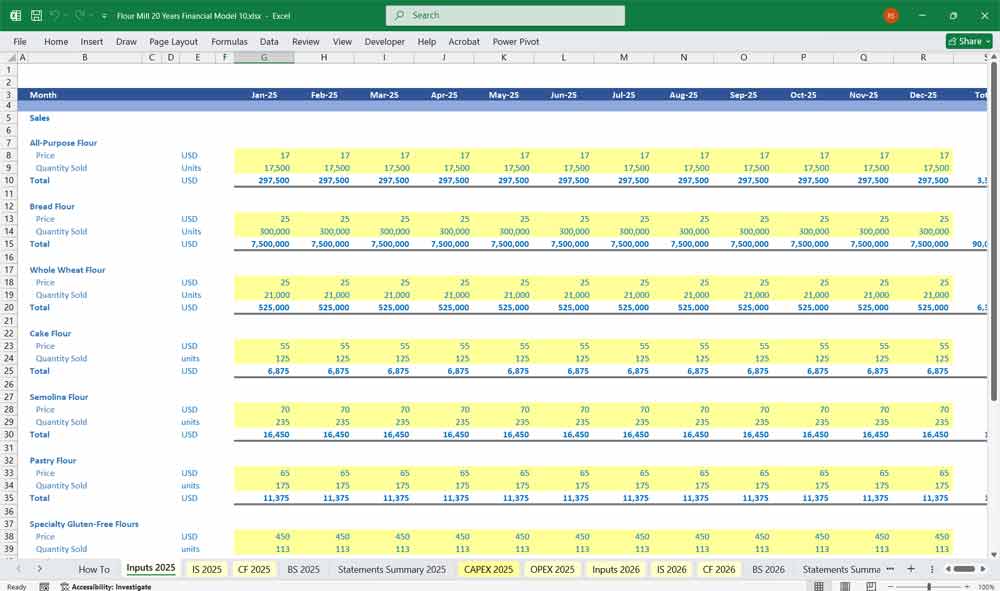

Revenue

Production Capacity: Total mill capacity (tons of wheat per day × working days).

Utilization Rate: % of capacity actually used (e.g., 70–90% depending on maturity).

Output Yield: Flour extraction rate (e.g., 70–75% of input wheat becomes flour; byproducts include bran).

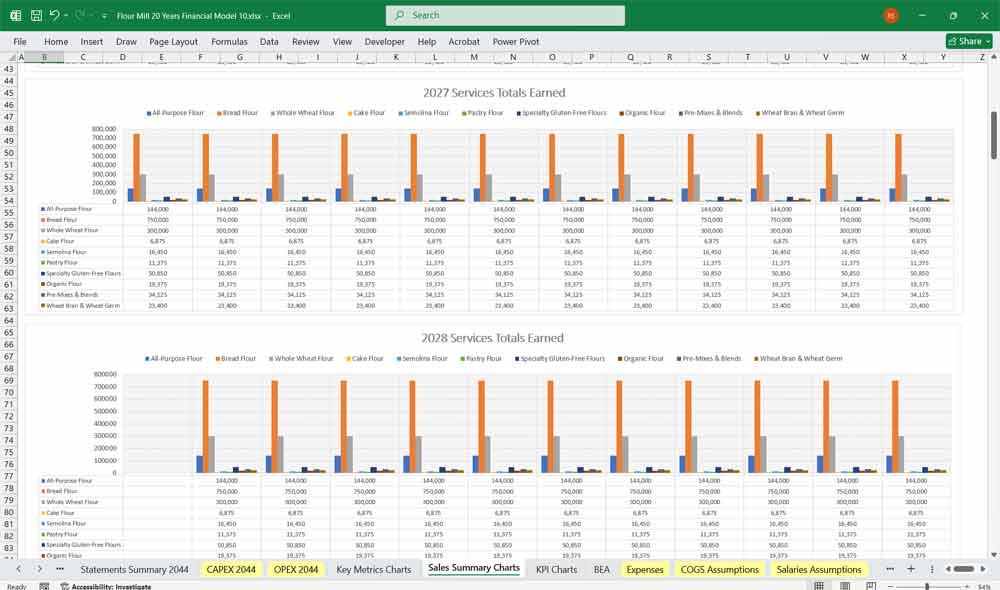

Product Mix:

Flour (main revenue)

Byproducts: Bran, germ, semolina (can be sold separately)

Selling Price: Assumed per ton/kg for flour and byproducts.

Total Revenue = (Flour output × price) + (Byproducts × price).

Cost of Goods Sold (COGS)

Raw Material (Wheat Purchase Cost): The single largest cost (often 65–75% of revenue).

Processing & Milling Costs:

Power & fuel consumption (electricity for rollers, gas for boilers, etc.)

Packaging costs (bags, labels, etc.)

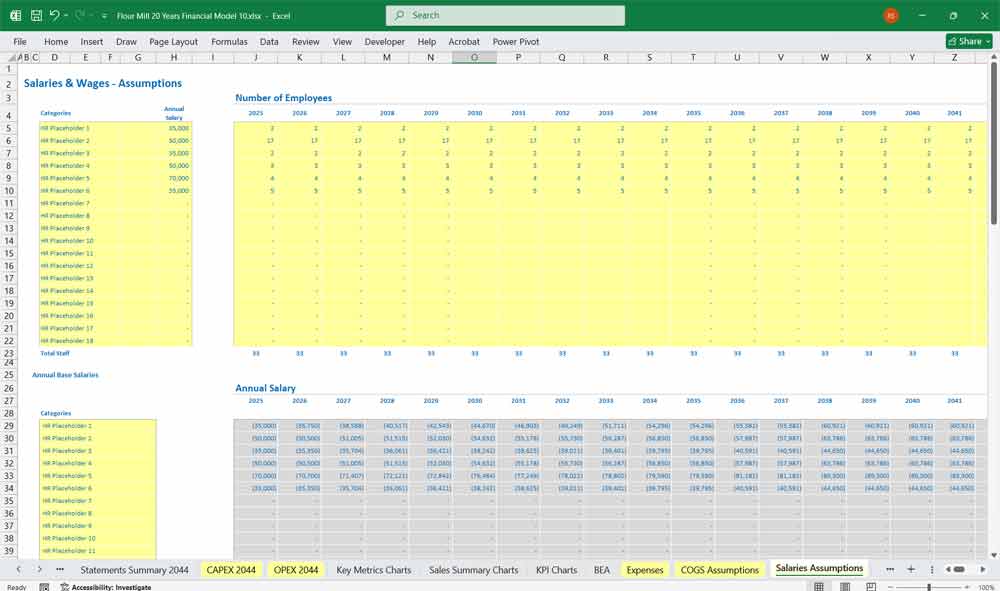

Direct labor (operators, supervisors, quality control).

Maintenance & Consumables: Spare parts, lubricants, repairs.

Freight & Transportation: Inbound wheat transport + outbound flour delivery.

Depreciation (factory equipment).

Gross Profit = Revenue – COGS

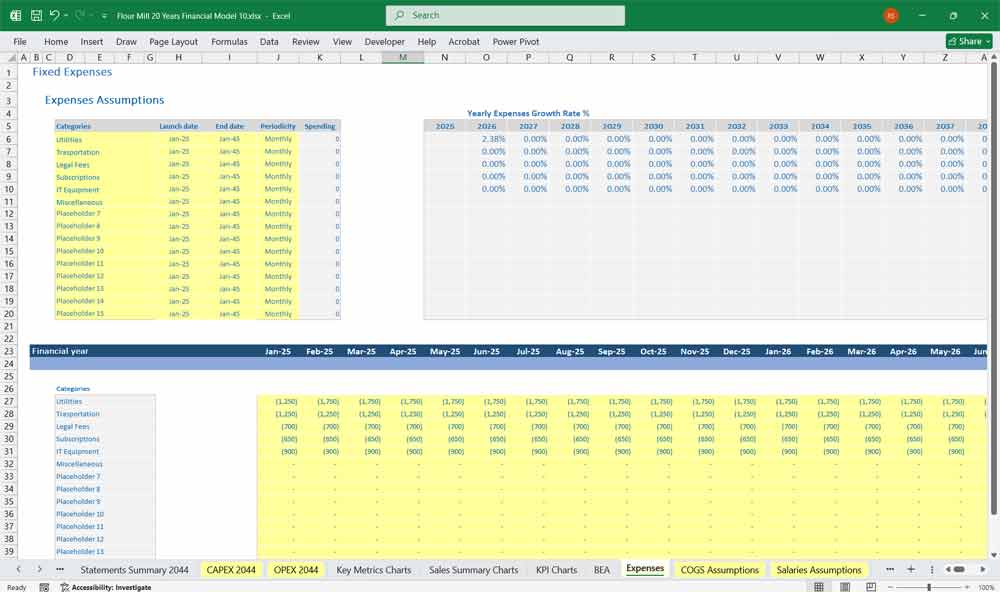

Operating Expenses (OPEX)

Selling & distribution expenses (sales team, marketing, commissions).

Administrative expenses (salaries, office overhead, IT, insurance).

Professional fees (audit, compliance).

Miscellaneous.

EBITDA = Gross Profit – OPEX

Other Items

Depreciation & amortization (if not included above).

Finance costs (interest on loans).

Tax expense (based on jurisdiction).

Net Income = EBITDA – Depreciation – Interest – Taxes

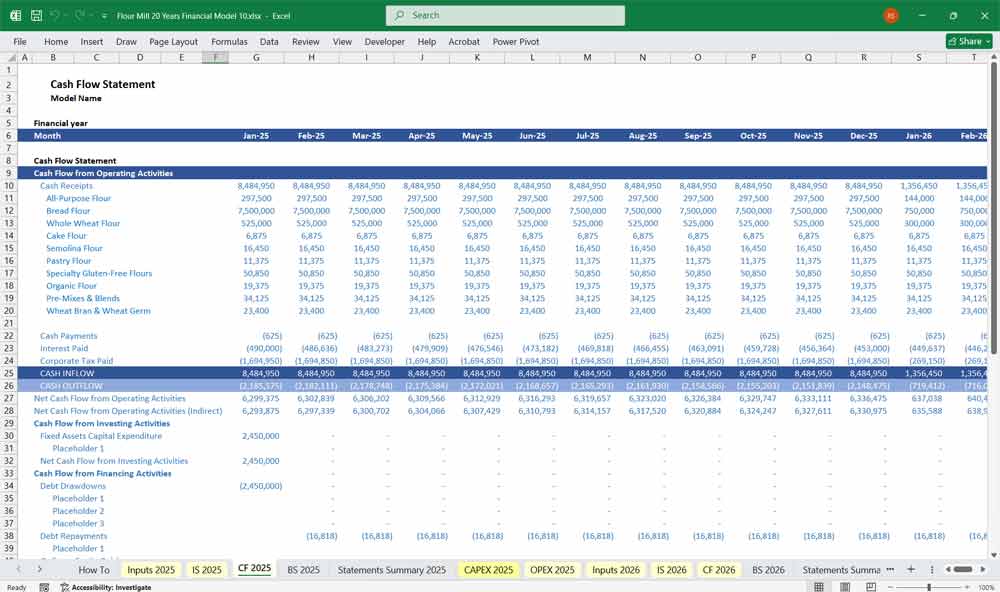

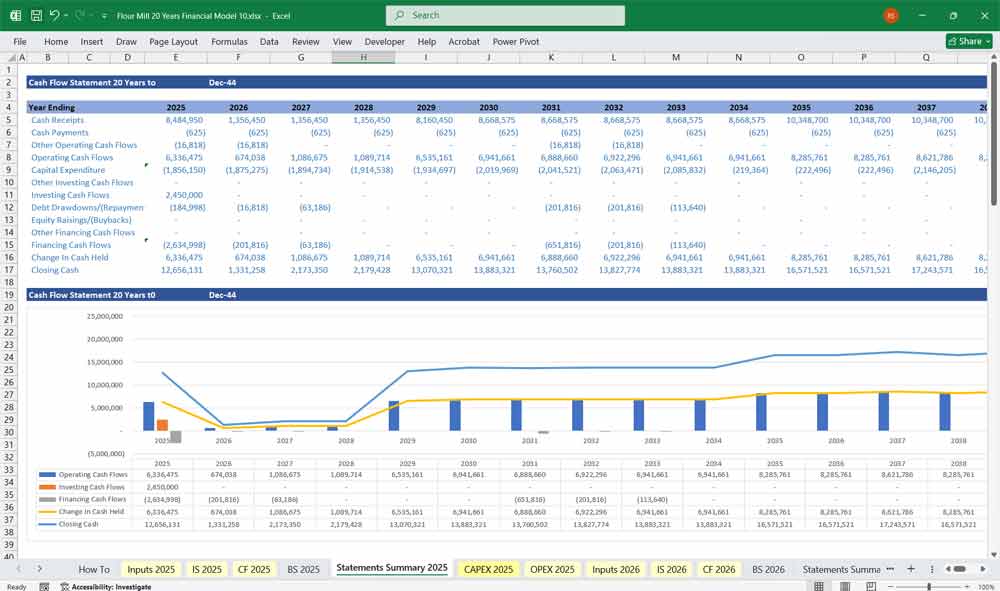

Flour Mill Cash Flow Statement

Tracks the actual movement of cash, separated into operating, investing, and financing activities.

Cash Flow from Operations

Net Income (from P&L).

Add back: Non-cash charges (Depreciation, Amortization).

Adjust for changes in Working Capital:

Inventory (raw wheat stock, flour stock, packaging materials).

Receivables (flour sold on credit).

Payables (delayed payment for wheat and utilities).

Operating Cash Flow = Net Income + Non-cash items – Working Capital Changes.

Cash Flow from Investing

Capital Expenditure (CAPEX): Purchase of mill machinery, silos, buildings, and land improvements.

Expansion costs (new production lines).

Residual/salvage value of equipment (if sold).

Cash Flow from Financing

Equity Injection: Capital raised from owners or investors.

Debt Drawdown: Loan proceeds.

Debt Repayments: Principal repayments.

Interest Payments (sometimes shown in operating depending on accounting).

Dividends Paid to shareholders.

Net Cash Flow = Operating CF + Investing CF + Financing CF

Closing Cash Balance = Opening Cash + Net Cash Flow

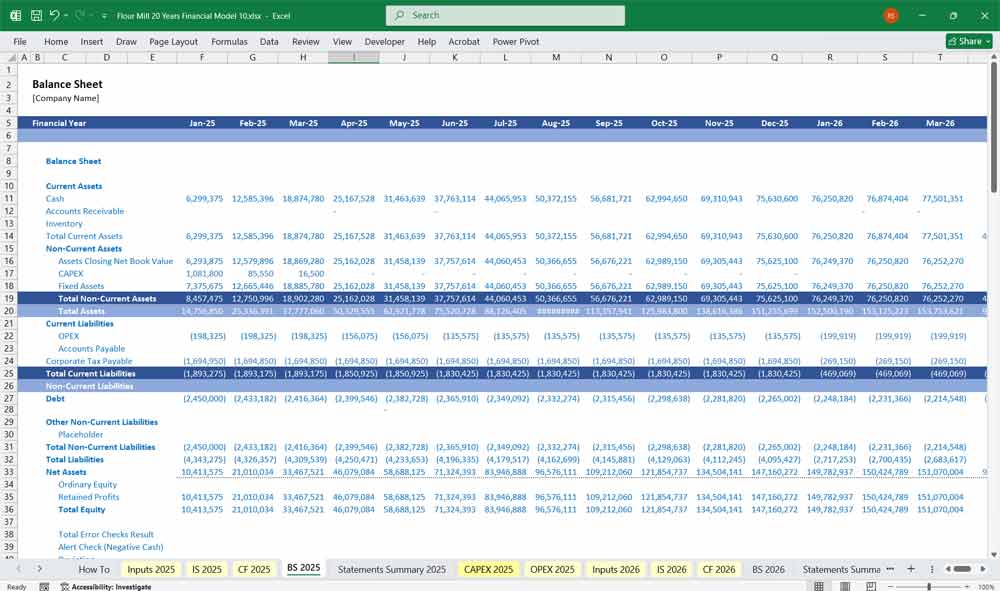

Flour Mill Balance Sheet

A snapshot of the flour mill’s financial position.

Assets

Current Assets

Cash & equivalents.

Accounts receivable (customers).

Inventory (wheat, flour, bran, packing materials).

Prepaid expenses & deposits.

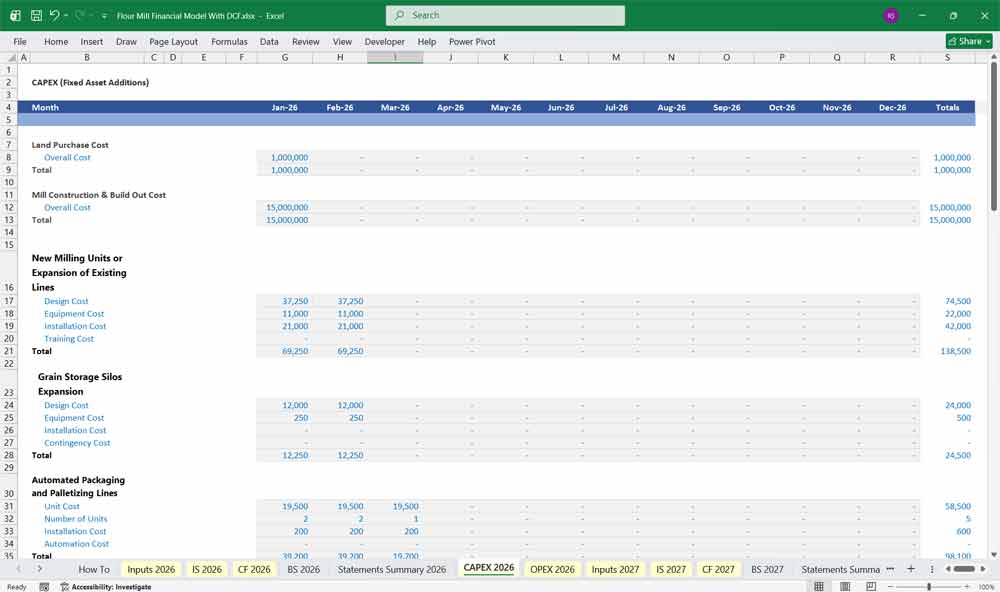

CAPEX (Fixed Asset Additions)

CAPEX Examples

New Milling Units or Expansion of Existing Lines.

Grain Storage Silos Expansion.

Inventory (wheat, flour, bran, packing materials).

Automated Packaging and Palletizing Lines.

- Quality Control Laboratory Equipment

OPEX

OPEX Examples

Personnel Costs.

Maintenance and Repair.

Transportation and Logistics.

Digital and Technology Costs.

Non-Current Assets

Property, Plant & Equipment (mills, silos, vehicles, land).

Intangible assets (licenses, software).

Accumulated depreciation (contra asset).

Total Assets = Current + Non-Current Assets

Liabilities

Current Liabilities

Accounts payable (wheat suppliers, utilities).

Short-term loans/overdrafts.

Accrued expenses (wages, utilities payable).

Non-Current Liabilities

Long-term loans (bank debt for capex).

Lease liabilities (if equipment is leased).

Total Liabilities = Current + Non-Current Liabilities

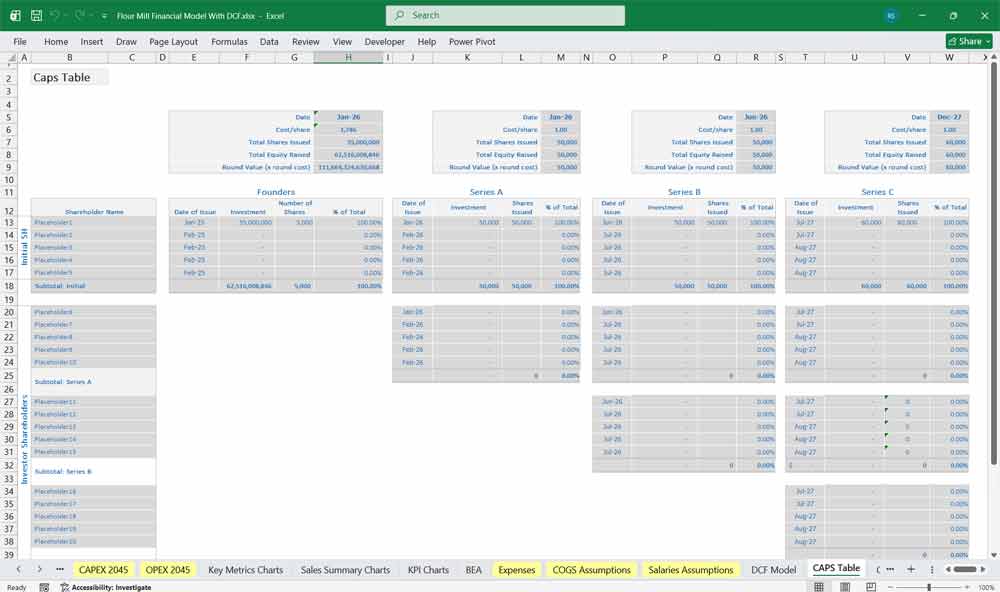

Equity

Paid-in capital (shareholder investment).

Retained earnings (cumulative net profits not distributed).

Reserves.

Total Equity = Share Capital + Retained Earnings

Balance Sheet Equation: Assets = Liabilities + Equity

Key Financial Metrics for a Flour Mill

Key Ratios & to Track

Gross Margin % = Gross Profit / Revenue

EBITDA Margin %

Net Margin %

Debt-to-Equity Ratio

Current Ratio = Current Assets / Current Liabilities

DSCR (Debt Service Coverage Ratio) = Cash Flow from Operations / Debt Service

Capacity Utilization %

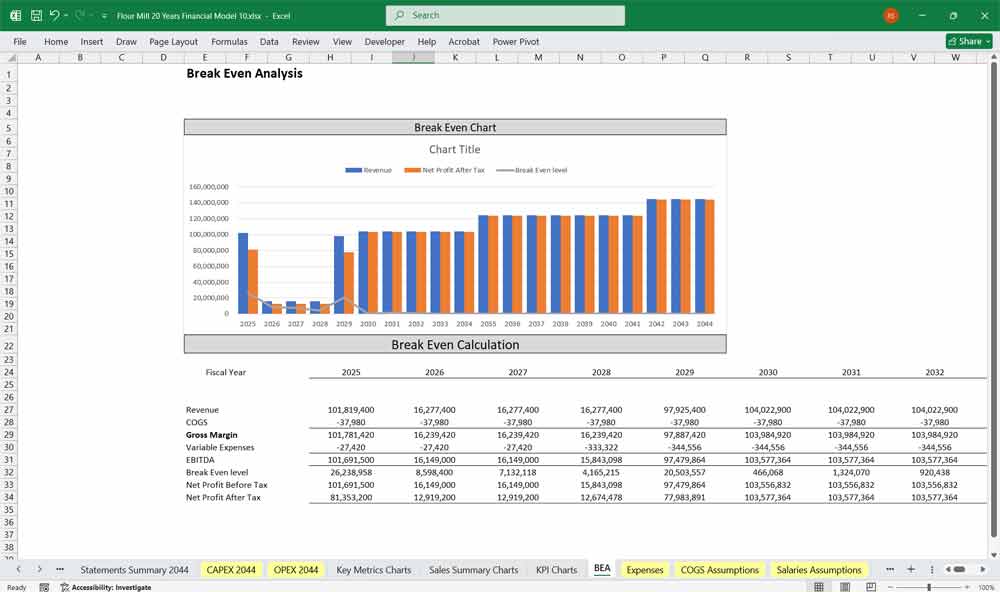

Break-even Point (tons of wheat processed vs. fixed + variable costs)

20-Year Flour Mill Financial Model Benefits

Mill owners and investors a long-term view of business performance, allowing them to see how capacity utilization, raw material costs, and selling prices might evolve over decades. Since flour milling is capital-intensive, with high upfront investment in machinery and infrastructure, having a long horizon helps assess whether the business will generate sustainable profits over its lifecycle.

Flour Mill Strategies

This model provides clarity on debt repayment and financing strategies. Flour mills often require significant bank loans or equity injections to set up. A 20-year projection ensures that repayment schedules, interest costs, and refinancing risks are mapped against expected cash flows, reducing the chance of liquidity crises and ensuring lenders gain confidence in the business.

Long-term Flour Mill Maintenance Planning

It also allows managers to anticipate maintenance and replacement cycles for equipment. Milling machinery and silos typically last 10–20 years before major overhauls are needed. A model spanning two decades can incorporate these capital expenditures, making sure funds are set aside for reinvestment without disrupting operations.

Scenario and Sensitivity Mill Analysis

Additionally, a long-term model enables the mill to test scenario and sensitivity analyses. Wheat prices, energy costs, and demand for flour are highly volatile. By extending projections over 20 years, owners can examine best- and worst-case scenarios, assess the impact of market shifts, and adjust strategies such as diversification into byproducts or value-added products.

Better Flour Mill Growth Planning

Finally, a 20-year horizon supports strategic planning and growth decisions. Whether the mill expands capacity, enters new markets, or pursues vertical integration (e.g., bakeries or packaged food), the model shows the financial impact of these decisions over time. This helps ensure that short-term gains do not compromise long-term sustainability, aligning business growth with shareholder expectations.

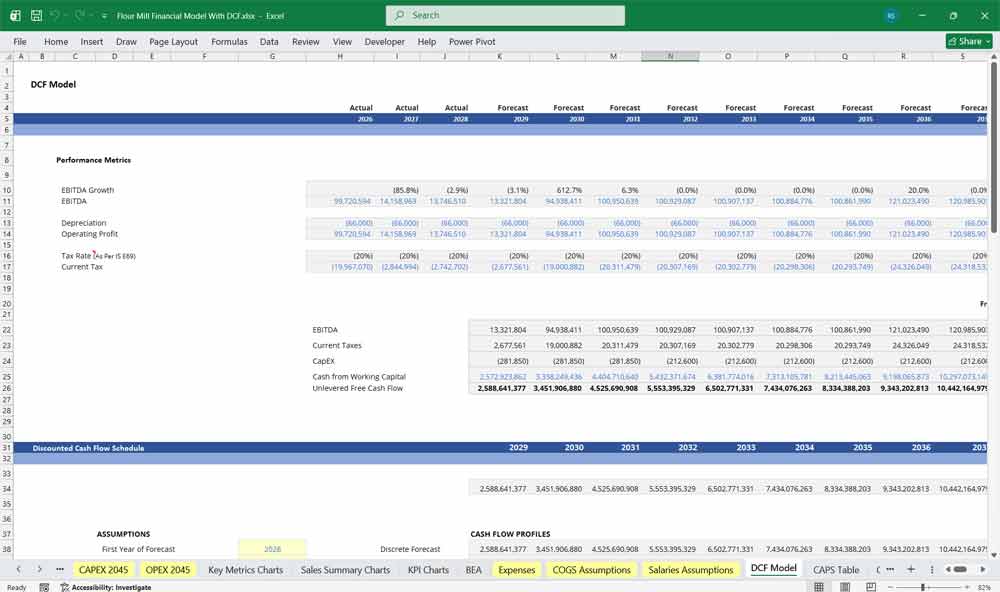

Valuing Your Mill With A DCF

Analysing the Discounted Cash Flow Of Your Flour Mill

A Discounted Cash Flow (DCF) analysis for a flour mill estimates the facility’s value based on projected future cash flows generated from processing wheat into flour and related by-products. Revenue forecasts are driven by milling capacity, utilization rates, flour pricing, by-product sales (such as bran), and regional demand from bakeries and food manufacturers, while costs include wheat procurement, energy, labor, maintenance, and capital expenditures for equipment upgrades. The projected free cash flows over a defined period, along with a terminal value reflecting the mill’s long-term operating life, are discounted to present value to determine the mill’s intrinsic value.

WACC for a Flour Mill

Weighted Average Cost of Capital (WACC) is used as the discount rate in valuing a flour mill and reflects the blended cost of equity and debt financing. The business is influenced by commodity price volatility (particularly wheat), margin pressures, working capital intensity, and competitive dynamics in the food processing industry. The WACC incorporates investors’ required returns, the company’s capital structure, and the tax benefits of debt, representing the minimum return necessary to justify investment in the milling operation.

Sensitivity Analysis for a Flour Mill

Sensitivity analysis is critical in valuing a flour mill due to uncertainties in wheat prices, flour selling prices, demand fluctuations, energy costs, and operating efficiency. Analysts typically test changes in key assumptions such as gross margins, throughput volumes, working capital requirements, capital expenditures, and WACC. By assessing how variations in these inputs affect the DCF valuation, sensitivity analysis identifies the most significant value drivers and provides a range of potential outcomes to support sound financial and operational decision-making.

Final Notes on the Financial Model

This 20 Year Flour Mill Financial Model focuses on balancing capital expenditures with steady revenue growth from diversified services. By optimizing operational costs, and power efficiency, and maximizing high-margin services, the model helps long-term sustainable profitability and cash flow stability.

Download Link On Next Page

Download Link On Next Page