Cement Factory Financial Model

20-year Financial Model for a Cement Factory

This very extensive 20 Year Cement Factory Model involves detailed revenue projections from all your cement factory sales, cost structures, capital expenditures, and financing needs. This model provides a thorough understanding of the financial viability, profitability, and cash flow position of the factory. Including: 20x Income and Cash Flow Statements, Balance Sheets, CAPEX and OPEX spreadheets, Statement Summary Excel Charts, and Revenue Forecasting Charts with the specified revenue streams, 20-year Break Even Analysis charts, employee salary tabs and expenses sheets.

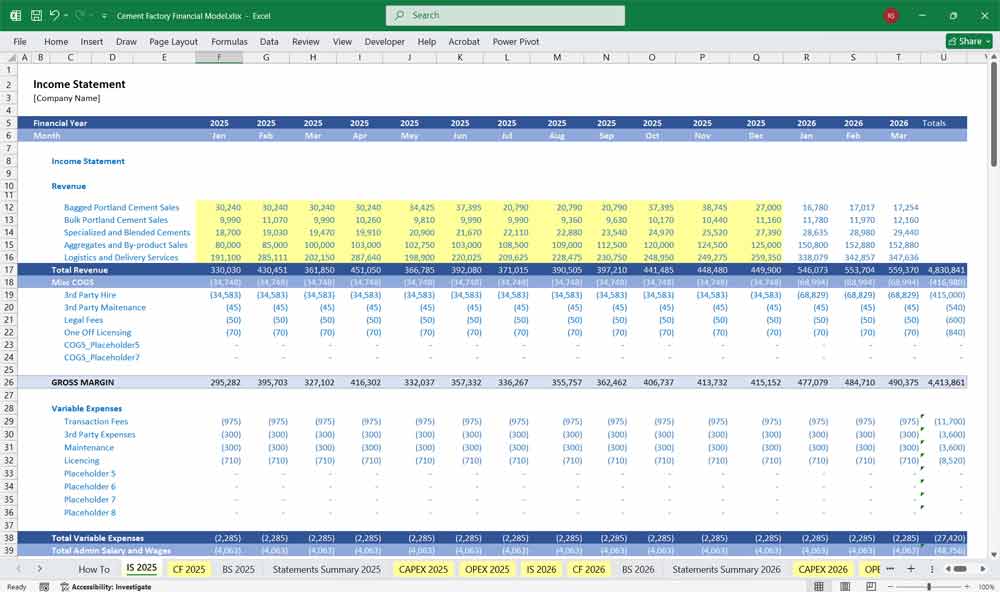

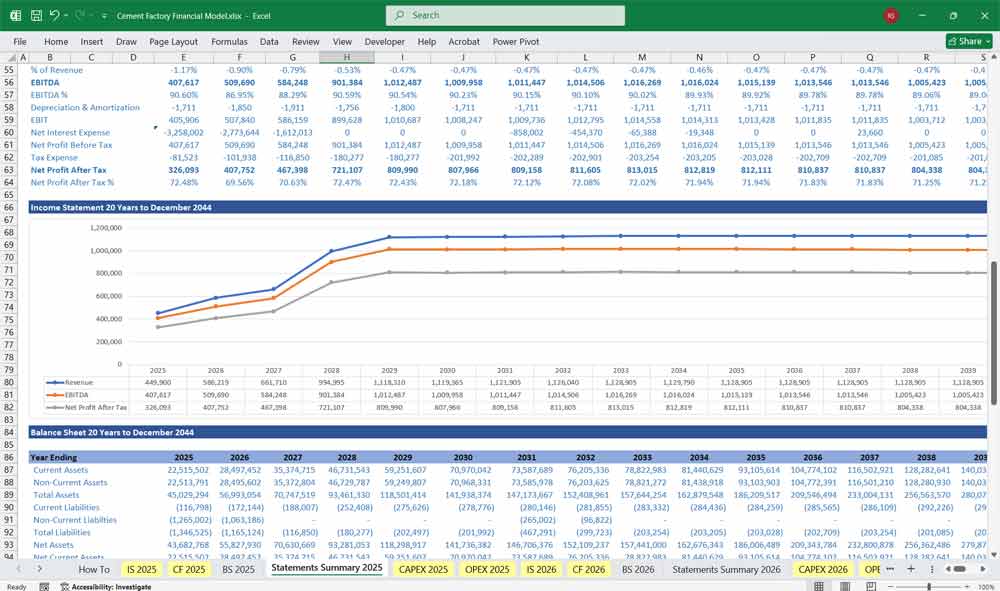

Income Statement (P&L)

Revenue Segments

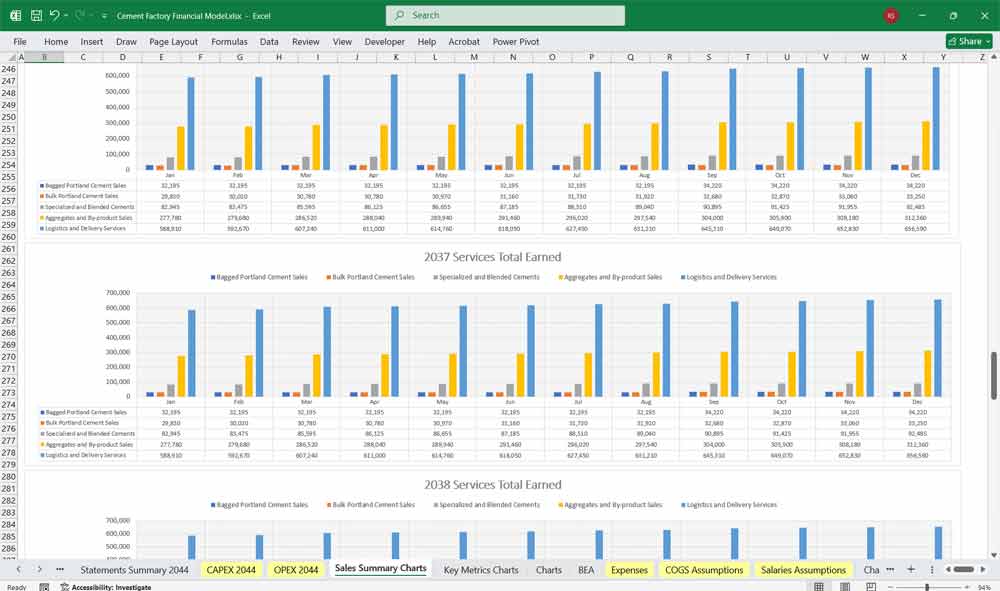

Bagged Cement Sales

Targeted at retail and smaller contractors.

Revenue = Volume sold (tons) × Price per ton

Bulk Portland Cement Sales

Sold in bulk to major infrastructure and commercial projects.

Higher volume, slightly lower margin.

Specialized and Blended Cements

Includes sulfate-resistant, white cement, fly-ash blended products, etc.

Premium pricing; smaller volumes.

Aggregates and By-Product Sales

Crushed stone, sand, gravel, clinker by-products.

Lower margins, high-volume side stream.

Logistics and Delivery Services

Revenue from delivery charges, own fleet utilization, logistics for third parties.

Cost of Goods Sold (COGS)

Raw Materials: Limestone, clay, gypsum, fly ash, additives.

Energy Costs: Electricity, coal, gas—major component.

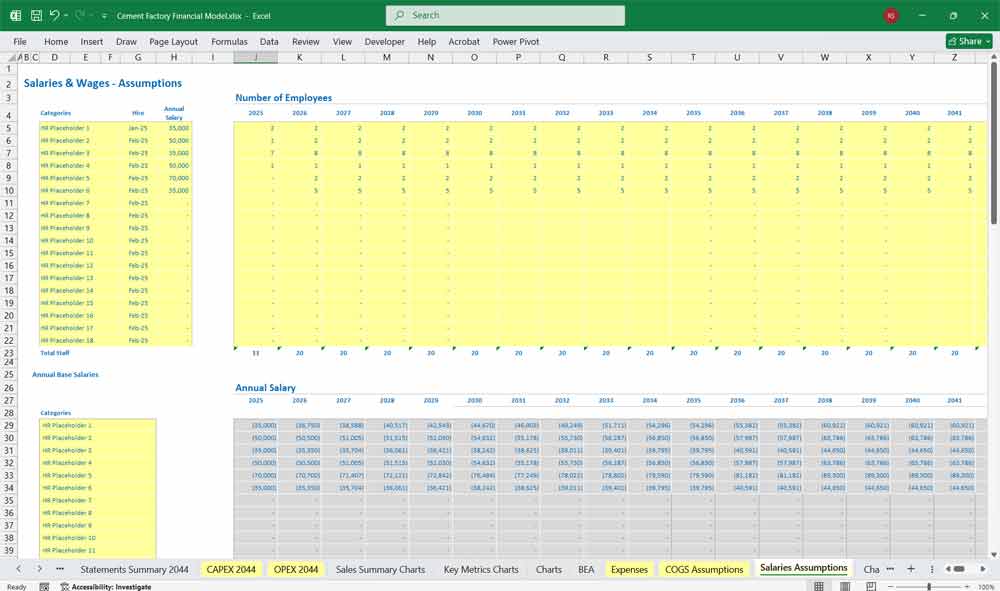

Labor (Production Staff)

Maintenance & Consumables

Packaging Costs (for bagged cement)

Depreciation (of production equipment)

Gross Profit = Revenue – COGS

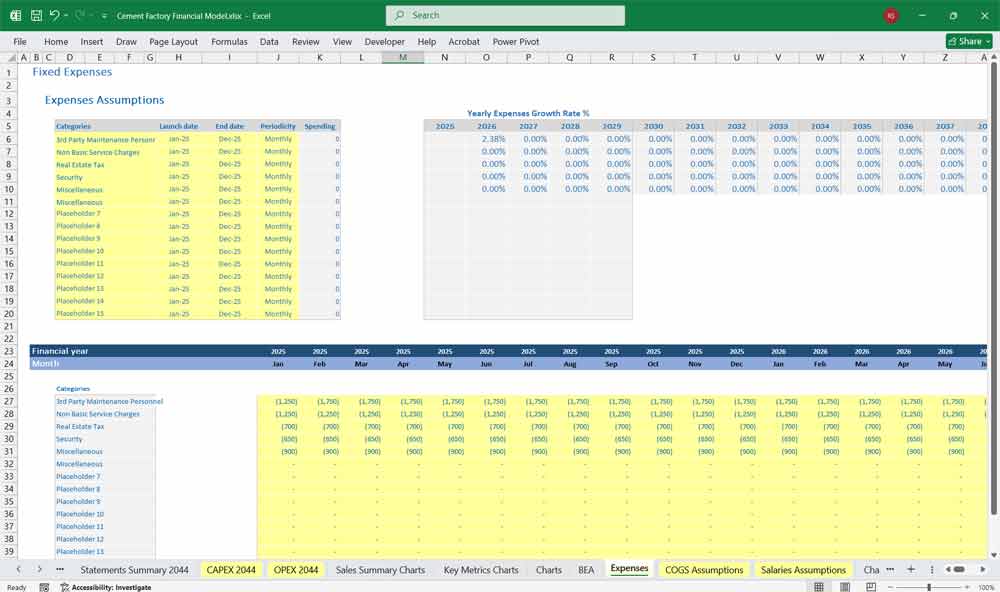

Operating Expenses (OPEX)

Selling & Distribution

Marketing & Branding

Administrative Staff

IT and Communication

Insurance, Legal, Licenses

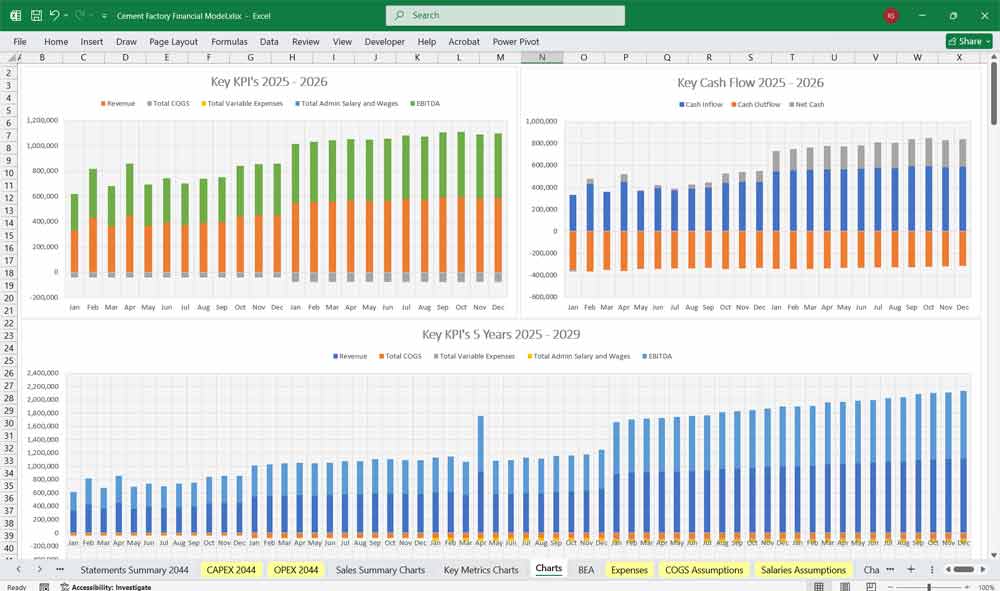

EBITDA = Gross Profit – OPEX

Other Income / Expenses

Interest Income/Expense

Foreign Exchange Gain/Loss

Government Subsidies (if any)

EBIT = EBITDA – Depreciation

Taxes

Corporate Tax Rate (e.g., 30%)

Net Income = EBIT – Interest – Taxes

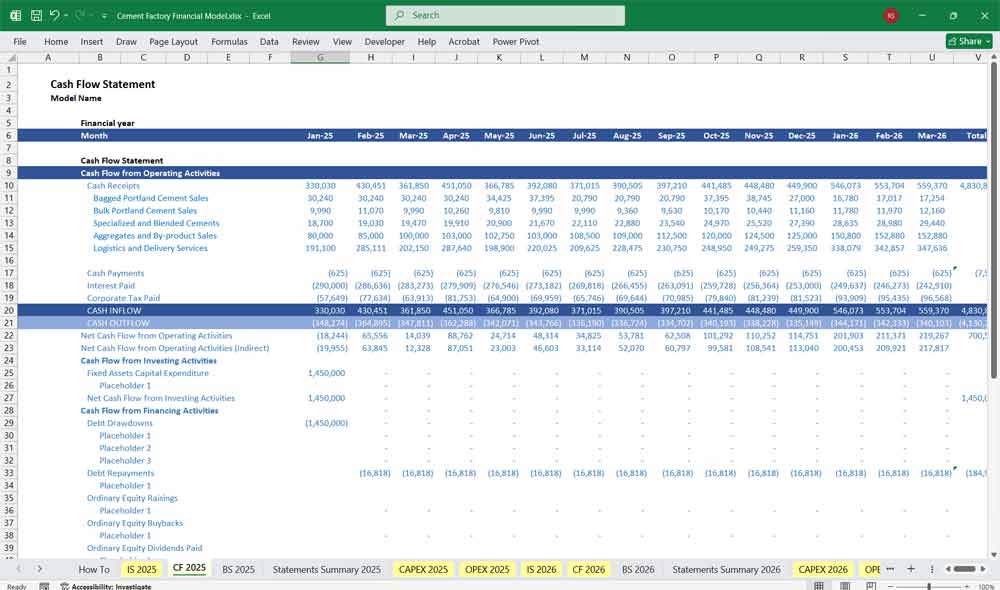

Cement Factory Cash Flow Statement

Operating Activities

Net Income

Add back non-cash items:

Depreciation

Amortization

Changes in Working Capital:

Increase in Receivables (–)

Increase in Payables (+)

Inventory Changes

Net Cash from Operations

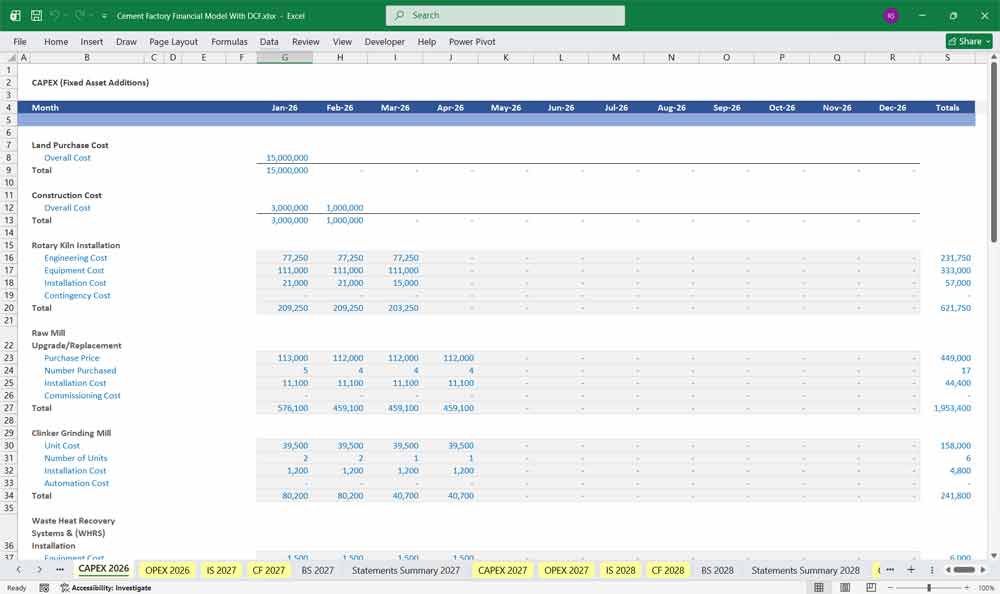

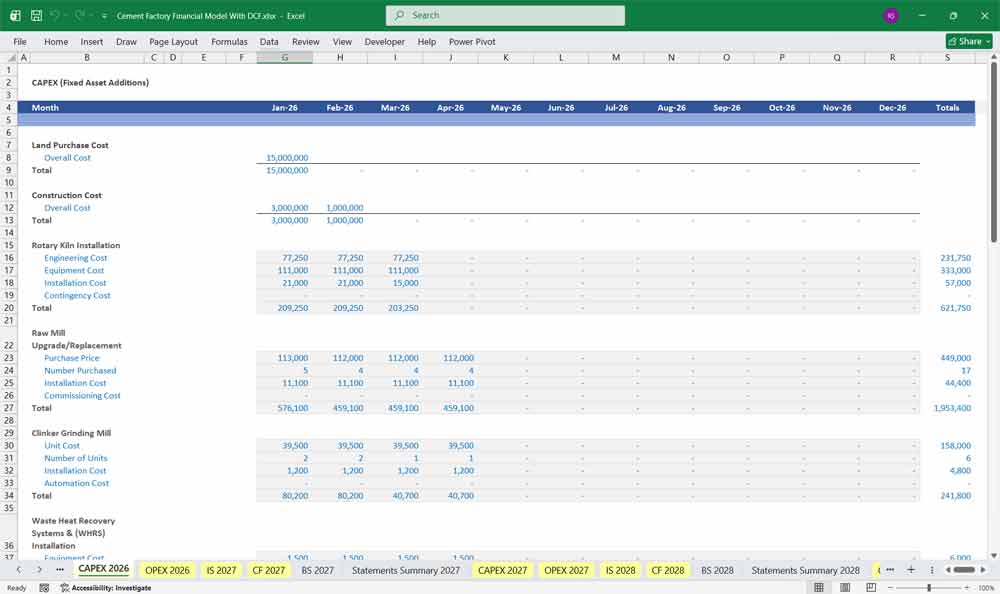

Investing Activities

Capital Expenditures (CapEx):

New kilns, maintenance of equipment, trucks, bagging plants

Investment in R&D or Specialized Products

Sale of Equipment

Net Cash from Investing

Financing Activities

Equity Injections

Debt Raised / Repaid

Interest Paid

Dividends Paid

Net Cash from Financing

Cash Reconciliation

Net Increase/Decrease in Cash = Operating + Investing + Financing

Ending Cash Balance = Beginning Cash + Net Increase/Decrease

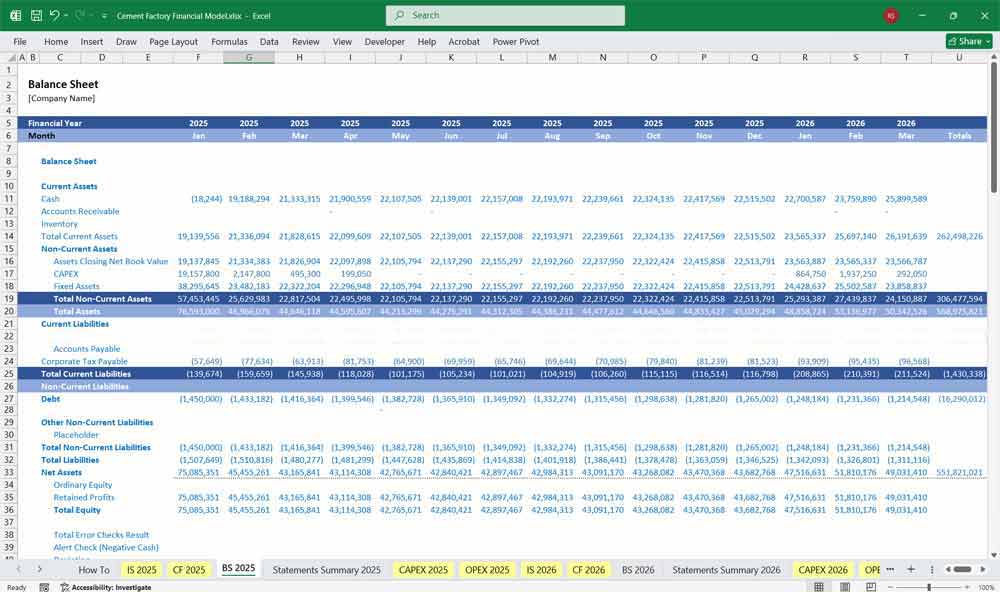

Cement Factory Balance Sheet

Assets

Current Assets

Cash & Equivalents

Accounts Receivable (from cement buyers, distributors)

Inventory:

Raw materials (limestone, gypsum)

Work-in-progress (clinker)

Finished goods (bagged cement)

Prepaid Expenses

Non-Current Assets

Property, Plant & Equipment (kilns, crushers, mills)

Vehicles & Transport Fleet

IT Infrastructure

Intangible Assets (software licenses, patents)

Accumulated Depreciation

Liabilities

Current Liabilities

Accounts Payable

Accrued Expenses

Short-Term Loans / Lines of Credit

Current Portion of Long-Term Debt

Non-Current Liabilities

Long-Term Loans/Bonds

Deferred Tax Liabilities

Lease Liabilities

Equity

Share Capital

Share Premium

Retained Earnings

Reserves (e.g., revaluation, currency translation)

Assets = Liabilities + Equity

Interlinking Financials

Net Income flows into Retained Earnings (Balance Sheet).

Depreciation is added back in Cash Flow, deducted in Income Statement.

CapEx reduces cash in Cash Flow, adds to PPE in Balance Sheet.

Debt service hits both Cash Flow (Financing) and Balance Sheet (Liabilities).

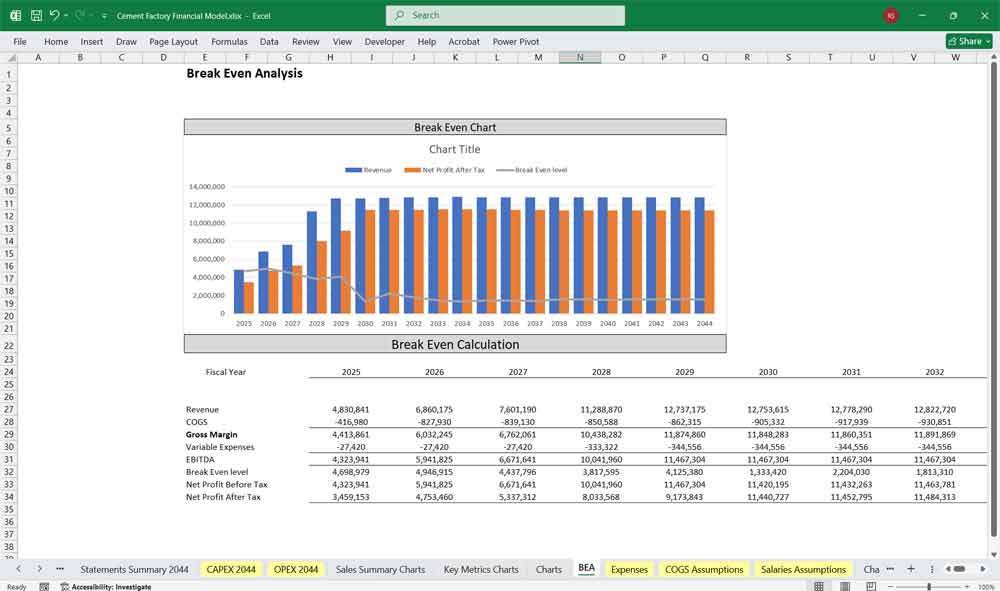

Key Financial Metrics for a Cement Factory

Revenue Metrics

Cement Factory Sales of Bagged Portland Cement

Bagged Portland Cement is primarily sold to the retail market, small contractors, and individual builders. It is packaged in 25–50 kg bags and distributed through hardware stores, regional dealers, and direct retail outlets. This segment is characterized by higher margins due to value-added packaging and wide accessibility. Cement Factory generates approximately 35% of its total revenue from bagged cement sales, making it a key driver of brand visibility and retail penetration.

Cement Factory Sales of

Bulk Portland Cement

Bulk Portland Cement is sold in large volumes to infrastructure projects, commercial real estate developers, and ready-mix concrete plants. Delivered in bulk via silos or tankers, this product supports large-scale construction activity and offers cost efficiency to major clients. Although priced lower per ton compared to bagged cement, its scale compensates with volume. This segment accounts for around 30% of Cement Factory’s sales, serving as a steady base for recurring B2B contracts.

Specialized and Blended Cement Revenue from

Cement Factory Sales

This category includes high-performance and custom formulations such as sulfate-resistant cement, white cement, and fly-ash or slag-blended cements. These are used in projects requiring durability, specific chemical resistance, or aesthetic finishes. Though volumes are relatively low, pricing is premium. Specialized and blended cement contributes roughly 10% to Cement Factory’s revenue, appealing to niche markets and government infrastructure mandates for green building materials.

Aggregates and By-product Cement Factory Sales

Cement Factory processes and sells aggregates like crushed stone, gravel, and sand, as well as by-products such as clinker and kiln dust. These are either used internally in concrete mixes or sold to external contractors and manufacturers. This segment allows the company to monetize production waste and quarry overburden. Aggregates and by-product sales represent about 15% of the company’s total income, adding value to otherwise underutilized resources.

Logistics and Delivery Services From Your

Cement Factory

To enhance customer service and capture downstream value, Cement Factory operates an in-house logistics network that includes truck fleets and bulk carriers. Delivery services are charged separately or bundled depending on the contract. The company also offers third-party logistics to smaller manufacturers. Logistics and delivery services generate approximately 10% of total sales, while also enabling better distribution control and customer retention.

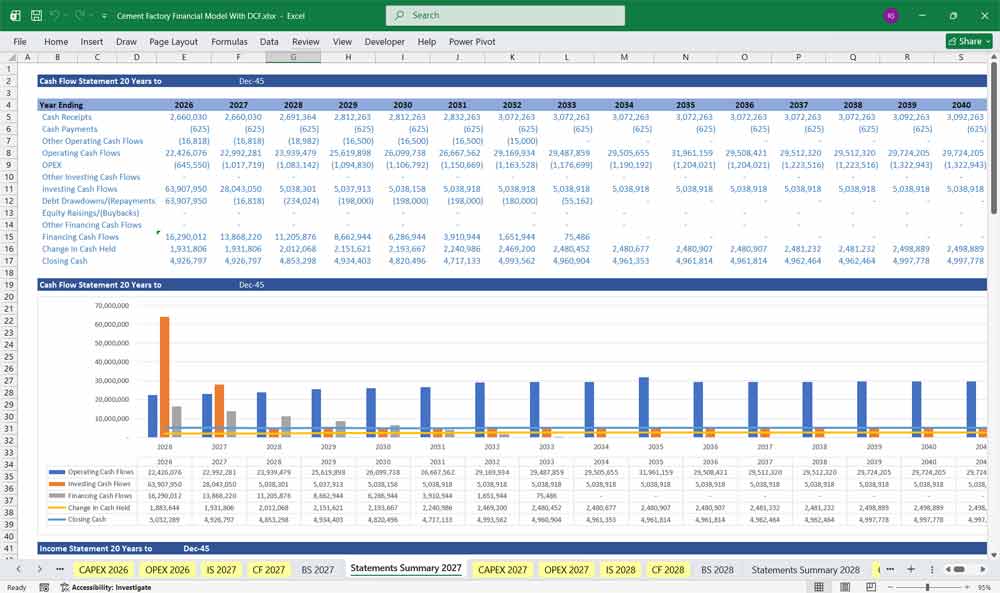

Cement Factory Discounted Cash Flow (DCF) with Terminal Value, Sensitivity Analysis, and WACC Model Add-On

DCF for a Cement Factory

A Discounted Cash Flow (DCF) analysis for a cement factory estimates the plant’s value based on projected future cash flows generated from cement production and sales. Revenue is driven by production capacity, capacity utilization rates, cement pricing, and regional construction demand, while costs include raw materials (such as limestone and clinker), energy, labor, and maintenance capital expenditures. The forecasted free cash flows over a defined period, along with a terminal value reflecting the plant’s long-term operating life, are discounted to present value to determine the factory’s intrinsic value.

WACC for a Cement Factory

Weighted Average Cost of Capital (WACC) is used as the discount rate in valuing a cement factory because it reflects the blended cost of debt and equity financing. Cement manufacturing is capital-intensive and exposed to cyclical construction activity, energy price volatility, and environmental regulations, all of which influence its risk profile and cost of capital. The WACC captures investors’ required returns, the company’s capital structure, and the tax shield benefits of debt, representing the minimum return required to justify continued investment in the facility.

Sensitivity Analysis for a Cement Factory

Sensitivity analysis is essential in cement factory valuation due to uncertainties in demand cycles, pricing pressures, fuel and power costs, and capital expenditure requirements. Analysts typically test changes in key assumptions such as sales volumes, average selling prices, operating margins, energy costs, and WACC. By evaluating how variations in these inputs affect the DCF valuation, sensitivity analysis highlights the most critical value drivers and provides a range of potential outcomes to support strategic and investment decisions.

Final Notes on the Financial Model

This 20 Year Cement Factory Financial Model focuses on balancing capital expenditures with steady revenue growth. By optimizing operational costs, and power efficiency, and maximizing high-margin services like Portland Bulk Sales, the model ensures sustainable profitability and cash flow stability.

Download Link On Next Page

Download Link On Next Page