Calcium Carbide Plant Financial Model

20-Year Financial Model for a Calcium Carbide Plant

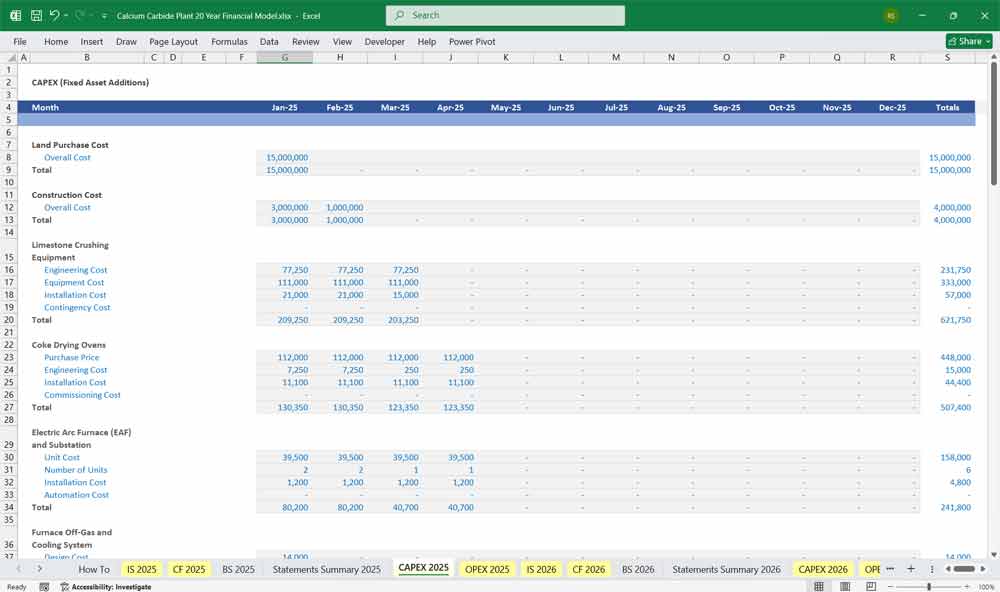

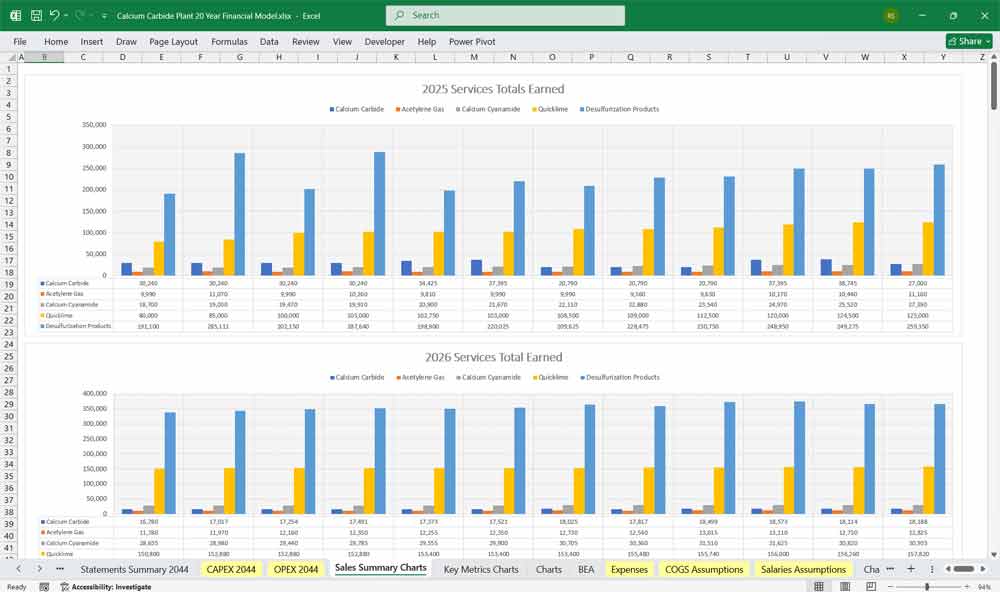

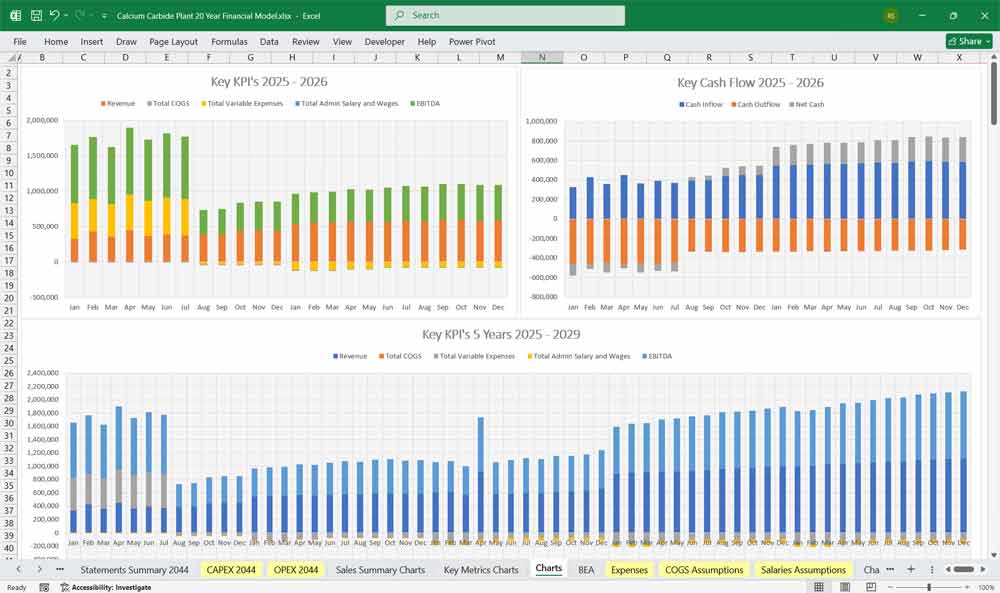

This very extensive 20 Year Calcium Carbide Model involves detailed revenue projections, cost structures, capital expenditures, and financing needs. This model provides a thorough understanding of the financial viability, profitability, and cash flow position of your plant. Includes: 20x Income Statements, Cash Flow Statements, Balance Sheets, CAPEX sheets, OPEX Sheets, Statement Summary Sheets, and Revenue Forecasting Charts with the revenue streams, BEA charts, sales summary charts, employee salary tabs and expenses sheets. Over 130 Spreadsheets in 1 Excel Workbook.

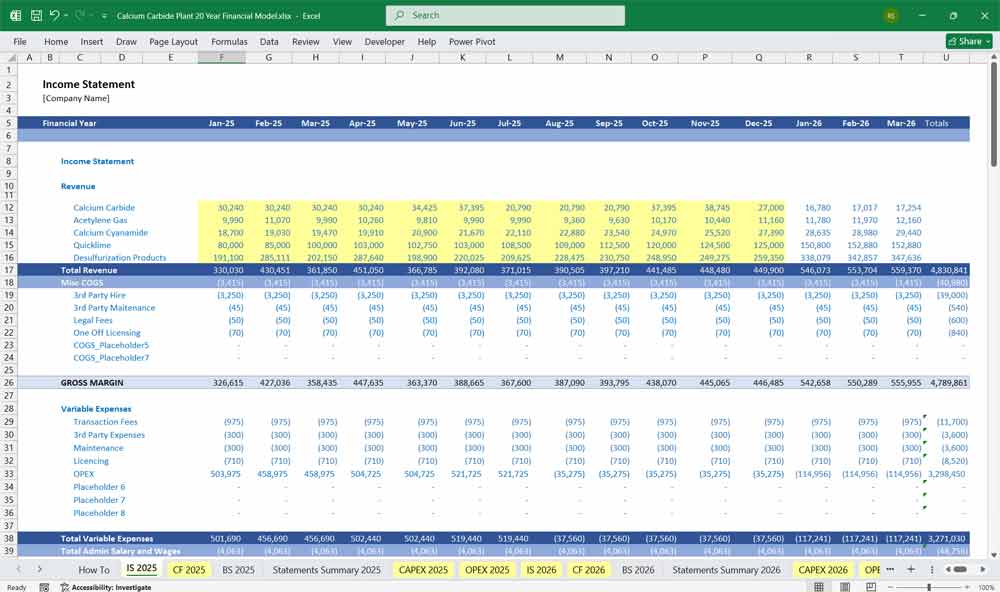

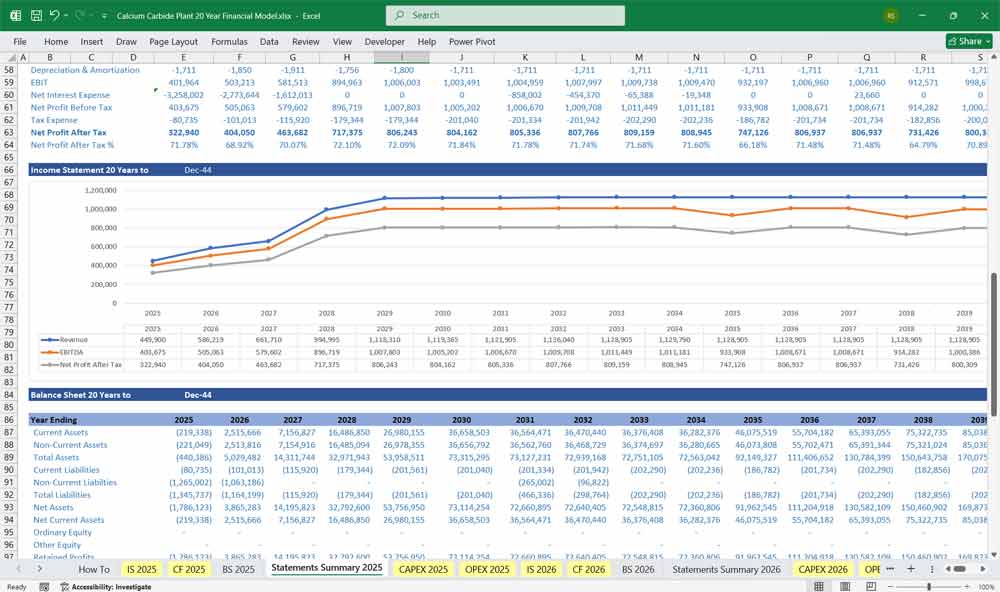

Income Statement (P&L)

Structure:

A. Revenue

Sum of revenues from:

Calcium Carbide Sales = Qty × Price

Acetylene Gas Sales = Qty × Price

Calcium Cyanamide Sales = Qty × Price

Quicklime Sales = Qty × Price

Desulfurization Products = Qty × Price

B. Cost of Goods Sold (COGS)

Includes:

Raw materials (coke, limestone, quicklime)

Power and fuel

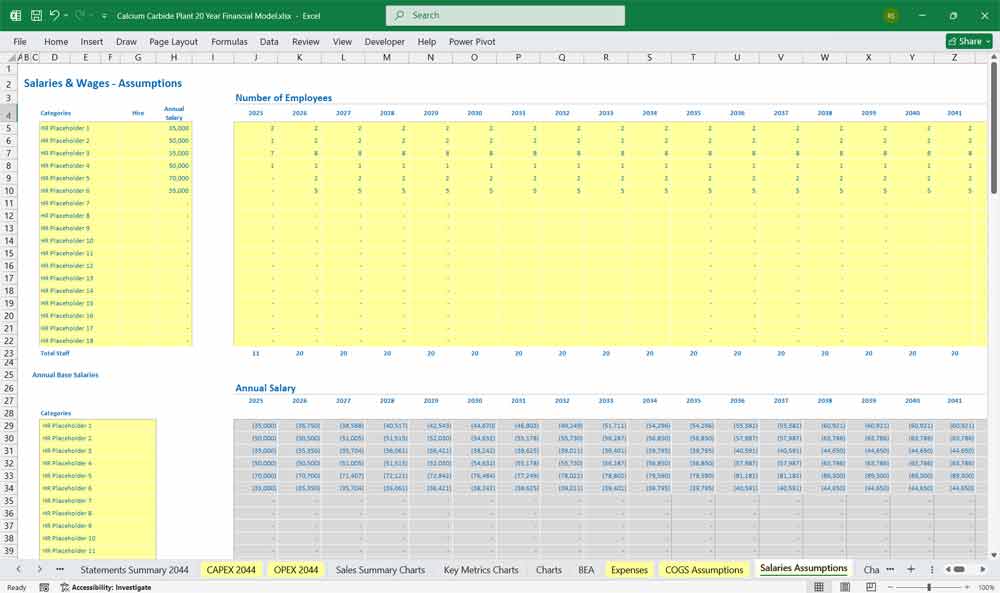

Direct labor

Maintenance and spare parts

Factory overheads

C. Gross Profit = Revenue – COGS

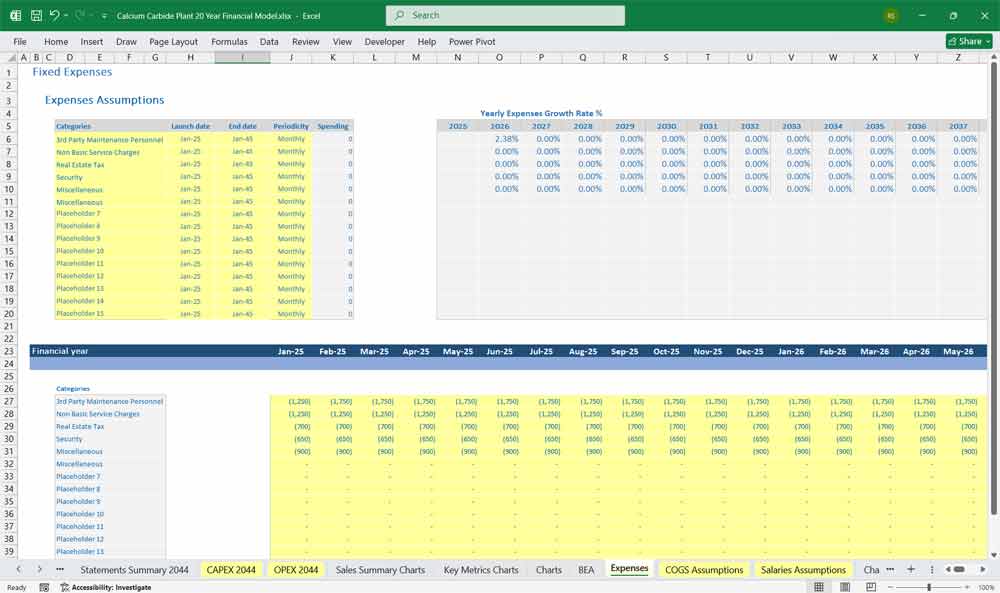

D. Operating Expenses

Selling & distribution

Administrative & general

R&D and technical supervision

Insurance and regulatory

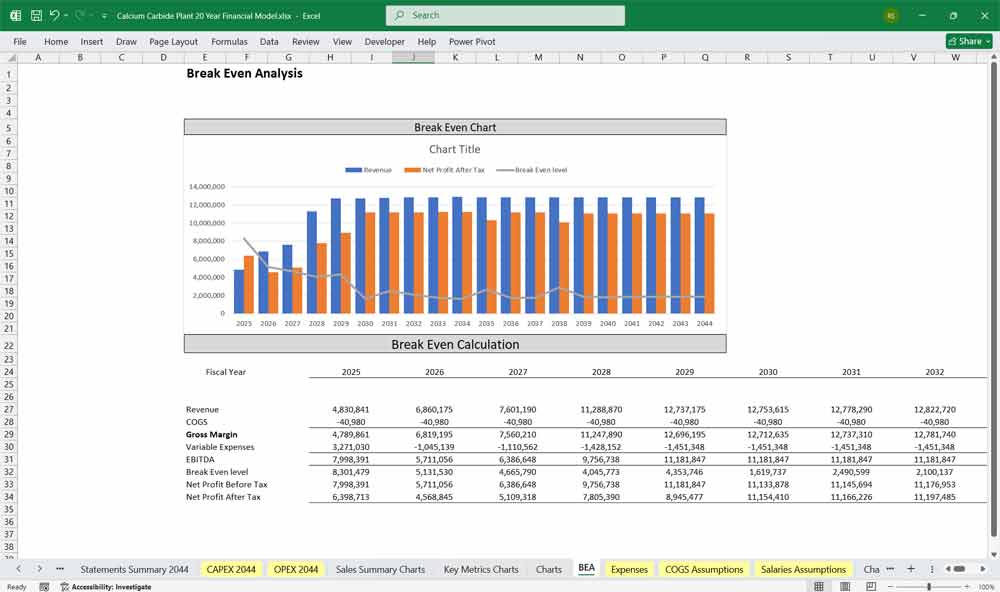

E. EBITDA = Gross Profit – Operating Expenses

F. Depreciation

Based on plant & equipment (typically 10–15% declining balance or 20-year straight-line)

G. EBIT = EBITDA – Depreciation

H. Interest Expense

Derived from loan financing schedule

I. EBT (Earnings Before Tax) = EBIT – Interest

J. Taxes = EBT × Tax Rate

K. Net Income = EBT – Taxes

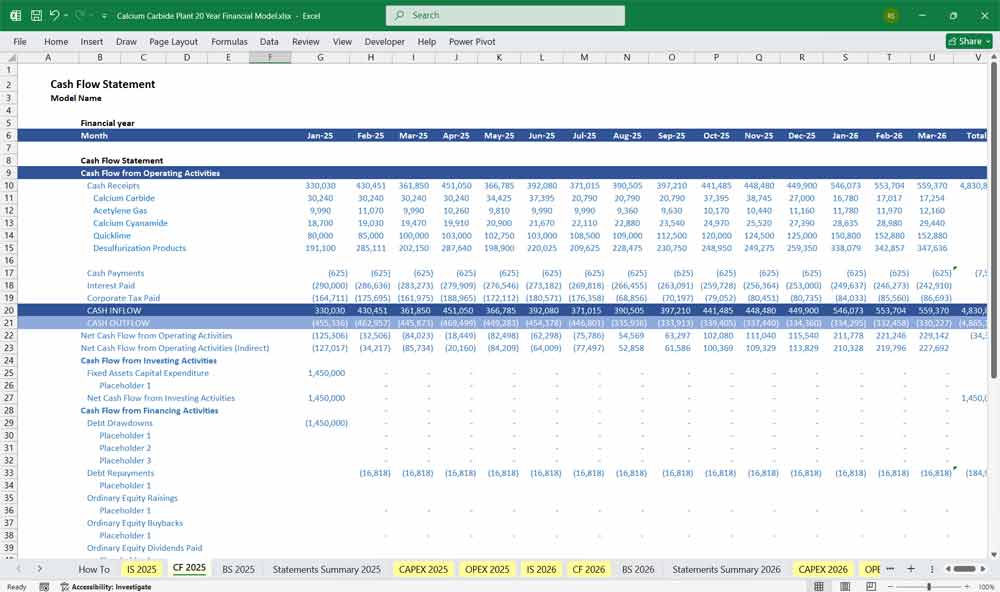

Calcium Carbide Plant Cash Flow Statement (CFS)

The Cash Flow Statement tracks all cash inflows and outflows, crucial for assessing liquidity and debt service capacity.2 It reconciles Net Income (accrual basis) to actual cash movement (cash basis).

A. Cash Flow from Operating Activities (CFO)

This section starts with Net Income and adjusts for non-cash items and changes in working capital.

Net Income: (From Income Statement)

+ Depreciation & Amortization (D&A): Add-back since it’s a non-cash expense.

Changes in Working Capital: Reflects changes in short-term assets and liabilities.

– $\Delta$ Inventory: An increase in inventory is a cash outflow.

– $\Delta$ Accounts Receivable (A/R): An increase in A/R means sales cash hasn’t been collected yet (cash outflow).

+ $\Delta$ Accounts Payable (A/P): An increase in A/P means costs were incurred but not yet paid (cash inflow).6

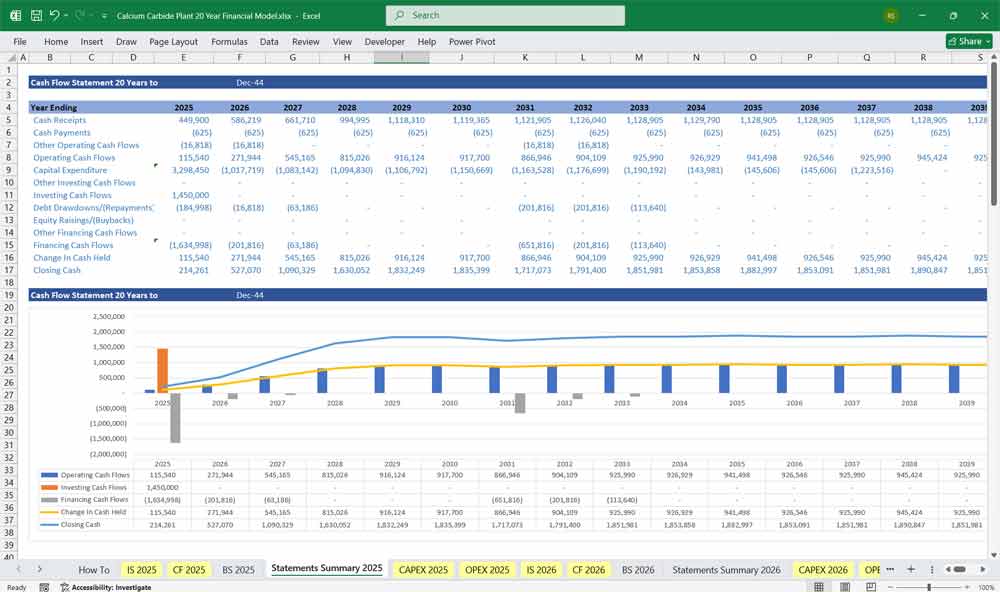

= Net Cash from Operating Activities (CFO)

B. Cash Flow from Investing Activities (CFI)

This section tracks cash used for and generated from investments in long-term assets.

– Capital Expenditures (CapEx): Cash spent on acquiring or upgrading the plant and equipment (cash outflow).

+ Asset Sales: Cash received from selling old assets (cash inflow).

= Net Cash from Investing Activities (CFI)

C. Cash Flow from Financing Activities (CFF)

This section tracks cash interactions with lenders and owners.

+ Debt Issued (New Loans): Cash received from new borrowing (cash inflow).

– Debt Repayment (Principal): Cash used to pay down the principal of loans (cash outflow).

– Dividends Paid: Cash distributed to shareholders (cash outflow).

= Net Cash from Financing Activities (CFF)

D. Net Change in Cash

Net Change in Cash: CFO + CFI + CFF

Ending Cash Balance: Beginning Cash Balance + Net Change in Cash

Calcium Carbide Plant Balance Sheet

Shows assets, liabilities, and equity over time.

A. Assets

Current Assets:

Cash & cash equivalents

Accounts receivable

Inventory (raw materials, finished goods)

Prepaid expenses

Non-Current Assets:

Property, Plant & Equipment (net of depreciation)

Land & buildings

Intangible assets (permits, software, patents)

B. Liabilities

Current Liabilities:

Accounts payable

Accrued expenses

Short-term debt

Long-Term Liabilities:

Term loans

Deferred tax liabilities

C. Shareholders’ Equity

Paid-in capital

Retained earnings (accumulated profit)

Reserves

Key Calcium Carbide Production Industry-Specific Considerations

High Fixed Cost Base: Equipment-heavy industry with high depreciation.

Production Intensity: Critical for staying competitive.

Quality & Certification: Failure costs can be catastrophic (scrap, rework).

Cyclicality & Diversification: Acetylene Gas/Steel and Metallurgy, Agricultural Applications Industry affect volumes.

20-Year Calcium Carbide Plant Financial Model Advantages

A 20-year financial model for a Calcium Carbide plant offers a significantly enhanced perspective on long-term project viability compared to the standard 5- or 10-year models. The primary benefit lies in accurately capturing the full economic life cycle of the plant’s core assets, which often have depreciation periods extending 15 to 20 years. This duration ensures that the model includes the entire scheduled debt repayment, the stabilization of maintenance CapEx after the initial warranty period, and the eventual need for major furnace overhauls or plant revitalization. By extending the horizon, stakeholders gain a clearer picture of the plant’s true steady-state profitability after initial ramp-up and capital allowances expire, providing a more robust foundation for valuation and capital budgeting decisions.

Calcium Carbide Plant Capital Structure Planning

Calcium Carbide production is an energy-intensive process, making it highly susceptible to fluctuations in electricity and raw material (coke/lime) prices. A longer model allows for the detailed simulation of long-term price contracts and hedging strategies, which are necessary to manage this commodity risk. Lenders and equity investors require this extensive view to assess the project’s capacity to service debt even during economic downturns or prolonged periods of low commodity prices. This deep dive into long-term solvency provides the confidence necessary to secure large-scale, non-recourse project financing, which is typical for industrial assets of this scale.

Valuation, investor analysis, Discounted Cash Flow (DCF) For Your Calcium Carbide Production

While the terminal value (representing cash flows beyond the explicit forecast period) is often a large component of valuation, a 20-year model pushes the terminal year further out, reducing the relative uncertainty and risk associated with this single, large assumption. The model generates a significantly longer stream of explicit Free Cash Flows, which are based on specific operational assumptions rather than generalized growth rates. This structural improvement in the DCF calculation yields a more reliable Net Present Value (NPV) and Internal Rate of Return (IRR), essential metrics for making major investment decisions.

Calcium Carbide Plant Tax Planning & Strategic Investment

Many industrial projects benefit from various government incentives, such as accelerated depreciation or tax holidays, which may span 5 to 10 years. A shorter model would fail to capture the significant increase in tax liability once these benefits expire. Conversely, the longer model allows management to strategically plan for major CapEx events—like furnace relining or equipment upgrades—that may occur every 10 to 15 years. This planned reinvestment ensures the plant remains competitive and efficient, allowing the model to project true economic replacement costs rather than relying on generic maintenance figures.

Calcium Carbide Long-Term Market Strategy

Calcium Carbide is an upstream chemical used in the production of PVC, acetylene, and various other industrial products, meaning its demand is tied to global infrastructure and manufacturing growth. A 20-year model allows the plant to simulate market shifts, the impact of carbon pricing or regulatory changes (given the energy intensity), and the potential for product diversification (e.g., shifting toward cleaner processes). This strategic foresight enables the plant’s owners to position the asset for long-term resilience, making the 20-year financial model an essential tool for long-range strategic planning and stakeholder communication regarding the asset’s enduring value.

Final Notes on the Financial Model

This 20 Year Calcium Carbide Plant Financial Model focuses on balancing capital expenditures with steady revenue growth from your plant production sales. By optimizing operational costs, power efficiency, and maximizing high-margin services, the models ensure sustainable profitability and cash flow stability.

Download Link On Next Page, view the full model description