Biofuel Production Plant Financial Model

This 20-Year, 3-Statement Excel Biofuel Production Plant Financial Model includes revenue streams from Bioethanol, Biodiesel, to Sustainable Aviation Fuel, Biolubricants, and Bioplastics, 10 in total. Cost structures and financial statements to forecast the financial health of your composite Biofuel production.

20-Year Financial Model for a Biofuel Production Plant

This very extensive 20 Year Biofuel Production Plant Model involves detailed revenue projections, cost structures, capital expenditures, and financing needs. This model provides a thorough understanding of the financial viability, profitability, and cash flow position of your manufacturing company. Includes: 20x Income Statements, Cash Flow Statements, Balance Sheets, CAPEX sheets, OPEX Sheets, Statement Summary Sheets, and Revenue Forecasting Charts with the revenue streams, BEA charts, sales summary charts, employee salary tabs and expenses sheets. Over 130 Spreadsheets in 1 Excel Workbook.

Overview of the Financial Model

Projection designed to assess the project’s viability, attract financing, and guide strategic decisions. The model is built on several key foundational assumptions:

Production Capacity & Ramp-Up: Defines the maximum annual production volume for each product and the timeline to reach full capacity (e.g., 50% in Year 1, 75% in Year 2, 100% in Year 3).

Feedstock Costs: The price and logistics of procuring primary inputs (e.g., soybean oil, used cooking oil, corn stover, algae).

Conversion Yields: The efficiency of converting a unit of feedstock into a unit of final product (e.g., 1 ton of feedstock yields 0.85 tons of Renewable Diesel).

Sales Prices: The projected selling price for each product, often linked to market indices (e.g., California Low Carbon Fuel Standard credits, RINs prices, fossil fuel benchmarks).

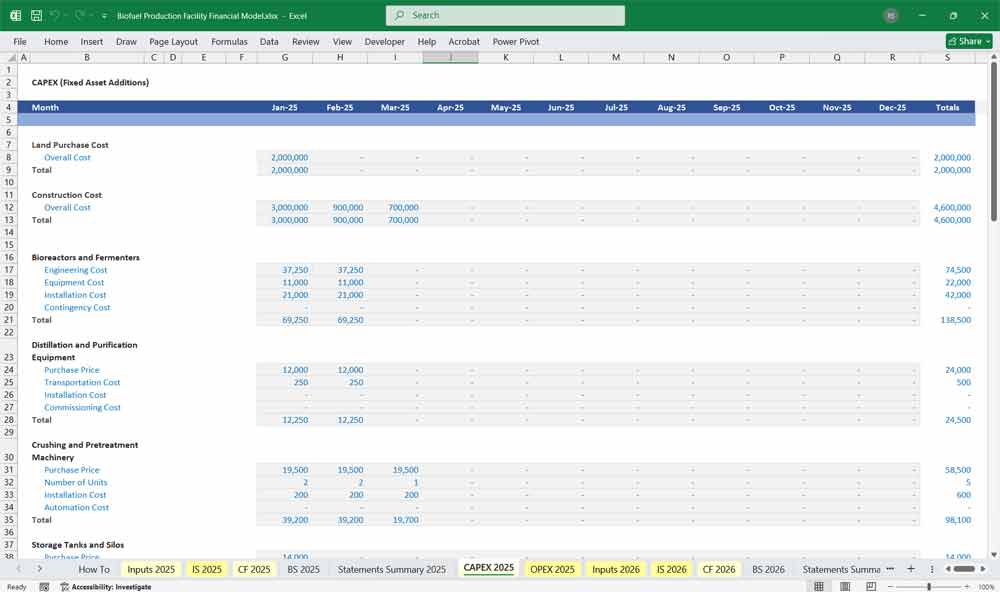

Capital Expenditure (CapEx): The total initial investment in land, plant construction, equipment, and technology.

Operating Expenditure (OpEx): The ongoing costs of running the plant.

Financing Structure: The mix of debt and equity, including interest rates, loan term, and grace period.

Incentives & Tax Credits: Critical revenue components like the Inflation Reduction Act credits, Blenders Tax Credit, and local green incentives.

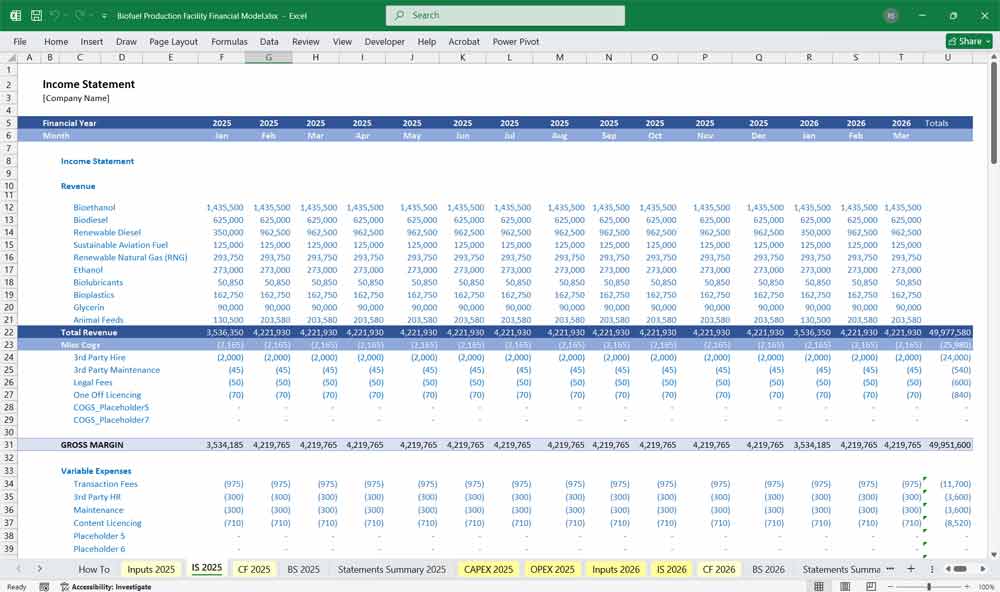

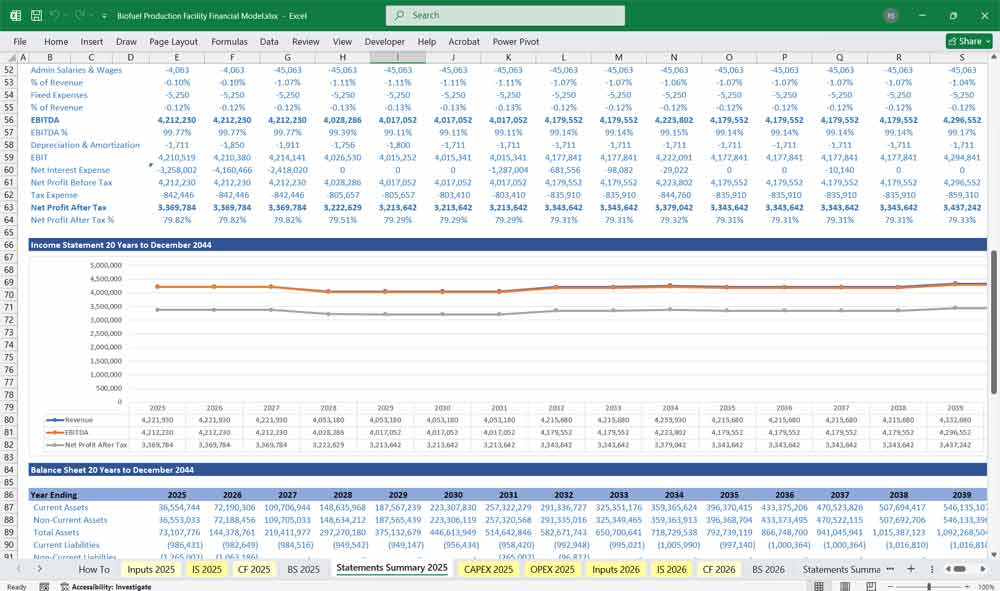

Income Statement (Profit & Loss Statement)

This statement shows the plant’s profitability over a specific period, typically annually.

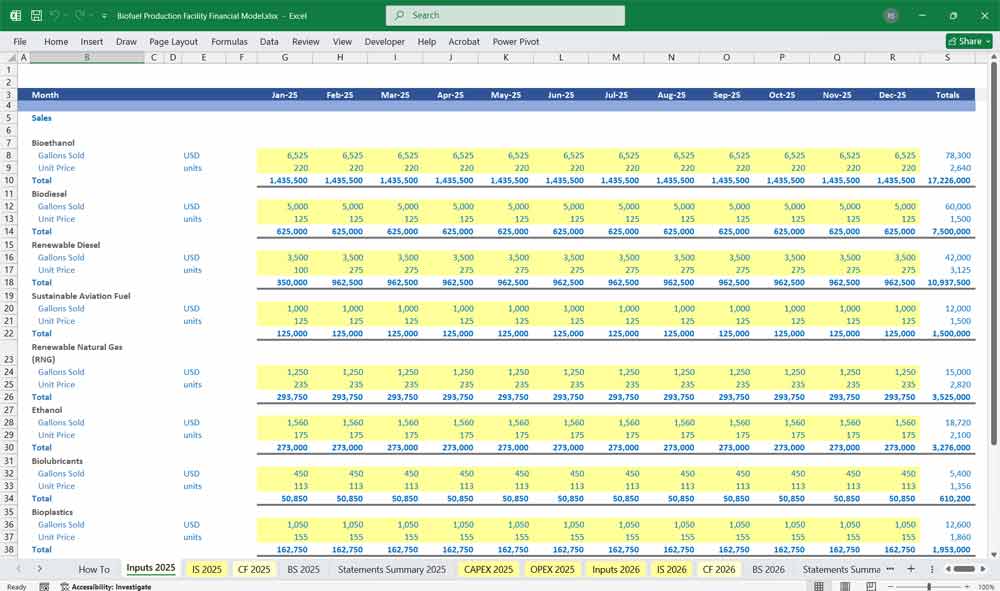

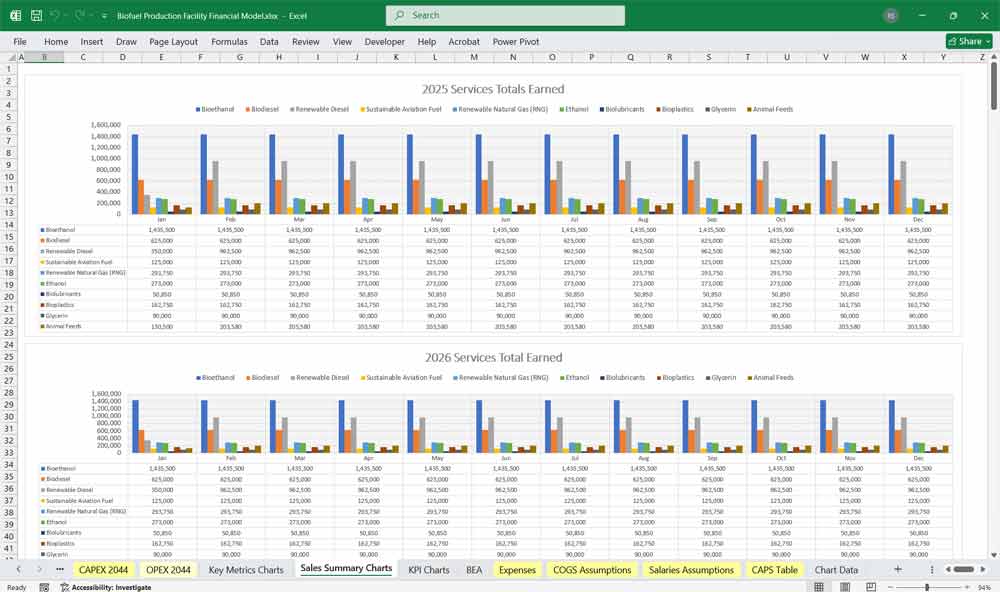

A. Revenue Streams

Revenues are calculated as: Production Volume (less planned downtime) x Off-take Agreement Percentage x Projected Selling Price.

Core Fuel Products:

Renewable Diesel (RD): High-value drop-in fuel. Revenue is a function of the diesel market price plus Renewable Identification Number (RIN) values (D4) and, crucially, California’s Low Carbon Fuel Standard (LCFS) credit value, which is tied to the fuel’s carbon intensity score.

Sustainable Aviation Fuel (SAF): Premium-priced product. Revenue includes the jet fuel price plus a significant green premium from airlines seeking to meet emissions targets, plus applicable RINs (D5/D7) and CORSIA/LCFS credits.

Biodiesel (FAME): Revenue based on its price as a blendstock for diesel, plus RIN values (D4).

Bioethanol: Revenue from its use as a gasoline additive, driven by the gasoline price and RIN values (D6).

Co-Products & High-Value Chemicals (Crucial for Economics):

Renewable Natural Gas (RNG): If produced from biogas (e.g., from anaerobic digestion of waste). Revenue is very high, driven by the natural gas price plus RINs (D3) and LCFS/RFS credits, often making it the most lucrative product on a per-unit basis.

Glycerin: A direct byproduct of biodiesel production. Sold in crude or refined form to the pharmaceutical, food, and chemical industries. Revenue is a function of its purity and market demand.

Biolubricants & Bioplastics: Higher-margin, specialty chemicals. Revenue is based on long-term contracts with industrial or consumer goods companies, often at a significant premium to petroleum-based alternatives.

Animal Feeds: Such as Dried Distillers Grains with Solubles from ethanol production or high-protein meal from oilseed processing. This provides a stable, lower-margin revenue stream that helps offset feedstock costs.

B. Cost of Goods Sold (COGS)

Feedstock Cost: The single largest operating expense. Calculated as Feedstock Consumption Volume x Purchase Price.

Catalysts & Chemicals: Costs for enzymes, methanol, hydrogen, and other chemicals required for the conversion processes.

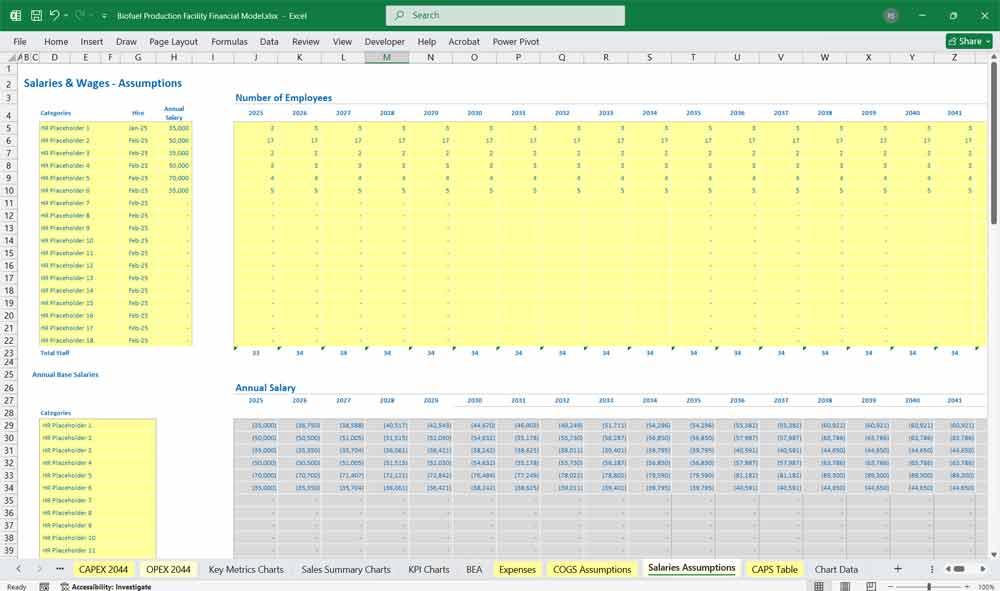

Direct Labor: Wages and benefits for plant operators and technicians.

Utilities: Electricity, natural gas, water, and wastewater treatment costs.

C. Gross Profit

Gross Profit = Total Revenue – COGS

Gross Margin (%) = (Gross Profit / Total Revenue) x 100. This indicates the core production efficiency.

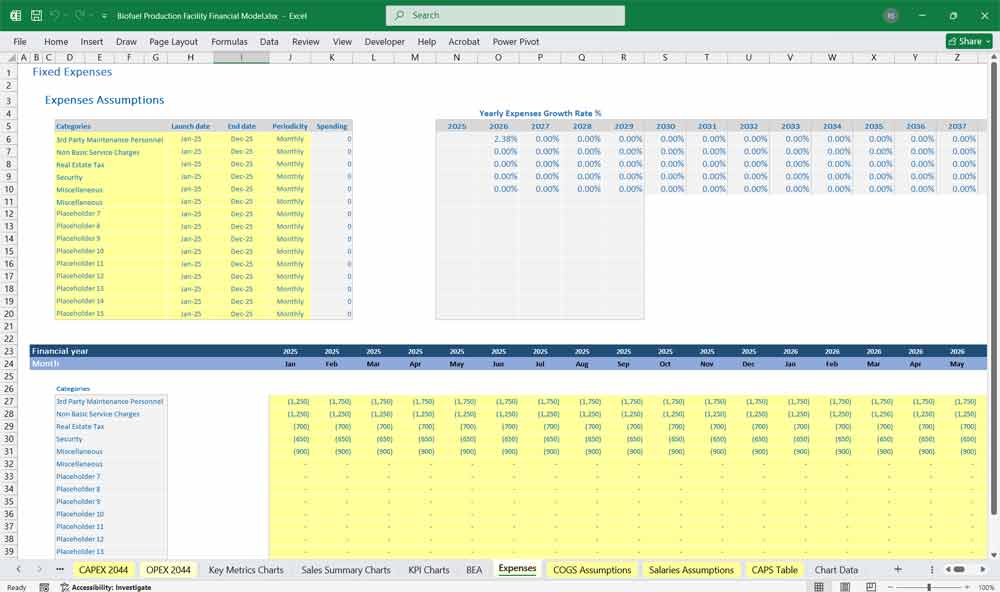

D. Operating Expenses (OpEx)

Fixed Operating Costs: Salaries for administrative staff, insurance, property taxes, and plant security.

Maintenance Costs: Both routine maintenance and an annual allocation for major overhauls (often a percentage of CapEx).

Selling, General & Administrative (SG&A): Marketing, sales commissions, legal, accounting, and corporate overhead allocations.

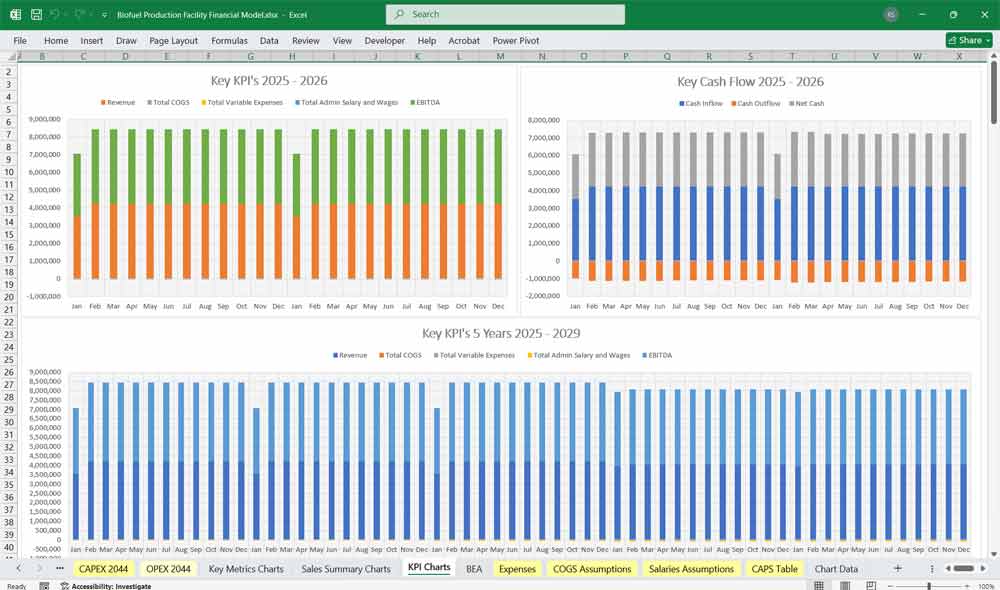

E. EBITDA & EBIT

EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) = Gross Profit – Operating Expenses. This is a key metric for comparing operational performance and debt-servicing capability.

Depreciation & Amortization: The non-cash charge that allocates the cost of capital assets over their useful life.

EBIT (Earnings Before Interest and Taxes) = EBITDA – Depreciation & Amortization. Also known as Operating Income.

F. Net Income

Interest Expense: Cash cost of servicing the project’s debt.

Pre-Tax Income = EBIT – Interest Expense.

Income Taxes: Calculated on Pre-Tax Income, considering tax shields from depreciation and interest.

Net Income = Pre-Tax Income – Income Taxes. The final “bottom-line” profit.

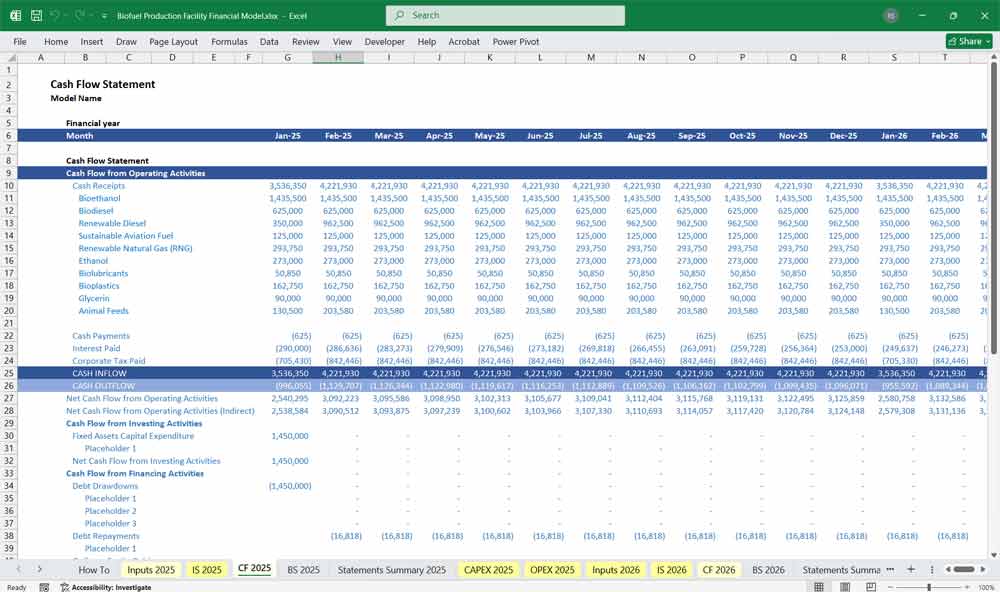

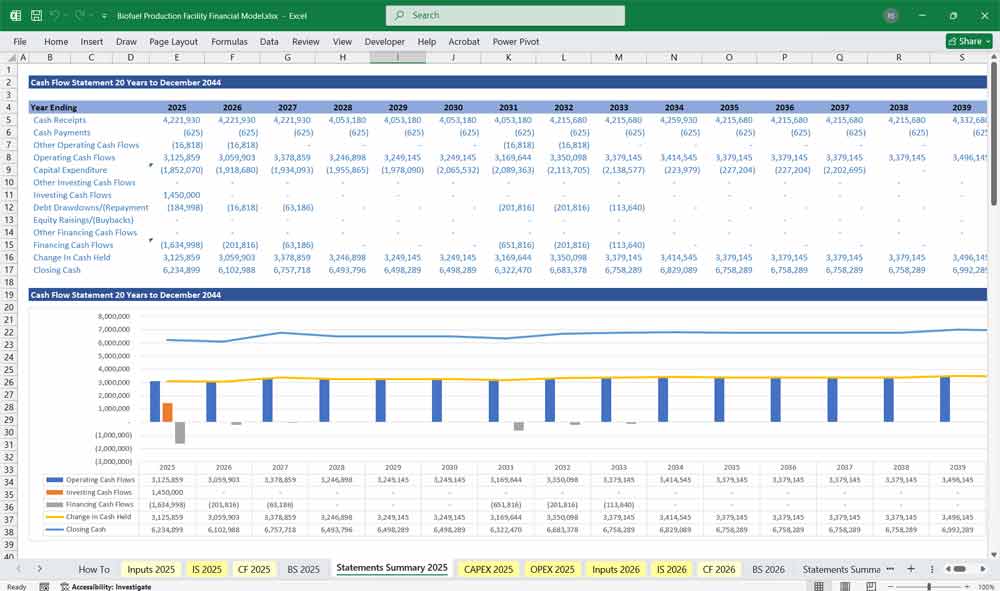

Biofuel Production Plant Cash Flow Statement

This statement tracks the actual movement of cash in and out of the business, crucial for understanding liquidity.

A. Cash Flow from Operating Activities

Starts with: Net Income.

Add Back: Non-cash expenses (Depreciation, Amortization).

Changes in Working Capital:

Increase in Inventory / Receivables: Uses cash.

Increase in Payables: Provides cash.

This section models the timing difference between receiving cash from customers and paying suppliers.

B. Cash Flow from Investing Activities

Capital Expenditures (CapEx):

Initial CapEx: The total cash outlay for the project’s construction in Year 0.

Sustaining CapEx: Ongoing capital expenditures for equipment replacements and upgrades throughout the project’s life.

C. Cash Flow from Investing Activities

Debt Drawdown: The initial inflow of cash from the loan at project financial close.

Equity Investment: The inflow of cash from equity investors.

Debt Principal Repayment: The annual cash outflow to pay down the loan balance.

Dividends / Distributions: Cash outflows to equity investors after debt obligations are met.

D. Net Change in Cash & Ending Cash Balance

Net Cash Flow = Sum of Cash from Operations, Investing, and Financing.

Ending Cash Balance = Beginning Cash Balance + Net Cash Flow.

This ending balance is critical for ensuring the company never runs out of cash (i.e., avoids a cash deficit).

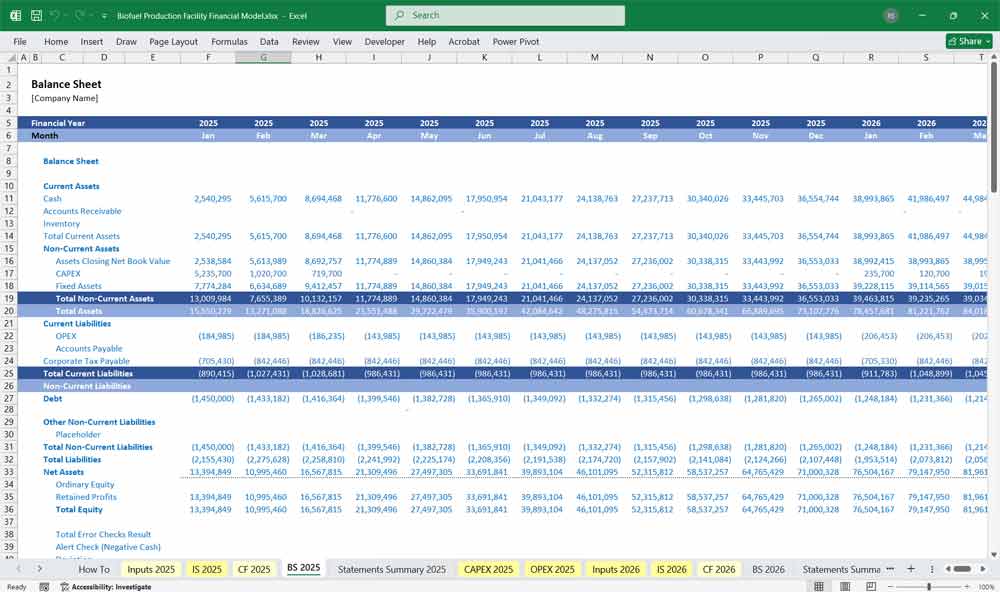

Biofuel Production Plant Balance Sheet

This provides a snapshot of the company’s financial position at a specific point in time (end of each year).

A. Assets (What the Company Owns)

Current Assets:

Cash & Cash Equivalents: The final figure from the Cash Flow Statement.

Accounts Receivable: Money owed by customers for products sold.

Inventory: Value of stored feedstock, work-in-progress, and finished goods.

Non-Current Assets:

Property, Plant & Equipment (PP&E): The original CapEx cost minus accumulated depreciation. This is the “book value” of the physical plant.

Other Assets: Prepaid expenses, rights-of-way, etc.

B. Liabilities (What the Company Owes)

Current Liabilities:

Accounts Payable: Money owed to feedstock suppliers and other vendors.

Accrued Expenses: Wages, taxes, and interest that are owed but not yet paid.

Current Portion of Long-Term Debt: The portion of the main loan due within the next 12 months.

Non-Current Liabilities:

Long-Term Debt: The principal amount of the loan outstanding, minus the current portion.

C. Shareholders’ Equity

Paid-in Capital: The total amount of money invested by shareholders.

Retained Earnings: The cumulative total of all Net Income earned over the life of the project, minus any dividends paid out.

The Accounting Equation must always hold:

Total Assets = Total Liabilities + Shareholders’ Equity

Key Outputs & Metrics For A Biofuel Production Plant

The model synthesizes the three statements to calculate critical investment metrics:

Net Present Value (NPV): The sum of all future annual Free Cash Flows, discounted back to today’s value using the project’s Weighted Average Cost of Capital (WACC). A positive NPV indicates a value-creating project.

Internal Rate of Return (IRR): The discount rate that makes the NPV equal to zero. This is the project’s effective annual return and is compared to the investor’s hurdle rate.

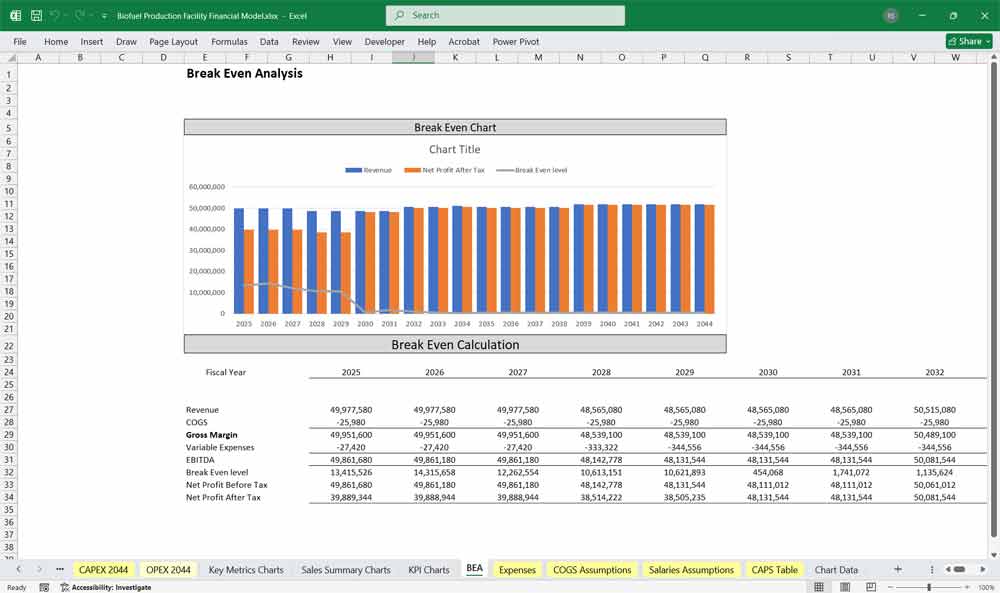

Debt Service Coverage Ratio (DSCR): (EBITDA – Sustaining CapEx – Taxes) / Total Annual Debt Service. Lenders require a minimum DSCR (e.g., 1.30x) to ensure sufficient cash flow to cover loan payments.

Loan Life Coverage Ratio (LLCR): The present value of future cash flows available for debt service divided by the outstanding debt balance. A measure of the overall debt repayment safety margin.

Payback Period: The number of years required for the cumulative cash flow to repay the initial equity investment.

Long-Term Viability For Your Biofuel Plant

A 20-year model is essential for accurately capturing the long-term economic viability and strategic value of a biofuel production plant. Unlike shorter-term projects, a biorefinery requires massive upfront capital investment (CapEx) in highly specialized equipment and technology. A model of this duration allows investors and lenders to see the full picture, demonstrating how the project will transition from a cash-intensive startup phase through to stable operations and, crucially, into a period of strong positive cash flows that deliver a satisfactory return on investment. It provides the necessary timeline to prove that the project can not only service its debt but also generate substantial profits over its entire economic life, making the initial financial risk palatable.

20 Years Of Biofuel Industry Economics

Furthermore, a 20-year horizon is critical for modeling the complex and volatile incentive structures that underpin the biofuel industry’s economics. Key revenue drivers like the federal Renewable Fuel Standard (RINs), California’s Low Carbon Fuel Standard (LCFS) credits, and tax incentives under the Inflation Reduction Act (IRA) are policy-dependent and have multi-year compliance cycles. A long-term model can incorporate sophisticated forecasts for these credit prices, including phase-outs, policy shifts, and the growing value of lower carbon intensity pathways. It also allows for the planning of technology upgrades to further reduce the carbon score, thereby maximizing the value of the plant’s output over decades, not just the first few years of operation.

20 Years Of Biofuel Market Fluctuation Monitoring

Finally, this extended timeframe provides the strategic flexibility needed to navigate market evolution and optimize product slates. A 20-year model can scenario-test the impact of shifting from a primary product like biodiesel to higher-value products like Sustainable Aviation Fuel (SAF) or Renewable Natural Gas (RNG) as market demand and profitability change. It can account for feedstock cost fluctuations, the development of new supply chains, and the planned cycles of sustaining capital expenditures for equipment refurbishment. In essence, a 20-year model is not just a static spreadsheet; it is a dynamic strategic roadmap that demonstrates the management team’s long-term vision and the project’s resilience and adaptability in a rapidly evolving energy landscape.

Final Notes on the Financial Model

This 20 Year Biofuel Production Plant Financial Model focuses on balancing capital expenditures with steady revenue growth from a diversified production line. By optimizing operational costs, and power efficiency, and maximizing high-margin services, the models ensure sustainable profitability and cash flow stability.

Download Link On Next Page, view the template description