Biochemical Fermentation Plant Financial Model

This 20-Year, 3-Statement Excel Biochemical Fermentation Plant Financial Model includes revenue streams from up to 80 product lines and a 6 Tier Subscrption add-on to track the revenue of your repeat orders. CAPEX and OPEX Spreadsheets, A Discounted Cash Flow (DCF) with Terminal Value, Sensitivity Analysis, and WACC Model add-on. Cost structures and financial statements to forecast the financial health of your Biochemical Plant.

20-Year Financial Model for a Biochemical Fermentation Plant

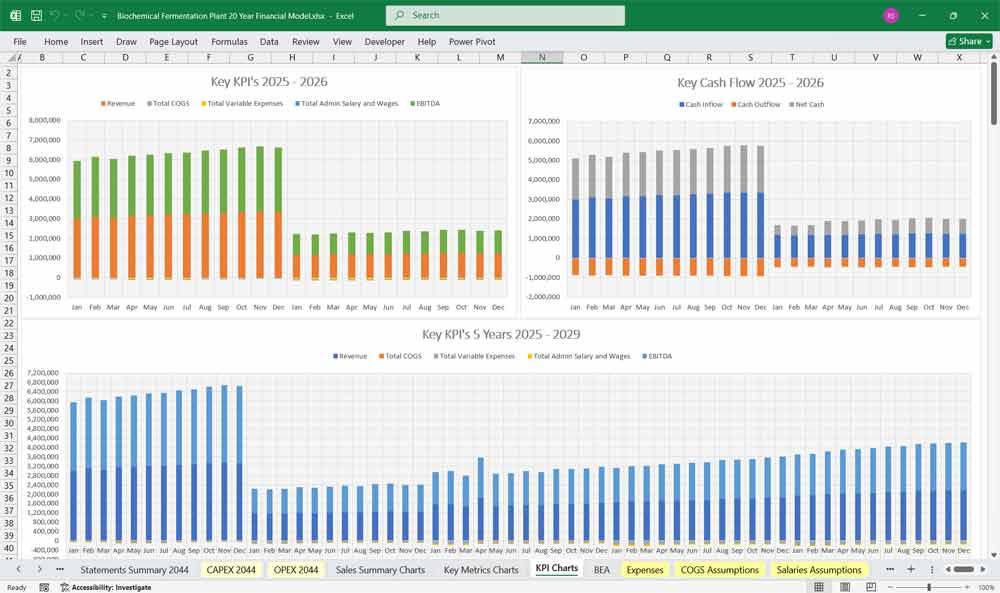

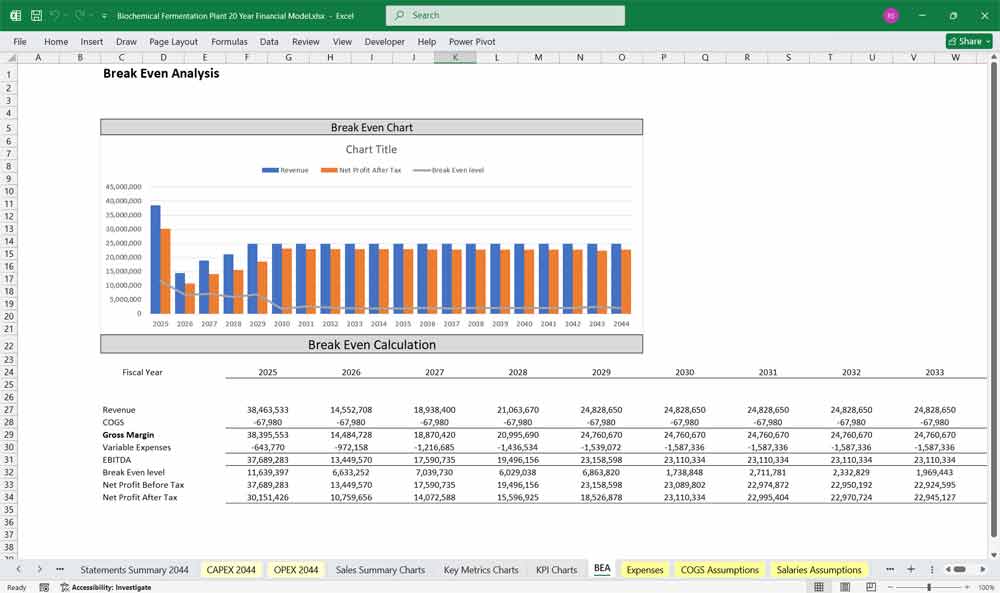

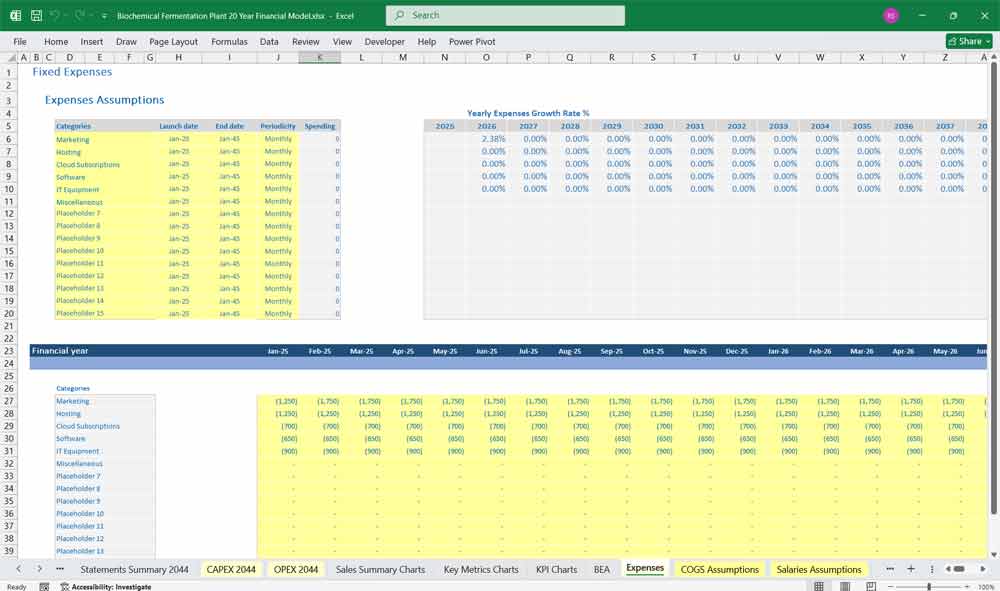

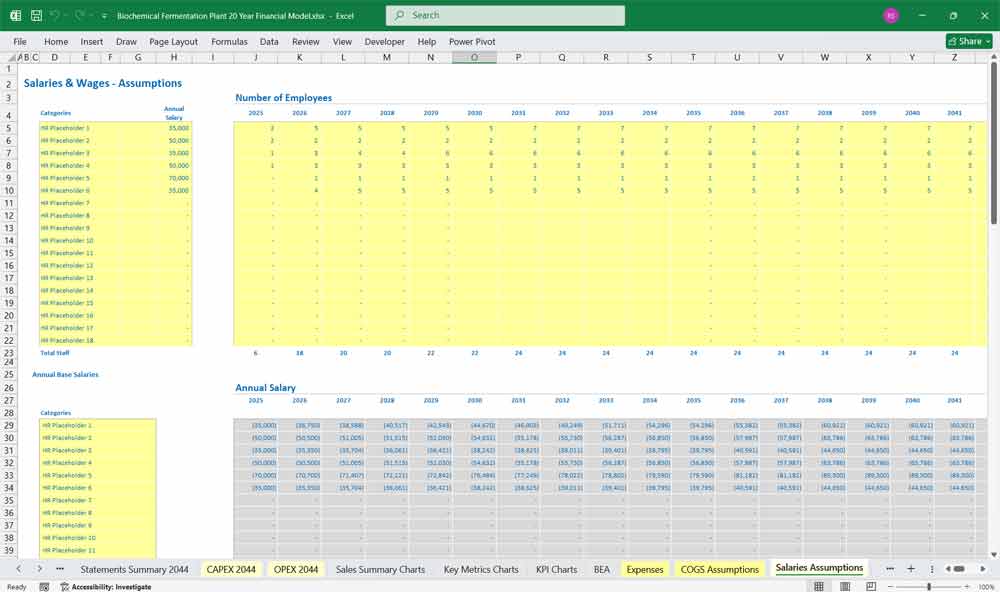

This very extensive 20 Year Biochemical Plant Model involves detailed revenue projections, cost structures, capital expenditures, and financing needs. This model provides a thorough understanding of the financial viability, profitability, and cash flow position of your manufacturing company. Includes: 20x Income Statements, Cash Flow Statements, Balance Sheets, CAPEX sheets, OPEX Sheets, Statement Summary Sheets, and Revenue Forecasting Charts with the revenue streams, BEA charts, sales summary charts, employee salary tabs and expenses sheets.

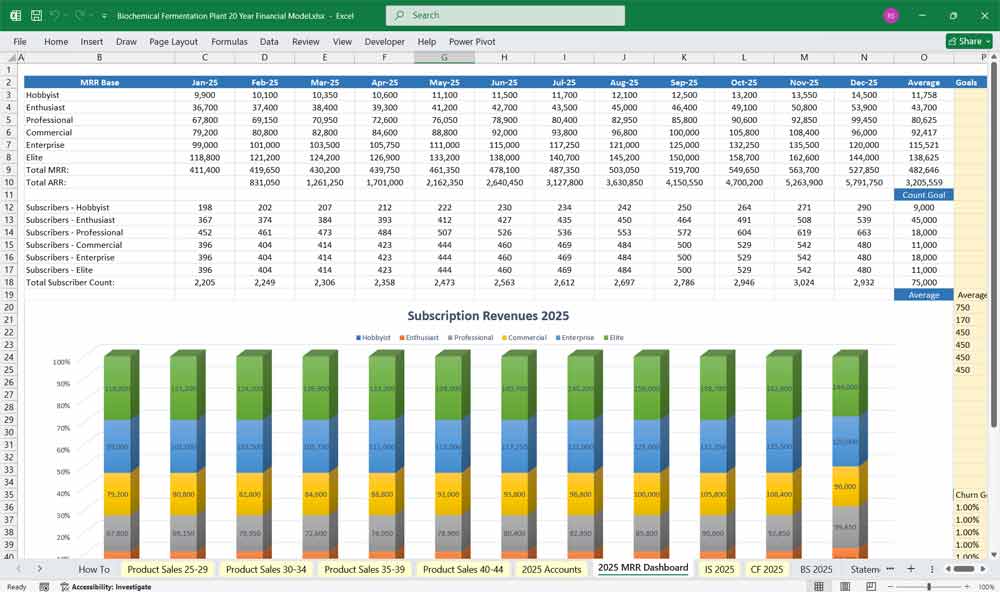

80 Product Line Examples

This section is the operational heart of the model, translating biological and industrial efficiency into financial numbers.

A. Bulk Bio-products (e.g., Enzymes, Organic Acids, Bioethanol):

Volume: High volume (tons or millions of liters).

Price: Low to moderate price per unit mass/volume. Highly competitive market.

Key Cost Drivers: Feedstock cost (e.g., corn syrup, molasses), energy consumption for agitation and aeration, and yield (conversion efficiency).

Assumptions: High utilization rates are critical for profitability. Economies of scale are a significant factor.

B. High-Purity Specialties (e.g., Amino Acids, Vitamins, Cosmetic Actives):

Volume: Medium volume (kilograms to tons).

Price: Moderate to high price. Value is driven by purity and specific functionality.

Key Cost Drivers: Cost of specialized precursors, tighter quality control, and more complex downstream purification (e.g., chromatography, crystallization).

Assumptions: Higher R&D costs and more stringent regulatory compliance.

C. Pharmaceutical Intermediates & APIs (Active Pharmaceutical Ingredients):

Volume: Low volume (grams to kilograms).

Price: Very high price. Driven by strict regulatory requirements (cGMP) and high efficacy.

Key Cost Drivers: Extremely high-purity raw materials, extensive validation, quality control/assurance, and significant waste handling costs.

Assumptions: Long lead times, rigorous regulatory approval processes, and long-term supply contracts provide stable but hard-to-obtain revenue.

D. Novel Products (e.g., Precision Fermented Proteins, Biopolymers):

Volume: Variable, depending on market adoption.

Price: Premium pricing due to novelty and sustainability claims.

Key Cost Drivers: High R&D, market development, and potentially expensive, non-commoditized feedstocks.

Assumptions: This line carries the highest risk but also the highest potential growth and margins. It requires separate assumptions for market penetration rates.

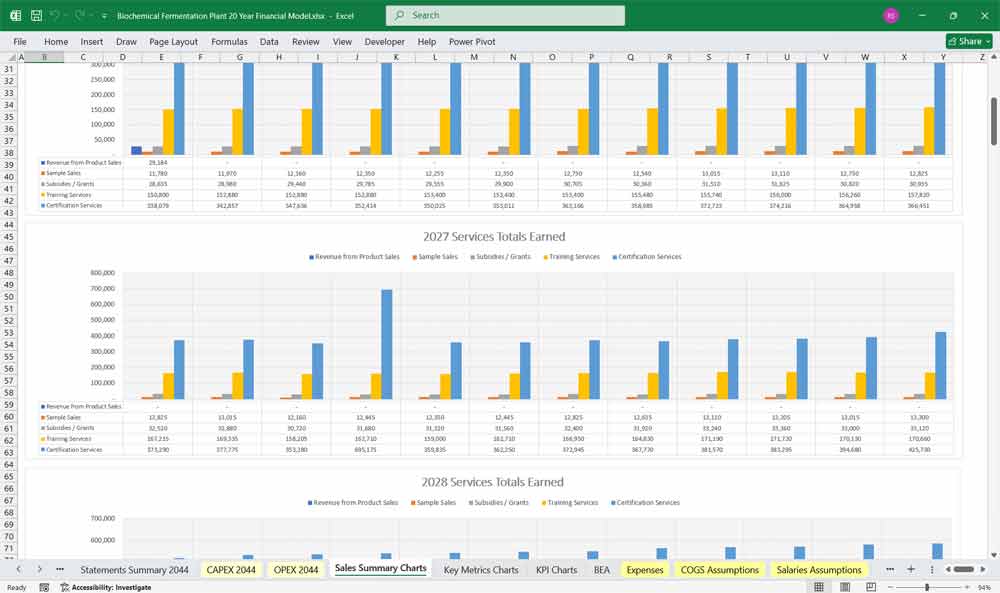

For each product line, the model will calculate:

Total Production Volume = (Fermenter Capacity) x (Utilization Rate) x (Yield)

Total Revenue = (Production Volume) x (Selling Price)

Direct Cost of Goods Sold (COGS) = (Feedstock Cost) + (Utilities Cost) + (Direct Labor) + (Consumables)

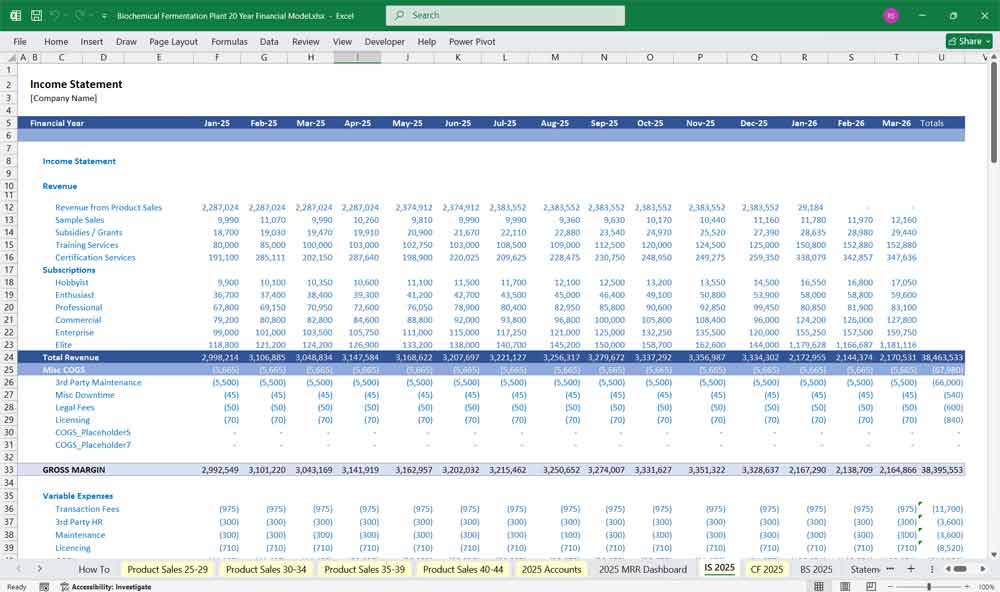

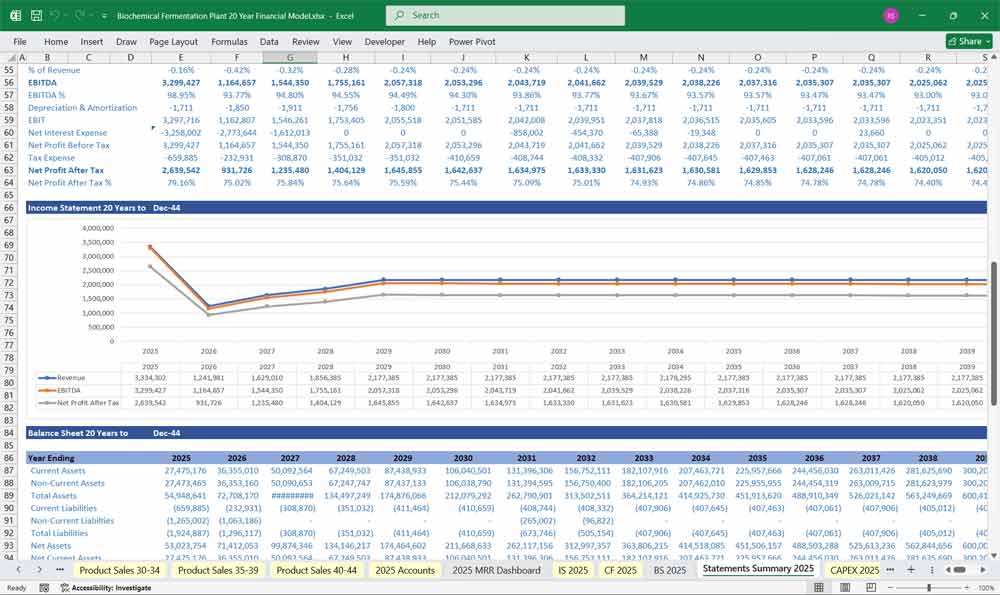

Income Statement (Profit & Loss Statement)

The Income Statement shows profitability over a period (e.g., one year).

Revenue:

Calculated from the Editable Product Lines section as the sum of revenues from:

- Contract Manufacturing (CMO) Services

- Downstream Processing (DSP) and Purification

- Process Optimization and Development

- Microbial Strain Development and Banking

May include deductions for royalties, rebates, and returns.

Cost of Goods Sold (COGS):

Direct Raw Materials: Cost of carbon sources (e.g., glucose), nitrogen sources (e.g., yeast extract), salts, and precursors.

Utilities: Cost of steam, electricity (a major cost for agitators and compressors), cooling water, and compressed air.

Direct Labor: Salaries of fermentation and purification operators.

Plant Overhead: Allocation of costs for maintenance, quality control lab, and plant management.

Gross Profit: = Revenue – COGS

Gross Margin: = (Gross Profit / Revenue) x 100%. This is a key indicator of production efficiency.

Operating Expenses (OpEx):

Research & Development (R&D): Strain improvement, process optimization, pilot-scale trials.

Sales, General & Administrative (SG&A): Salaries for sales and admin staff, marketing, legal, insurance.

Regulatory & Quality Assurance: Costs of maintaining cGMP/other certifications and conducting audits.

Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA): = Gross Profit – Operating Expenses. A measure of core operational profitability.

Depreciation & Amortization (D&A): A non-cash expense that allocates the cost of CapEx assets over their useful life. Fermenters might be depreciated over 15 years, lab equipment over 7.

Earnings Before Interest and Taxes (EBIT) / Operating Income: = EBITDA – D&A.

Interest Expense: Calculated based on the outstanding debt balance from the Balance Sheet and the assumed interest rate.

Pre-Tax Income: = EBIT – Interest Expense.

Income Taxes: Applied at the prevailing corporate tax rate.

Net Income: = Pre-Tax Income – Income Taxes. The final “bottom-line” profit.

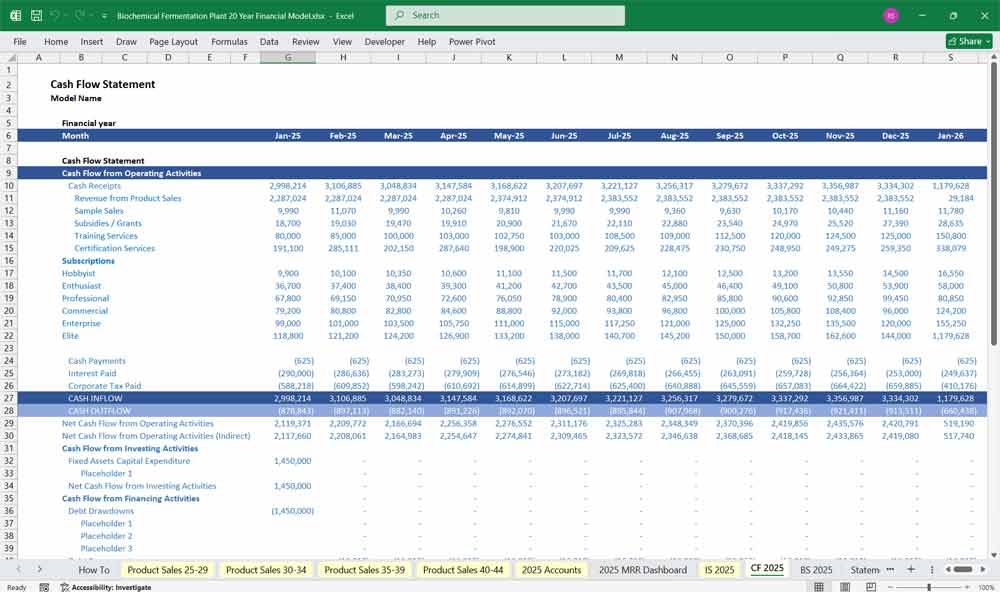

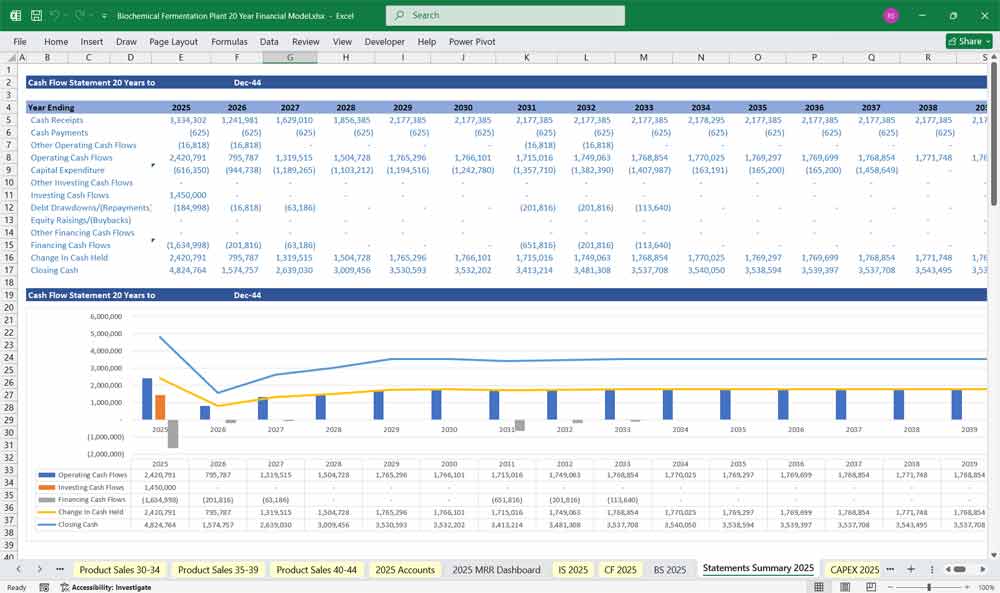

Biochemical Fermentation Plant Cash Flow Statement

The Cash Flow Statement tracks the actual movement of cash, separated into three categories.

Cash Flow from Operating Activities (CFO):

Starts with Net Income.

Add back non-cash expenses (Depreciation & Amortization).

Adjust for changes in Working Capital:

Increase in Accounts Receivable: Represents sales made but not yet paid for, which is a use of cash.

Increase in Inventory: Represents raw materials or finished goods produced but not sold, a use of cash.

Increase in Accounts Payable: Represents bills not yet paid, which is a source of cash.

Net CFO is a critical indicator of the business’s ability to generate cash from its core operations.

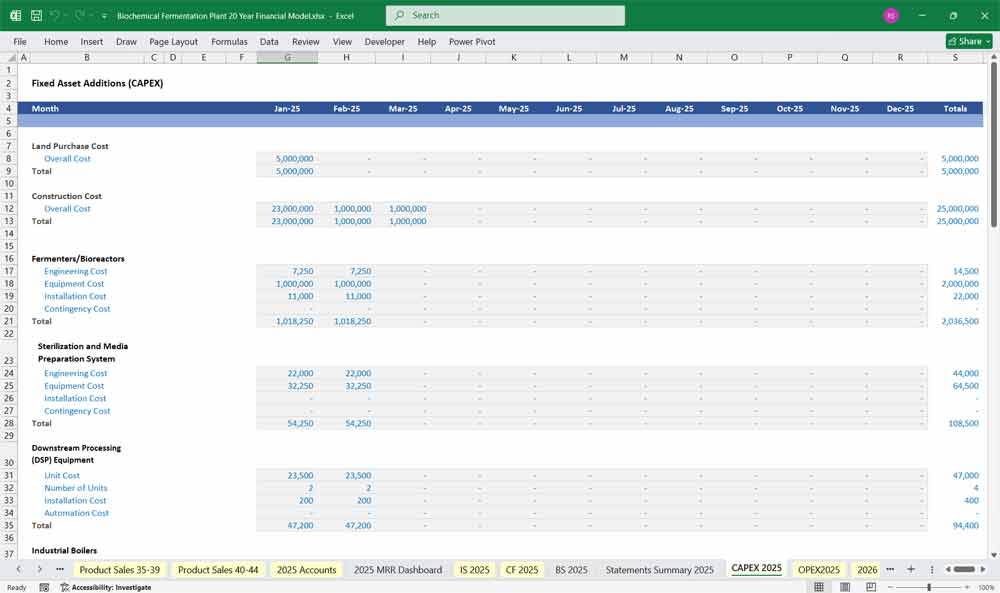

Cash Flow from Investing Activities (CFI):

Consists almost entirely of Capital Expenditures (CapEx).

This includes payments for land, building construction, fermenters, downstream processing equipment, and lab fit-outs.

This is typically a significant negative (outflow) in the early years.

Cash Flow from Financing Activities (CFF):

Inflows: Proceeds from issuing equity (investor funds) and drawing down debt (loans).

Outflows: Repayment of debt principal (not interest, which is in the Income Statement) and payment of dividends to shareholders.

Net Change in Cash: = CFO + CFI + CFF.

Ending Cash Balance: = Beginning Cash Balance + Net Change in Cash. This Ending Cash balance flows to the Balance Sheet.

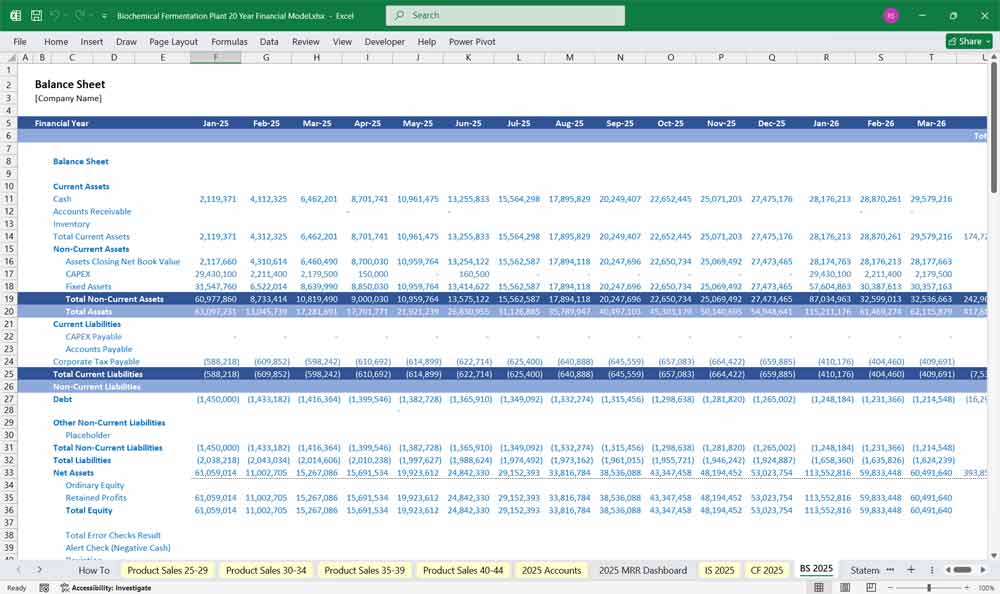

Biochemical Fermentation Plant Balance Sheet

The Balance Sheet provides a snapshot of the plant’s financial position at year-end, reflecting assets, liabilities, and equity.

Structure:

Assets

Current Assets:

Cash & Cash Equivalents

Accounts Receivable

Inventory (feedstock, WIP, finished goods)

Prepaid Expenses

Non-Current Assets:

Property, Plant & Equipment (PP&E):

Fermenters, downstream processing, utilities, land, buildings

Depreciated using straight-line or accelerated methods

Intangible Assets (patents, process licenses, goodwill)

Deferred Tax Assets

Liabilities

Current Liabilities:

Accounts Payable

Short-Term Loans

Accrued Expenses

Current Portion of Long-Term Debt

Non-Current Liabilities:

Long-Term Debt

Lease Liabilities

Deferred Tax Liabilities

Provisions (decommissioning, maintenance reserves)

Equity

Paid-in Capital (shareholders’ equity)

Retained Earnings

Other Comprehensive Income

Balance Check:

Total Assets = Total Liabilities + Equity

Key Biochemical Fermentation Plant Industry-Specific Considerations

High Fixed Cost Base: Equipment-heavy industry with high depreciation.

R&D Intensity: Critical for staying competitive.

Quality & Certification: Failure costs can be catastrophic (scrap, rework).

Cyclicality & Diversification: Aerospace/automotive cycles affect volumes.

20-Year Biochemical Fermentation Plant Financial Model Advantages

A 20-year financial model is indispensable for navigating the substantial upfront investment and long development cycles inherent to a biochemical fermentation plant. Unlike a standard business, such a facility faces enormous initial capital expenditures (CapEx) for specialized fermenters, downstream purification equipment, and stringent quality control labs, coupled with years of research, strain development, and regulatory approvals before a product can be commercially launched. A model spanning two decades is essential to accurately capture the true return on investment, demonstrating how these early-year losses and massive cash outflows are gradually offset by stable, high-margin revenue in the out-years. This long-term view is critical for securing patient capital from investors—such as venture capital, private equity, or strategic partners—who understand the deep-tech bio-economy and are focused on the potential for a substantial payoff over a longer horizon.

20 Years of Biochemical Fermentation Plant Strategic Planning

Furthermore, the extended timeline allows for sophisticated strategic planning and product lifecycle management. A biochemical plant is not a static operation; its core technology can be leveraged to produce a pipeline of products. A 20-year model provides the framework to strategically plan the transition from a single flagship product to a diversified portfolio. It can map out the commercialization of higher-margin products—such as moving from bulk enzymes to pharmaceutical intermediates—and schedule crucial future investments in capacity expansion or technology upgrades without jeopardizing financial stability. This forward-looking approach enables management to make informed decisions about when to retire older product lines and re-tool fermenters for new, more profitable applications, ensuring the plant remains competitive and technologically relevant for decades.

Detailed scenario analysis For Your Biochemical Plant

this comprehensive model is a vital tool for risk mitigation and resilience planning. The bio-based industry is subject to volatile feedstock costs, shifting regulatory landscapes, and rapid technological disruption. A 20-year model allows management to run detailed sensitivity and scenario analyses, testing the plant’s vulnerability to these long-term risks. For instance, it can project the financial impact of a key patent expiring in Year 12, a 20% increase in raw material costs in Year 15, or the arrival of a disruptive competitive technology in Year 8. By stress-testing the business case against these potential futures, management can develop robust contingency plans, secure long-term supply contracts, and build financial buffers, thereby transforming the model from a static spreadsheet into a dynamic roadmap for enduring success.

Benefits of an 80 Product Line Model for your Biochemical Plant

Operating a biochemical fermentation plant with a portfolio of up to 80 product lines across sectors like biofuels, pharmaceuticals, industrial enzymes, food and beverage, and biomaterials creates an unparalleled competitive advantage through profound risk mitigation. This vast diversification insulates the company from volatility in any single market. A downturn in the biofuel sector due to shifting energy policies, for instance, would have a minimal overall impact if it is counterbalanced by stable, high-margin revenue from essential pharmaceuticals like insulin and vaccines, or consistent demand for industrial enzymes for detergents. Similarly, seasonal fluctuations in food and beverage production can be absorbed by the steady output of bioplastics or specialty chemicals. This strategic spread ensures a stable revenue base, making the business resilient to economic cycles, regulatory changes, and market disruptions that would critically threaten a single-product facility.

Biochemical Plant Offering 80 Product Lines

This model shows the potential to unlock powerful operational synergies and maximizes asset utilization. The core fermentation and downstream processing infrastructure is often adaptable across product lines. A single fermenter could be sequenced to produce a batch of industrial enzymes for textiles, followed by a campaign of amino acids for food fortification, and then a run of lactic acid for bioplastics. This flexibility allows the plant to dynamically allocate its capacity to the highest-margin products at any given time, ensuring that no capital asset sits idle. Expertise gained in optimizing high-yield processes for bulk products like sustainable ethanol can inform the scale-up of more complex compounds, while the stringent quality control protocols from pharmaceutical manufacturing elevate standards across all product lines, enhancing overall efficiency and product quality.

Biochemical Plant Diversification View

An 80-product line model transforms the view of the plant from a mere manufacturer into a dominant, innovation-driven platform in the bio-economy. This scale provides immense strategic leverage in sourcing raw materials, as bulk purchasing of feedstocks like corn syrup or sucrose becomes more cost-effective. In the marketplace, the ability to offer a one-stop-shop for a vast array of bio-based solutions—from drug ingredients and food additives to eco-friendly plastics and cleaning agents—creates unrivalled value for customers and significant barriers for competitors. This setup also fosters a unique internal innovation ecosystem where research and development in one area, such as discovering a new enzyme, can potentially unlock applications in another, like improving the efficiency of biofuel production or creating a novel biomaterial, ensuring the company remains at the forefront of industrial biotechnology for the long term.

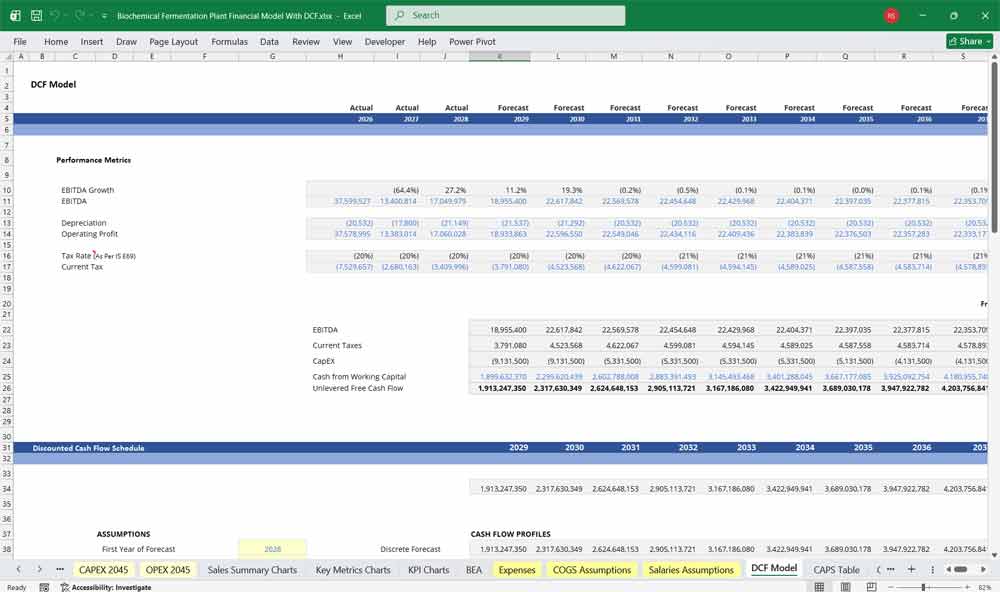

Valuing Your Biochemical Fermentation Plant With A DCF

Discounted Cash Flow: Valuing the Industrial-Scale Petri Dish

This 20-year Discounted Cash Flow (DCF) analysis for a biochemical fermentation plant, the valuation is a race between capital intensity and biological efficiency. The early years of the model are dominated by the “valley of death”—massive CapEx spent on stainless steel bioreactors, seed tanks, and downstream purification units. The DCF meticulously tracks the ramp-up of “titer” and “yield” (the concentration and efficiency of the microbes) as the plant moves from pilot scale to commercial production. By discounting the future revenues from high-value molecules—like bio-manufactured fragrances or specialty proteins—the model determines if the “microbial sweat” can ultimately pay back the significant upfront investment in hardware.

WACC: Pricing Scale-Up and Contamination Risk

The Weighted Average Cost of Capital (WACC) for a fermentation plant reflects a hybrid of manufacturing stability and “bio-industrial” anxiety. While more predictable than a clinical-stage biotech firm, the discount rate carries a premium to account for the risk of “scale-up failure,” where a microbe optimized in a lab underperforms in a 200,000-liter tank. In the 2026 market, the cost of debt is heavily influenced by the project’s “first-of-a-kind” (FOAK) status; lenders often demand higher interest rates until the plant proves its “steady-state” performance. This hurdle rate ensures the 20-year valuation is sufficiently “punished” for the risk of batch contamination or genetic drift that could halt production for weeks.

Sensitivity Analysis: Stress-Testing Feedstock and Recovery

For a biochemical fermentation plant, Sensitivity Analysis is the primary tool for measuring “metabolic profitability.” The most critical variables are feedstock costs (typically glucose or sugar) and downstream recovery rates (how much product is actually captured after the brewing is done). Analysts use sensitivity tables to see how a $50/tonne increase in sugar or a 5% drop in purification efficiency swings the unit cost of the final product. By stress-testing the model against “batch failure rates” and fluctuating energy prices for sterilization, the analysis reveals the project’s “break-even” biological performance, identifying the exact threshold where the microbes become more expensive than the traditional chemical processes they aim to replace.

Final Notes on the Financial Model

This 20 Year 80 product line Biochemical Fermentation Plant Financial Model focuses on balancing capital expenditures with steady revenue growth from diversified product lines. By optimizing operational costs, and power efficiency, and maximizing high-margin services, the models ensure sustainable profitability and cash flow stability.

Download Link On Next Page, view the template description.

Download Link On Next Page