Aluminum Smelter Financial Model

This 20-Year, 3-Statement Excel Aluminum Smelter Financial Model includes revenue streams from Ingot, Slab, and Billet Sales, OPEX cost structures, financial statements, Discounted Cash Flow (DCF) with Terminal Value, Sensitivity Analysis, and WACC, to forecast the financial health of your Aluminum Smelter.

20-year Financial Model for an Aluminum Smelter

3 Statement 20 Year Aluminum Smelter Model follows detailed revenue projections, cost structures, capital expenditures, and financing. Offers a thorough understanding of the financial viability, profitability, and cash flow position of the Smelter. Including: 20x Income and Cash Flow Statements, Balance Sheets, CAPEX and OPEX Sheets, Statement Summary Charts, and Revenue Forecasting and Projection Spreadsheets, with the specified revenue streams, 20-year BEA and sales summary charts, employee salary spreadsheets and expenses spreadsheets.

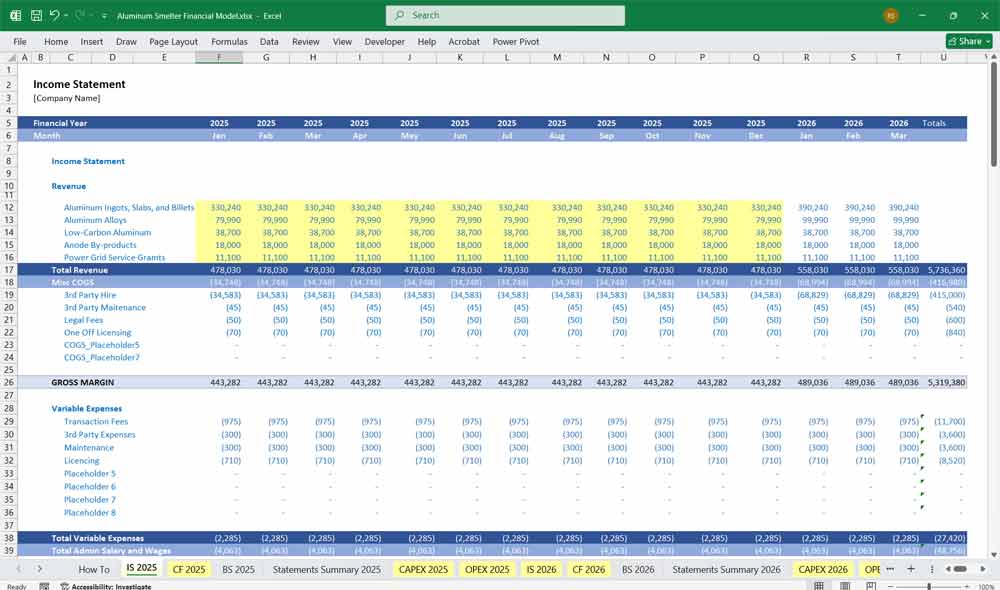

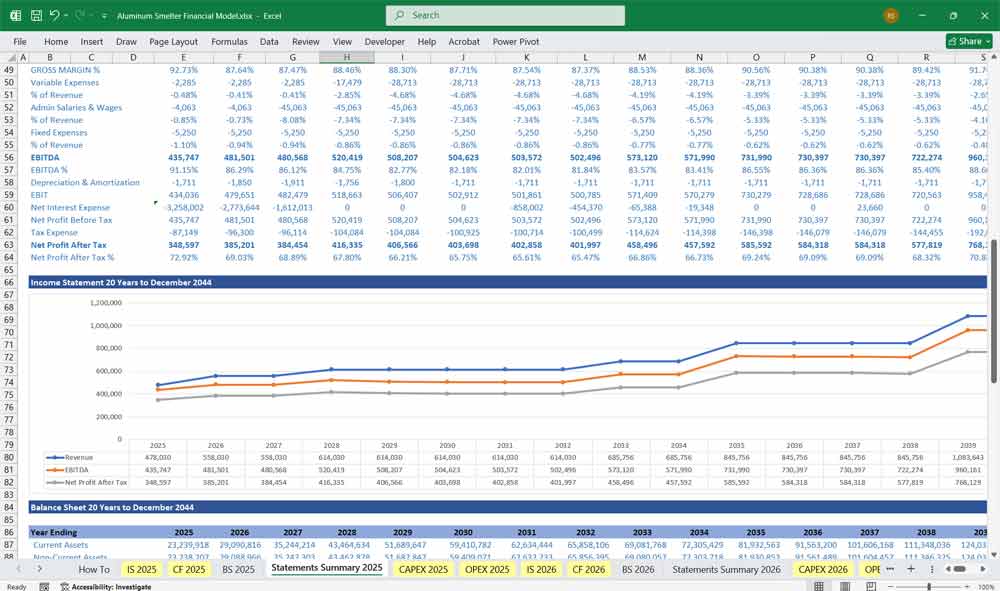

Income Statement

Revenue Streams

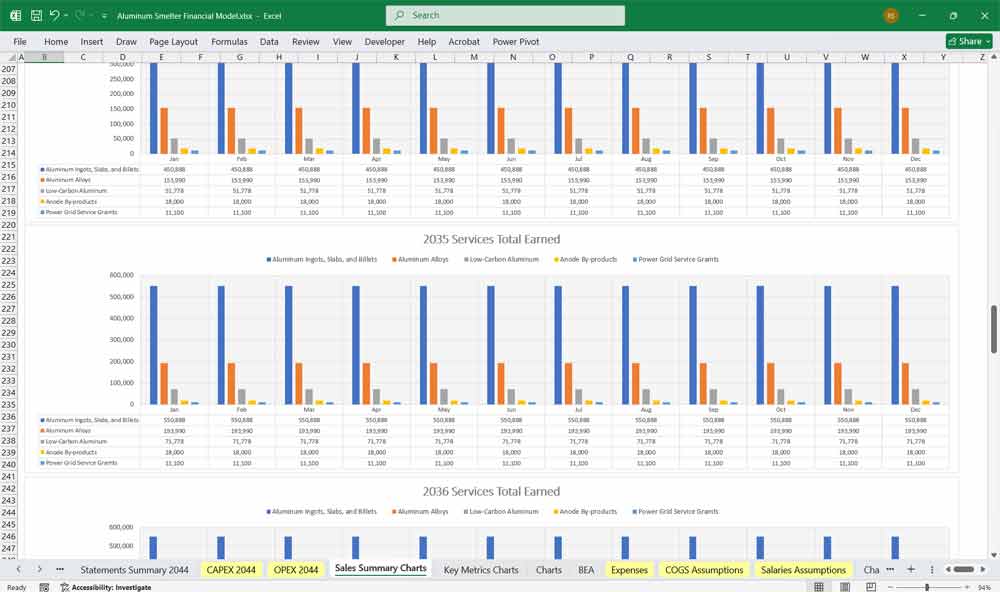

Aluminum Ingot Sales

Revenue is calculated as the volume of ingots sold multiplied by the market price per tonne.Aluminum Slab Sales

Slabs are semi-finished products used in rolling; sold at a slightly higher price than ingots.Aluminum Billet Sales

Billets are high-value, extrudable aluminum forms sold to downstream fabricators.Aluminum Alloy Sales

Includes specialty alloys sold at a premium due to customized chemical composition.Low-Carbon Aluminum Sales

Fetches a premium over standard aluminum; valued for ESG compliance and emissions certification.Anode By-product Sales

Includes tar, pitch, and other residuals from anode production—secondary revenue stream.Power Grid Service Grants

Income received from governments or utilities for providing demand response or grid stability services.

Total Revenue is the sum of all these product-based and service-based income sources.

OPEX

Raw Material Costs

Includes costs of alumina (or bauxite if refining is integrated), cryolite, and fluoride salts.Electricity Costs

The largest operating cost, based on kilowatt-hour usage per tonne of aluminum.Carbon Anode Consumption

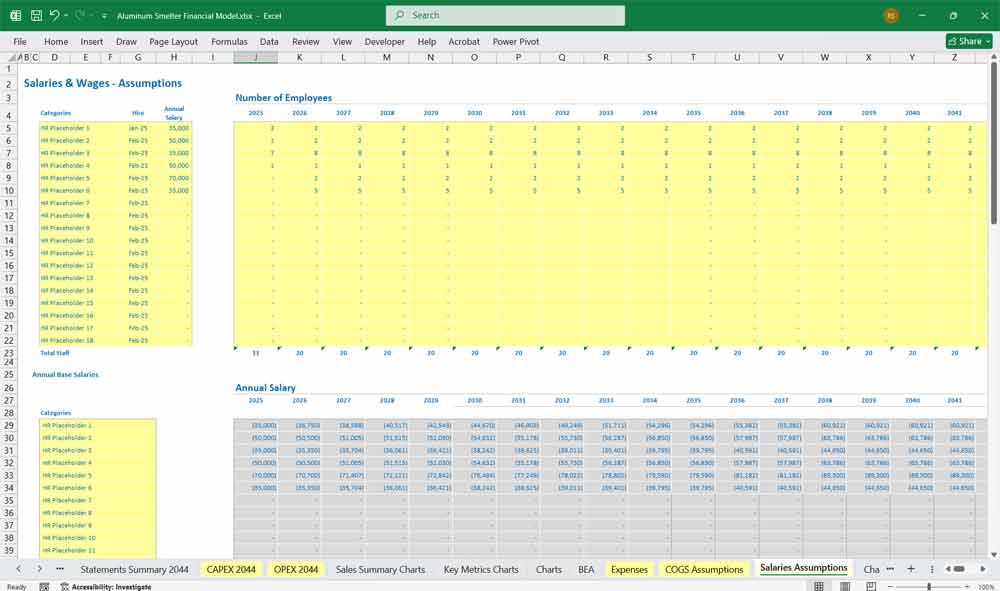

Includes cost of anodes, which are consumed during electrolysis and need regular replacement.Labor Costs (Direct)

Wages and benefits for plant operators, technicians, and maintenance staff.Maintenance and Consumables

Spare parts, refractory materials, lubricants, and general upkeep.Depreciation of Manufacturing Assets

Non-cash expense tied to plant and machinery in production.

Other Income and Expenses

Interest Income and Expenses (related to financing activities)

Foreign Exchange Gains or Losses (due to international sales or imports)

Hedging Gains or Losses (from commodity price or FX hedging)

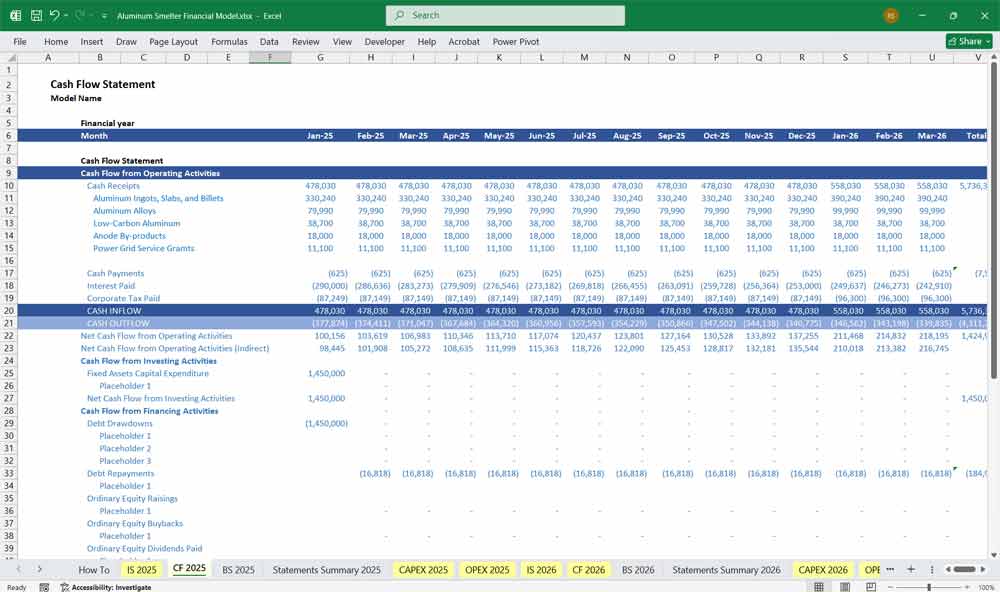

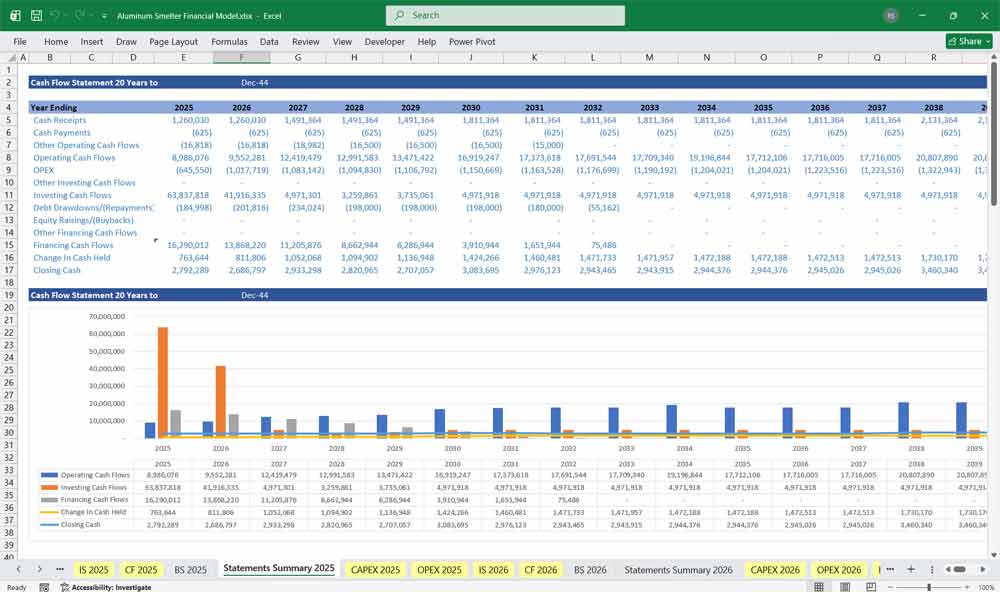

Aluminum Smelter Cash Flow Statement

Cash Flows from Operating Activities

Starts with Net Income

Adds back Depreciation and Amortization (non-cash)

Adjusts for changes in Working Capital (receivables, inventory, payables)

Deducts Taxes Paid

The result is Net Operating Cash Flow, representing core cash generation from the smelter.

Cash Flows from Investing Activities

Capital Expenditures: Large up-front investments in smelter construction, followed by recurring sustaining capex.

Asset Sales or Salvage: Sale of old equipment or land.

Other Investments: Potential investments in grid infrastructure or renewable energy.

The result is Net Investing Cash Flow.

Cash Flows from Financing Activities

Debt Issuance and Repayments: Project finance loans, bonds, or credit facilities.

Equity Infusions: Capital from shareholders.

Dividend Payments: Cash distributed to shareholders (if applicable).

The result is Net Financing Cash Flow.

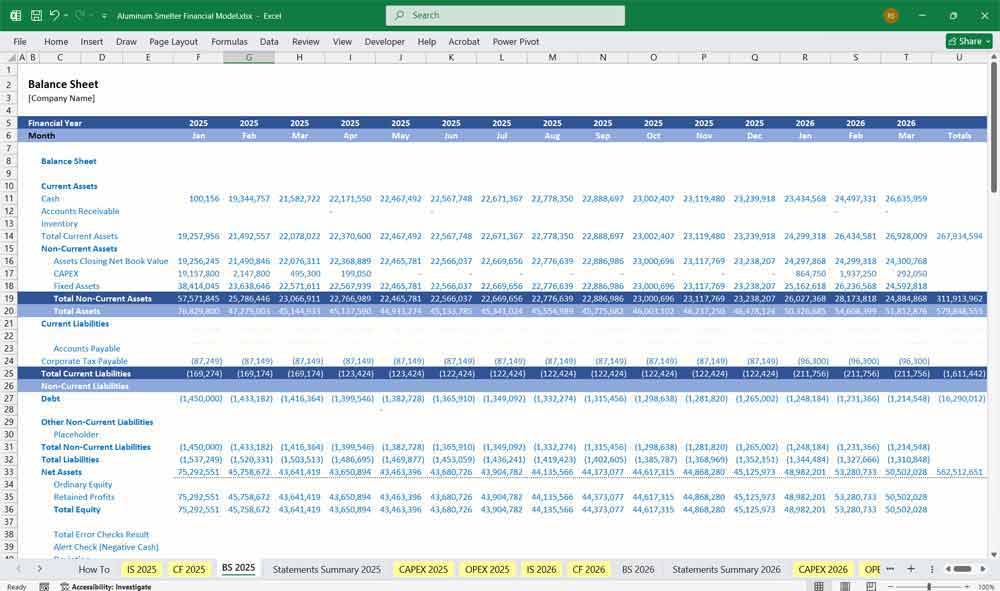

Aluminum Smelter Balance Sheet

Assets

Current Assets: Includes cash, accounts receivable, and inventories (raw materials, WIP, finished goods).

Property, Plant & Equipment (PPE): Smelter, potlines, rolling/casting facilities, and substations.

Intangible Assets: Software, licenses, emissions trading permits.

Deferred Tax Assets: Arise from temporary timing differences.

Liabilities

Current Liabilities: Accounts payable, accrued expenses, and current portion of long-term debt.

Long-Term Liabilities: Includes loans, bonds, and environmental provisions.

Deferred Tax Liabilities: May arise due to accelerated depreciation.

Equity

Share Capital: Contributions from shareholders.

Retained Earnings: Cumulative profits retained in the business.

Reserves: May include revaluation or currency translation reserves.

The accounting identity must hold: Assets = Liabilities + Equity

Aluminum Smelter Optional Enhancements

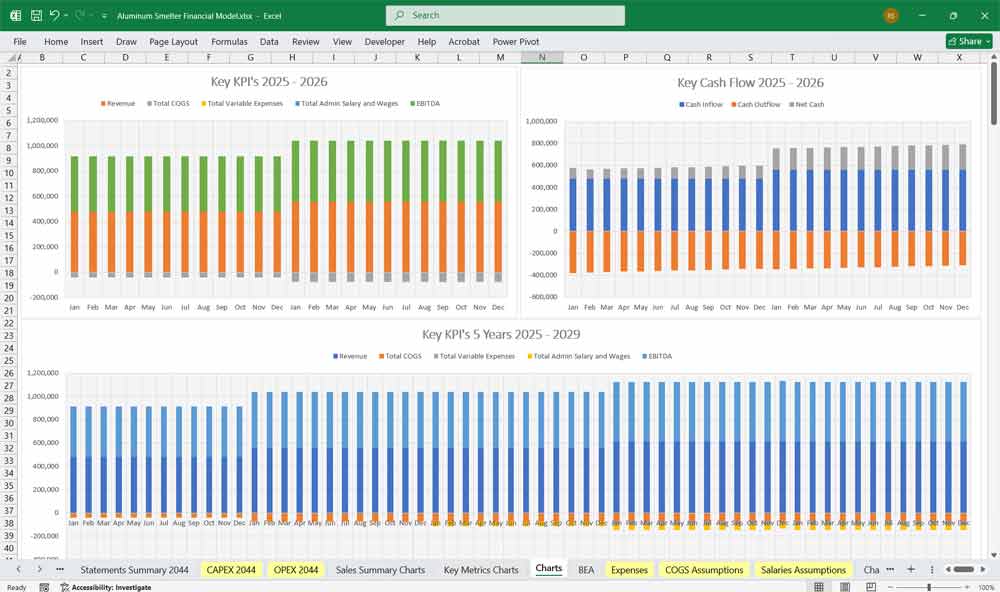

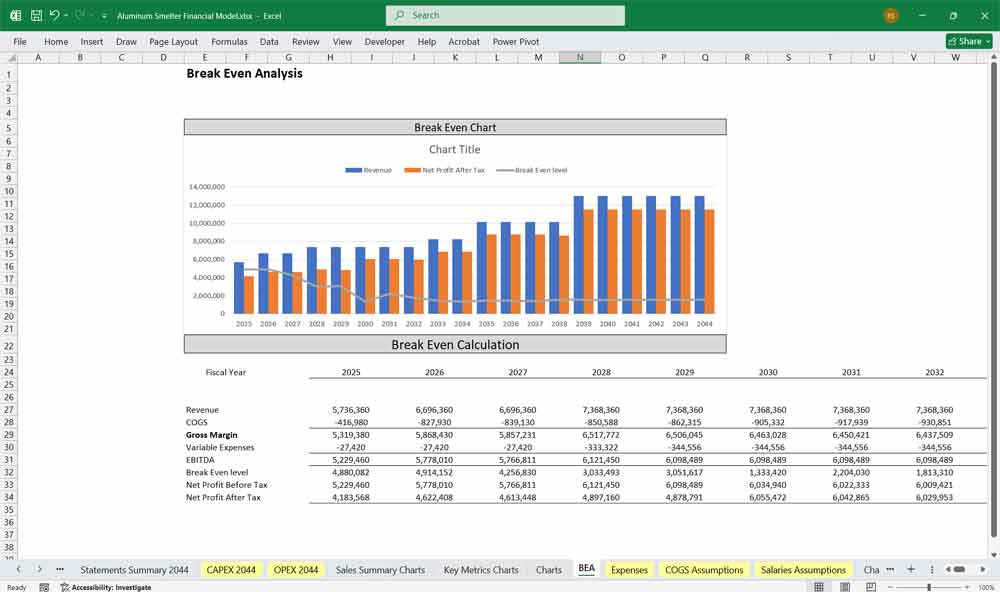

Key Metrics to Monitor

EBITDA and EBIT margins

Free Cash Flow

Production Cost per Tonne

Premium Realization from Low-Carbon Aluminum

Debt-to-Equity Ratio

Net Present Value (NPV) and IRR (for investment modeling)

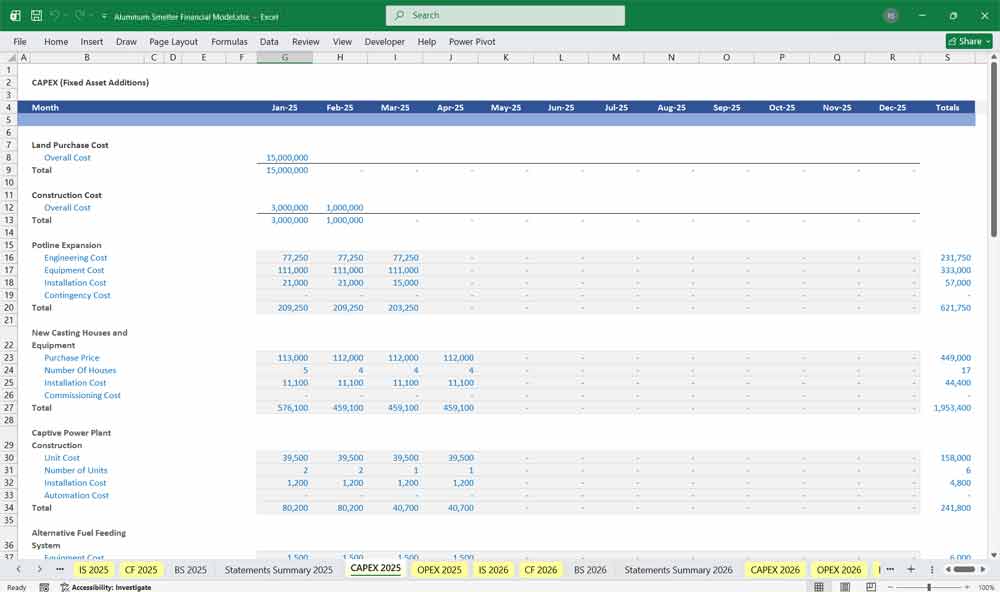

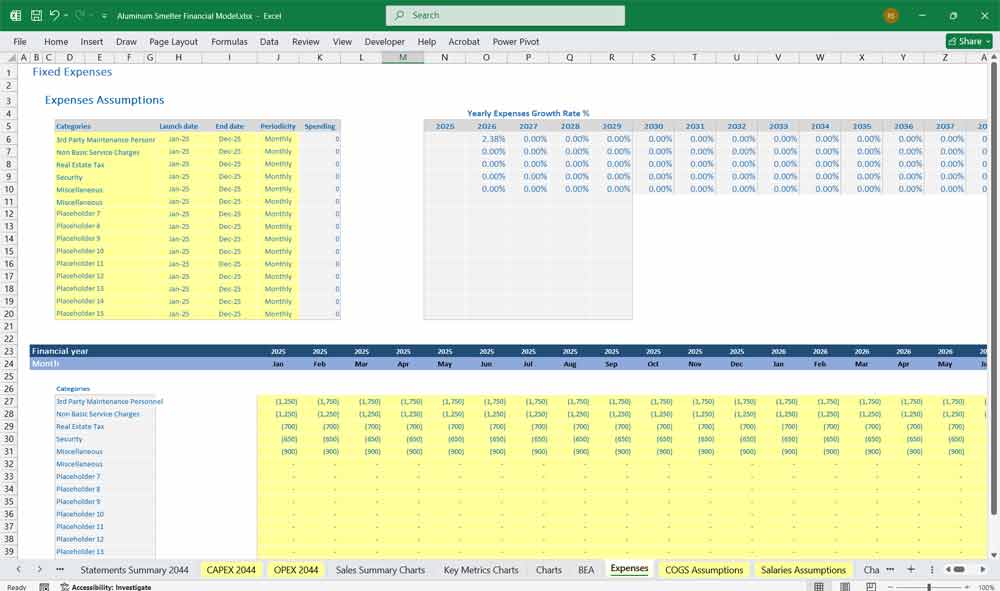

Capital Expenditure (CapEx): Initial investment in infrastructure, hardware, and construction.

- Potline Expansion

- New Casting House and Equipment

- Captive Power Plant Construction

Operational Expenditure (OpEx): Ongoing costs for maintenance, utilities, staffing.

- Personnel Costs

- Maintenance and Repair

- Energy Consumption (Fuel & Electricity)

- Raw Material Procurement

Key Financial Revenue Raises for an Aluminum Smelter

Revenue Metrics

Aluminum Smelter and Aluminum Ingot Sales

Aluminum ingots are the most basic form of cast aluminum produced by an aluminum smelter. These ingots are typically sold to downstream manufacturers for further processing into sheets, wires, or extrusions. Revenue from aluminum ingot sales is directly influenced by global commodity prices and the smelter’s production efficiency. This represents a core revenue stream and serves as the foundation for other value-added product offerings.

Aluminum Smelter Aluminum Slab Sales

Aluminum slabs are semi-finished products produced by the aluminum smelter and primarily used in rolling operations to create aluminum sheets and coils. These slabs command slightly higher margins than ingots due to their added processing value. Revenue from slab sales is driven by demand from automotive, packaging, and construction industries.

Aluminum Billet Sales and your

Aluminum Smelter

Billets are cylindrical cast forms of aluminum produced by the aluminum smelter for extrusion processes. They are typically used in the production of structural profiles, window frames, and heat sinks. Billet sales are a premium segment of the smelter’s revenue, because they cater to specialized downstream customers with quality and size requirements.

Aluminum Smelter Revenues From Aluminum Alloy Sales

Aluminum alloys produced by the aluminum smelter contain small percentages of other metals (like magnesium, silicon, or copper) to enhance strength, corrosion resistance, or workability. These are sold to specialized industries such as aerospace, automotive, and defense. Alloy sales bring in higher per-tonne revenue due to custom formulations and added processing complexity.

Aluminum Smelter Revenues From Low-Carbon Aluminum Sales

Low-carbon aluminum is produced using renewable energy sources or process improvements that significantly reduce greenhouse gas emissions. The aluminum smelter can market this product at a premium, especially to customers in Europe, North America, and Japan where sustainability and carbon reporting are critical. This revenue stream is increasingly important as ESG-driven demand grows globally.

Anode By-product Sales from your

Aluminum Smelter

During the electrolysis process, carbon anodes are consumed and generate by-products such as tar, pitch, and aluminum dross. The aluminum smelter can sell these by-products to industries such as cement, chemicals, or recycling, generating a secondary revenue stream. While modest in size, it improves resource utilization and adds to operational efficiency.

Aluminum Smelter And Power Grid Service Grants

Aluminum smelters often consume large amounts of electricity and can enter agreements with power grid operators to provide demand response or load balancing. In return, the smelter may receive power grid service grants or subsidies. This revenue stream helps offset electricity costs and supports the smelter’s role in grid stability, especially in regions with renewable energy variability.

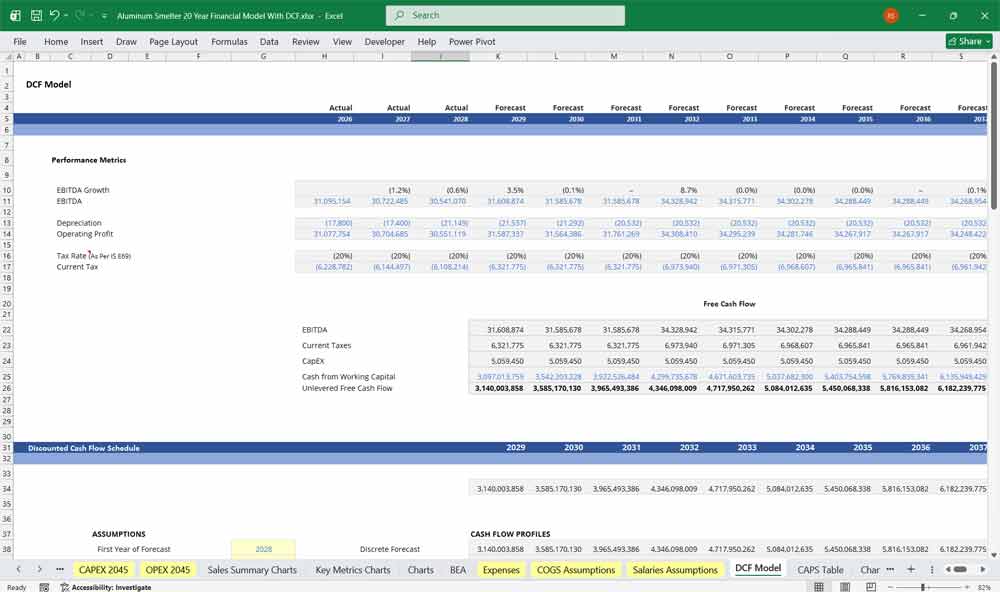

Aluminum Smelter Discounted Cash Flow (DCF) with Terminal Value, Sensitivity Analysis, and Weighted Average Cost of Capital (WACC) Add-On

DCF: Valuing Energy-Intensive Industrial Life Cycles

In an Aluminum Smelter, the Discounted Cash Flow (DCF) analysis must account for the heavy capital intensity of “potlining” cycles and long-term energy contracts. Unlike midstream assets with steady fees, a smelter’s cash flow is highly cyclical, driven by the spread between LME aluminum prices and input costs like alumina and electricity. The 20-year DCF models the timing of major relining projects—which require significant periodic CapEx—against projected global demand for lightweight materials in the EV and aerospace sectors, ensuring the net present value accounts for these massive reinvestment humps.

WACC: Pricing Commodity Volatility and Carbon Risk

The Weighted Average Cost of Capital (WACC) for an aluminum smelter often carries a higher risk premium due to the industry’s exposure to global commodity cycles and high operational leverage. Because smelting is one of the most electricity-intensive industrial processes, the discount rate must incorporate the “carbon risk” associated with the facility’s energy source. A smelter powered by coal will likely face a higher cost of capital and more stringent lending terms than a “green” smelter powered by hydropower, as investors bake the potential for future carbon taxes or stranded asset risks directly into the WACC.

Sensitivity Analysis: Stress-Testing Power Prices and Premiums

For an aluminum smelter, Sensitivity Analysis is the primary tool for navigating “margin squeeze” scenarios. Since power can account for nearly a third of production costs, analysts use sensitivity tables to see how a $10/MWh increase in electricity or a drop in regional “product premiums” impacts the break-even point. By stress-testing the model against fluctuating LME prices and alumina-to-aluminum ratios, the analysis reveals the facility’s resilience to global oversupply. This is critical for determining if the smelter can remain “cash-positive” during the inevitable troughs of the 20-year commodity cycle.

Final Notes on the Financial Model

This 20 Year Aluminum Smelter Financial Model must focus on balancing capital expenditures with steady revenue growth from reliable revenue services. By optimizing operational costs, and power efficiency, and maximizing high-margin services like ingot sales, this model ensures sustainable profitability and cash flow stability.

Download Link On Next Page

Download Link On Next Page