Titanium Plant Financial Model

20-Year Financial Model for a Titanium Plant

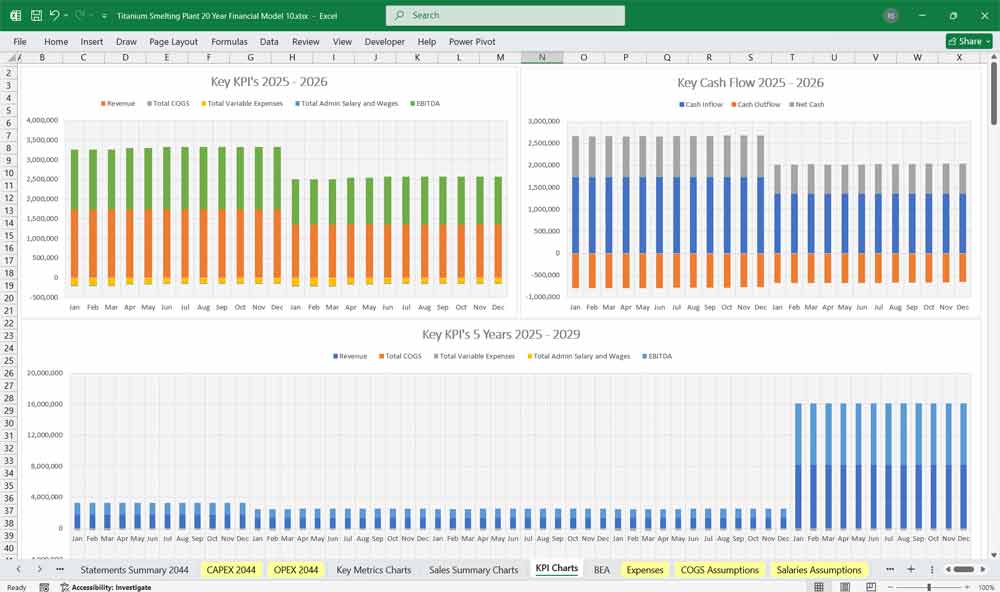

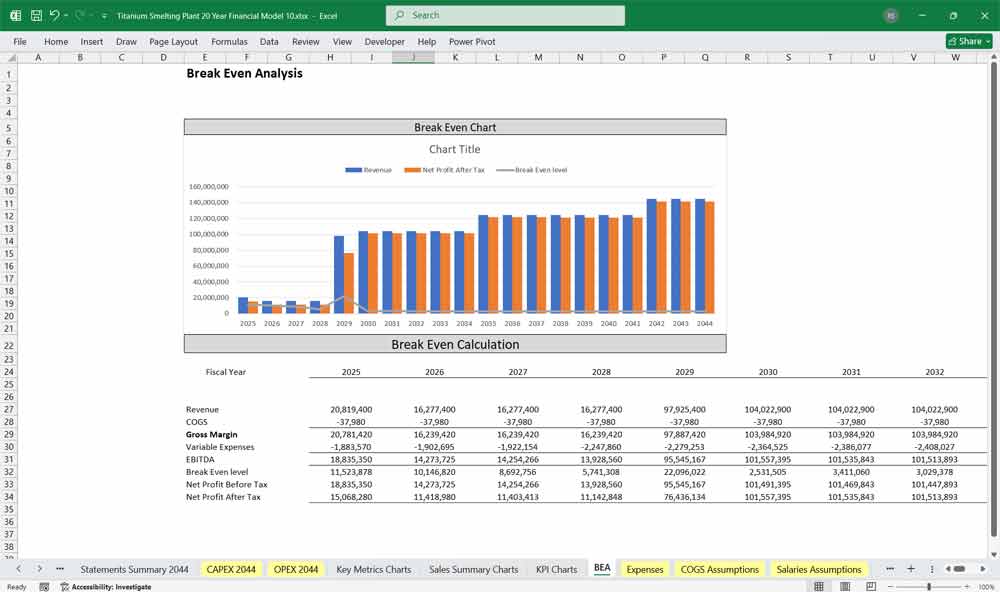

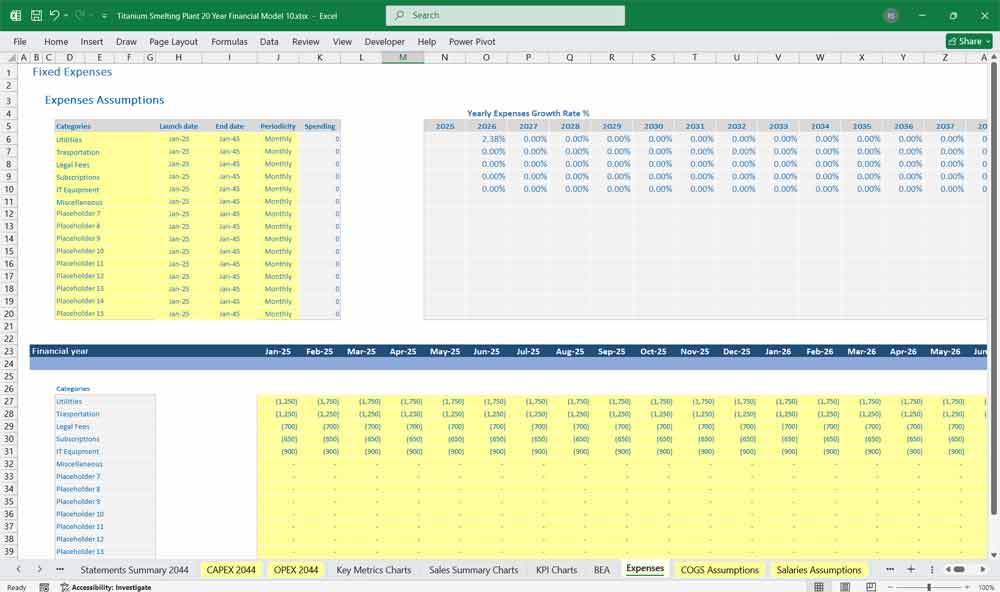

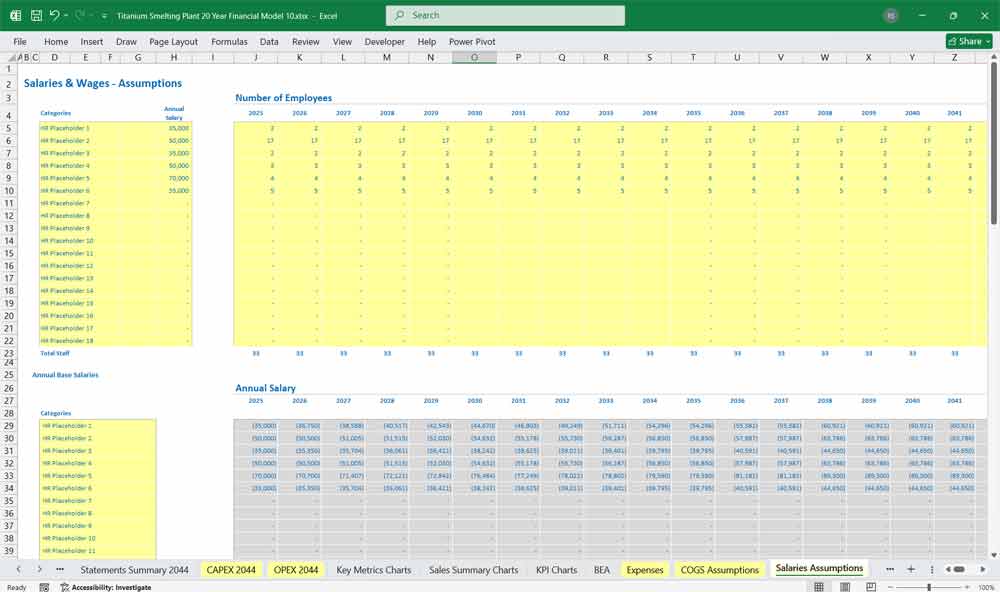

This very extensive 20 Year Titanium Plant Model involves detailed revenue projections, cost structures, capital expenditures, and financing needs. This model provides a thorough understanding of the financial viability, profitability, and cash flow position of your plant. Includes: 20x Income Statements, Cash Flow Statements, Balance Sheets, CAPEX sheets, OPEX Sheets, Statement Summary Sheets, and Revenue Forecasting Charts with the revenue streams, BEA charts, sales summary charts, employee salary tabs and expenses sheets. Over 130 Spreadsheets in 1 Excel Workbook.

Executive Summary of the Financial Model

This financial model projects the economic performance of a titanium production facility. The plant’s operations span from the production of raw Titanium Sponge to various finished and semi-finished products like ingots, alloys, and mill products (plates, sheets, rods). The model is built on a monthly basis for detailed working capital and construction tracking, and transitions over a 20-year period.

Key Drivers:

Production Volume: Ramped up over the first 2-3 years to nameplate capacity.

Pricing: Based on market rates for each product, often with a grade-based premium (e.g., Aerospace Grade vs. Commercial Grade).

Input Costs: Primarily Titanium Tetrachloride (TiCl4), Magnesium, and electricity, which are highly volatile.

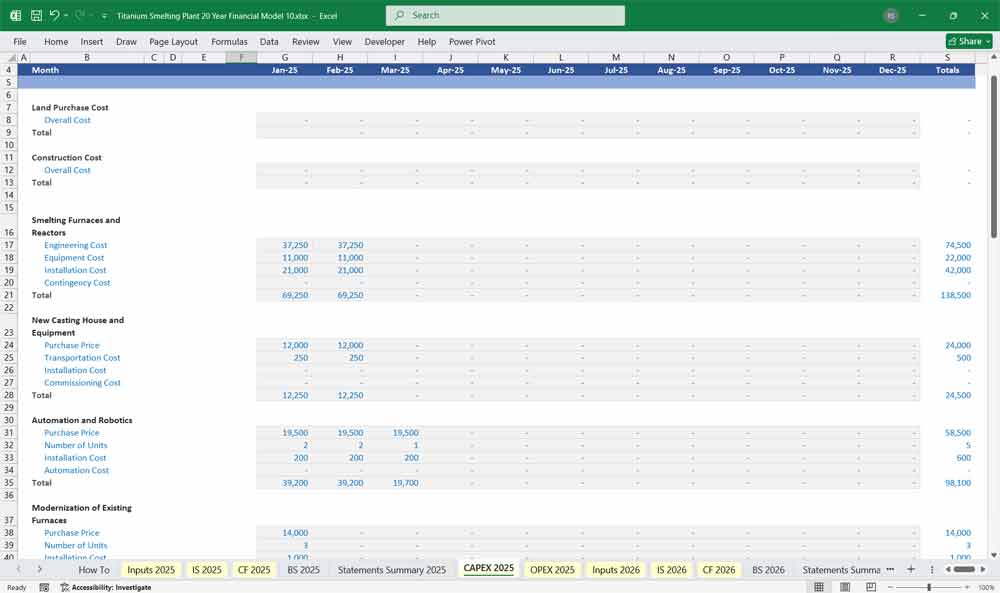

Capital Expenditure (CapEx): Significant initial investment for specialized, corrosion-resistant equipment.

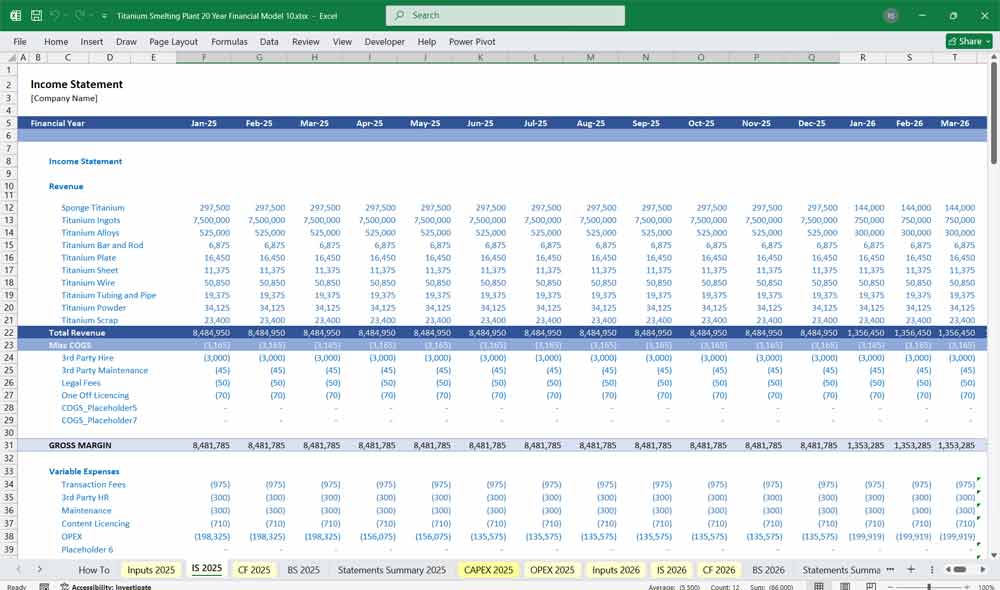

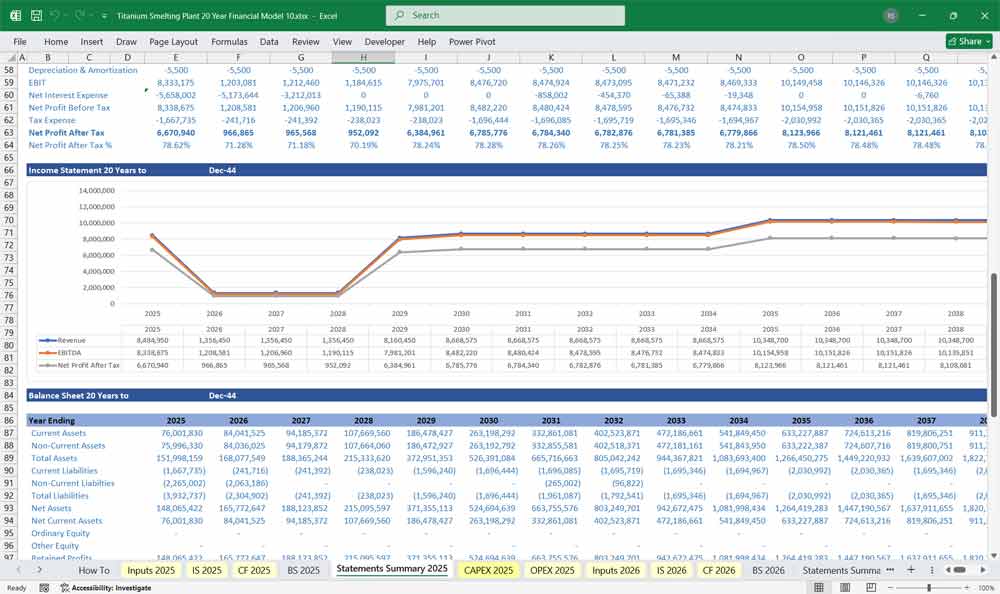

Income Statement

The Income Statement shows the company’s profitability over a specific period.

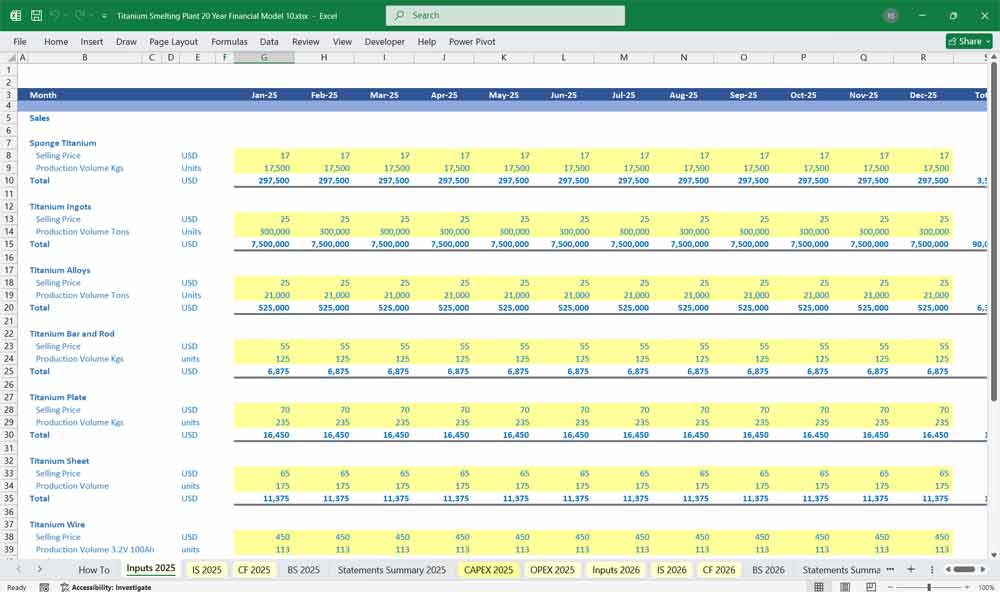

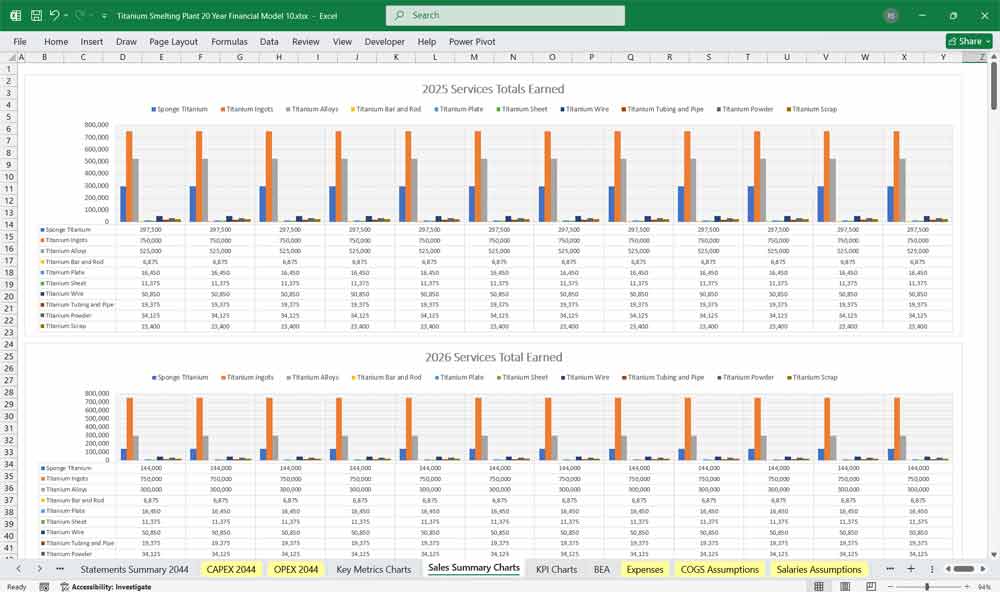

A. Revenue

This is broken down by product stream. Volume is in metric tons (MT) or kilograms (for powder), and price is per unit. 10 editable revenue streams, here are some examples.

Titanium Sponge: The primary raw form of titanium.

Assumptions: Volume (MT), Price ($/kg or $/MT). Often sold to other processors if not fully consumed internally.

Titanium Ingots: Sponge is melted (often via Vacuum Arc Remelting – VAR) to form ingots.

Assumptions: Volume (MT), Price ($/kg). Price includes a premium over sponge for the melting process.

Titanium Alloys: Ingots of specific chemistries (e.g., Ti-6Al-4V).

Assumptions: Volume (MT), Price ($/kg). Significant premium for high-performance alloys. Alloying elements (Vanadium, Aluminum) are a major cost.

Mill Products:

Plates & Sheets: Rolled from slabs.

Assumptions: Volume (MT), Price ($/kg). Price is highly dependent on thickness and surface finish.

Rods & Bars: Extruded or rolled.

Assumptions: Volume (MT), Price ($/kg).

Titanium Powder: For Additive Manufacturing (3D Printing).

Assumptions: Volume (kg), Price ($/kg). This is the highest value-added product, sold at a significant premium.

B. Cost of Goods Sold (COGS)

This is calculated to determine Gross Profit.

1. Direct Raw Materials:

Titanium Tetrachloride (TiCl4) – The main feedstock.

Magnesium (Mg) – A reducing agent in the Kroll process (some is recycled).

Alloying Elements – e.g., Vanadium, Aluminum, Tin.

2. Direct Labor: Plant operators, technicians, and metallurgists.

3. Manufacturing Overheads:

Utilities: Massive electricity consumption for furnaces (melting, sintering) and electrolysis (MgCl2 splitting). Natural gas for heating.

Consumables: Crucibles, electrodes, rolling mill rolls, inert gases (Argon).

Maintenance & Repairs: High-maintenance environment due to corrosive materials.

Depreciation & Amortization: Of production-related assets (buildings, machinery). This is a non-cash expense but critical for the model.

Gross Profit = Total Revenue – COGS

Gross Margin % = (Gross Profit / Revenue) * 100

C. Operating Expenses (OpEx)

These are non-production costs.

Research & Development (R&D): Crucial for developing new alloys and optimizing processes.

Sales, General & Administrative (SG&A): Salaries for management, sales team, marketing, office expenses, etc.

Marketing & Distribution: Freight, shipping, and logistics costs.

Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) = Gross Profit – Operating Expenses (excluding D&A)

Earnings Before Interest and Taxes (EBIT) = EBITDA – D&A

D. Other Income/Expenses

Interest Expense: On debt used to finance the project.

Interest Income: From cash reserves.

Profit Before Tax (PBT) = EBIT + Other Income – Interest Expense

Tax Expense: Calculated on PBT at the applicable corporate tax rate.

Net Income = PBT – Tax Expense

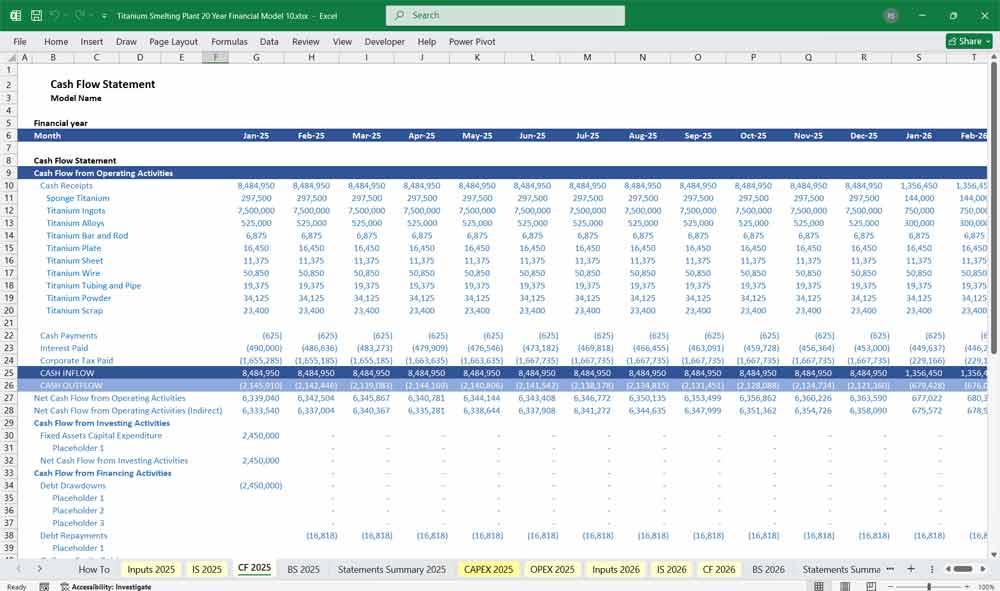

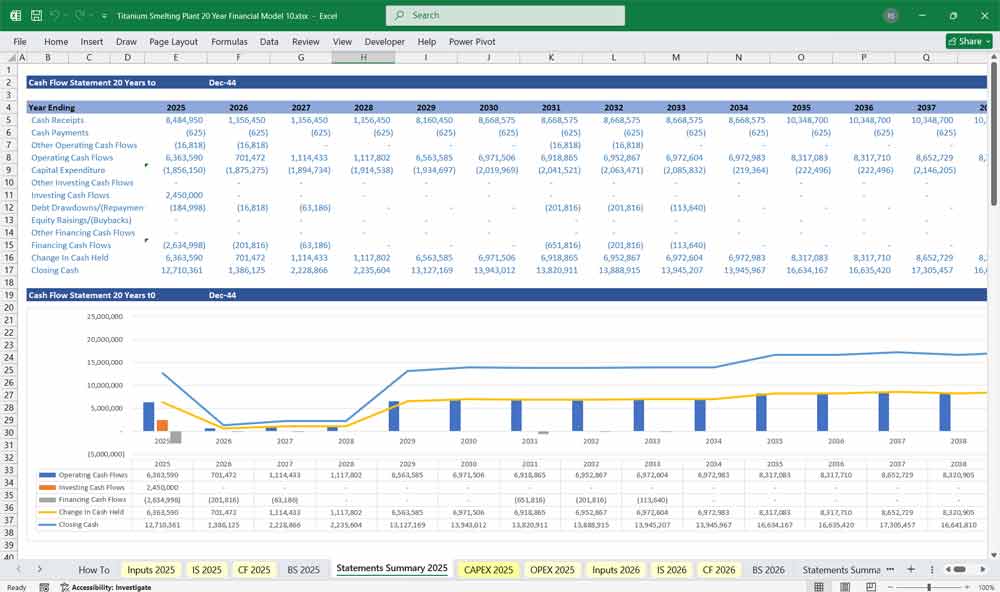

Titanium Plant Cash Flow Statement

The Cash Flow Statement tracks the actual movement of cash, separated into three activities.

A. Cash Flow from Operating Activities (CFO)

This starts with Net Income and adjusts for non-cash items and changes in working capital.

Start with: Net Income

Add Back: Depreciation & Amortization (non-cash)

Adjust for Changes in Working Capital:

Increase in Accounts Receivable: (Cash Outflow) – Customers owe you more.

Increase in Inventory: (Cash Outflow) – You’ve produced/bought more raw materials, WIP, and finished goods.

Increase in Accounts Payable: (Cash Inflow) – You owe your suppliers more, so you’ve held onto cash.

Net Cash from Operating Activities = Net Income + D&A – ΔNWC (where ΔNWC is the net change in working capital items).

B. Cash Flow from Investing Activities (CFI)

This covers the purchase and sale of long-term assets. It is almost always negative in the early years.

Capital Expenditures (CapEx):

Initial CapEx: Land, buildings, Kroll reactors, vacuum arc furnaces (VAR), forging presses, rolling mills, plasma atomizers (for powder), laboratory equipment.

Sustaining CapEx: Ongoing replacements and upgrades to maintain production.

Proceeds from Sale of Assets: (Typically minimal).

Net Cash from Investing Activities = Total CapEx – Proceeds from Asset Sales

C. Cash Flow from Financing Activities (CFF)

This shows the cash flows from and to investors and lenders.

Proceeds from Issuing Debt: Drawdowns from bank loans or bond issuances.

Repayment of Debt Principal: (Cash Outflow).

Proceeds from Issuing Equity: Cash from selling shares.

Payment of Dividends: (Cash Outflow) – Only if the company is profitable and has excess cash.

Net Cash from Financing Activities = Debt Issued + Equity Issued – Debt Repayment – Dividends

Net Change in Cash = CFO + CFI + CFF

Ending Cash Balance = Beginning Cash Balance + Net Change in Cash

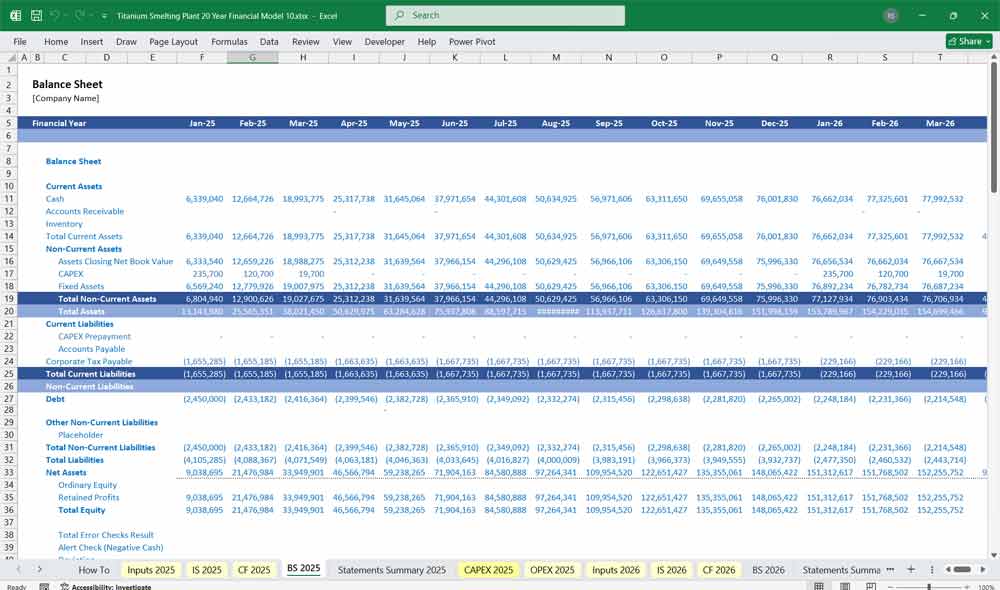

Titanium Plant Balance Sheet

The Balance Sheet is a snapshot of the company’s financial position at a point in time (Assets = Liabilities + Equity).

A. Assets

Current Assets:

Cash & Cash Equivalents: The final figure from the Cash Flow Statement.

Accounts Receivable: Money owed by customers (typically 30-90 days).

Inventory: Raw Materials (TiCl4, Mg), Work-in-Progress (WIP), Finished Goods (Sponge, Ingots, Plates).

Prepaid Expenses: Insurance, rent, etc., paid in advance.

Non-Current Assets (Fixed Assets):

Property, Plant & Equipment (PP&E): Gross PP&E (purchase cost) minus Accumulated Depreciation.

Gross PP&E = Prior Period Gross PP&E + Current Period CapEx

Net PP&E = Gross PP&E – Accumulated Depreciation

Intangible Assets: Patents, licenses.

B. Liabilities

Current Liabilities:

Accounts Payable: Money owed to suppliers (e.g., for TiCl4, electricity).

Accrued Expenses: Wages, utilities, interest that are owed but not yet paid.

Short-Term Debt: The portion of long-term debt due within one year.

Non-Current Liabilities:

Long-Term Debt: The principal amount of loans not due within the year.

C. Shareholders’ Equity

Common Stock & Additional Paid-In Capital: Money raised from issuing shares.

Retained Earnings: Cumulative net income kept in the company (not paid out as dividends).

Retained Earnings (Current) = Retained Earnings (Prior) + Net Income (Current) – Dividends Paid (Current)

Key Titanium Plant Industry-Specific Considerations

High Fixed Cost Base: Equipment-heavy industry with high depreciation.

R&D Intensity: Critical for staying competitive.

Quality & Certification: Failure costs can be catastrophic (scrap, rework).

Cyclicality & Diversification: Aerospace/automotive cycles affect volumes.

20-Year Titanium Plant Financial Model Advantages

This 20-year financial model is crucial for accurately capturing the long-term capital-intensive nature of a titanium plant. The initial phase involves staggering capital expenditure (CapEx) for specialized equipment like Kroll reactors and vacuum arc furnaces, with profitability often remaining elusive for the first several years. A short-term model would only show this period of negative cash flows, potentially dooming the project from the start. A 20-year horizon, however, allows the model to demonstrate how the initial investment is amortized over time, revealing the point at which the plant achieves break-even and begins to generate a substantial return on investment, thus justifying the upfront financial commitment to investors and lenders.

Strategic Planning For Titanium Plant Investments

this extended timeframe is essential for strategic planning and market alignment, as the titanium industry is characterized by long business cycles, especially in its core aerospace and defense sectors. The sales cycle for qualifying as a supplier and securing long-term contracts for aircraft components or military applications can span many years. A 20-year model can incorporate realistic production ramps, reflect the timing of major contract revenues, and plan for subsequent capacity expansions. It allows management to proactively schedule future CapEx waves for equipment upgrades or new product lines, such as titanium powder for additive manufacturing, ensuring the business remains competitive over decades

Titanium Plant Risk Assessment

A long-term an indispensable tool for robust risk assessment and sensitivity analysis. Key variables, such as the volatile prices of raw materials (e.g., titanium sponge) and energy, or shifts in global demand, can be stress-tested over a 20-year period. This long-view analysis helps identify the project’s most critical vulnerabilities and its ability to withstand economic downturns. By modeling different scenarios—such as a recession impacting aerospace demand or a tariff on imported materials—stakeholders can develop contingency plans, secure appropriate financing covenants, and understand the true risk-adjusted potential of the enterprise.

Titanium Plant Stakeholder Confidence

A 20-year financial model supports credible valuation and exit planning. Potential acquirers, such as large metallurgical conglomerates or private equity firms, will demand a clear view of the plant’s long-term cash flow generation to assess its worth. The model provides a foundation for advanced valuation techniques, including Discounted Cash Flow (DCF) analysis, which relies on projecting free cash flows far into the future. By illustrating a compelling financial trajectory over two decades, the model not only helps in attracting initial funding but also in maximizing shareholder value for a future merger, acquisition, or public listing.

Final Notes on the Financial Model

This 20 Year Titanium Plant Financial Model focuses on balancing capital expenditures with steady revenue growth from a diversified titanium plant product line. By optimizing operational costs, and power efficiency, and maximizing high-margin services, the models ensure sustainable profitability and cash flow stability.

Download Link On Next Page