Soda Ash Production Plant Financial Model

Financial Model for a Soda Ash Production Plant

This very extensive 20 Year Soda Ash Production Plant Model involves detailed revenue projections, cost structures, capital expenditures, and financing needs. This model provides a thorough understanding of the financial viability, profitability, and cash flow position of the plant. Including: 20x Income Statements, Cash Flow Statements, Balance Sheets, CAPEX sheets, OPEX Sheets, Statement Summary Sheets, and Revenue Forecasting Charts with the specified revenue streams, BEA charts, sales summary charts, employee salary tabs and expenses sheets. Over 100 Spreadsheets in 1 Excel Workbook for the closest monitoring of your Soda Ash Production Plant Financials.

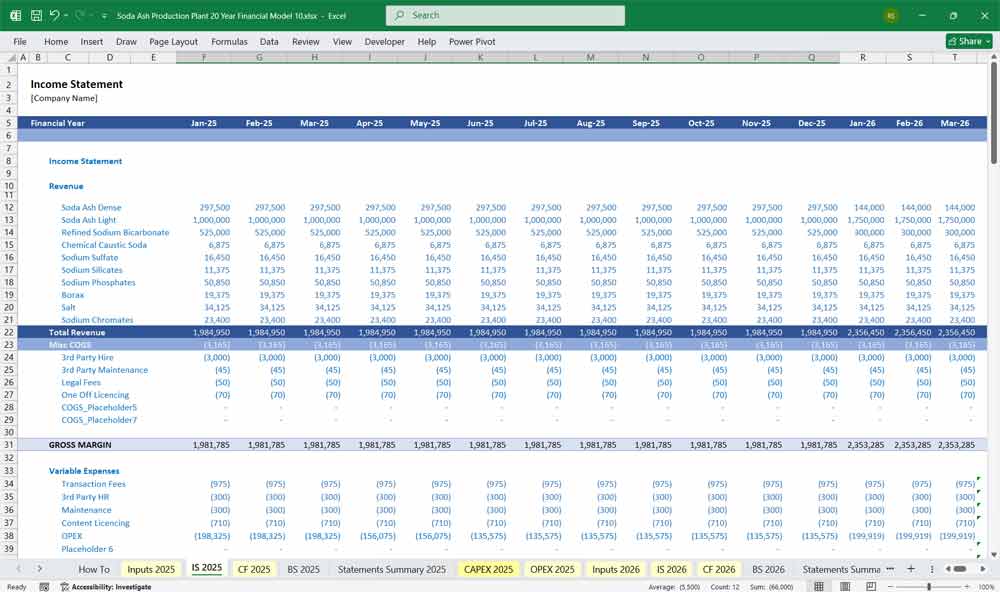

The Income Statement

This statement shows the plant’s profitability over a specific period (e.g., one year).

Revenue:

Calculated as:

Production Volume * Utilization Rate * Sales Pricefor Soda Ash and by-products.

Cost of Goods Sold (COGS):

Variable Costs: Sum of all direct costs (Raw Materials, Utilities, Variable Labor) which scale with production volume.

Gross Profit:

Revenue - COGS.Gross Margin:

(Gross Profit / Revenue) * 100.

Operating Expenses (OPEX):

Sum of Fixed Labor, SG&A, and other fixed costs.

Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA):

Gross Profit - OPEX. This is a key metric for operational performance, excluding financing and accounting decisions.

Depreciation & Amortization (D&A):

A non-cash expense calculated based on the CAPEX schedule and the depreciation method.

Earnings Before Interest and Taxes (EBIT) / Operating Profit:

EBITDA - D&A.

Interest Expense:

Calculated based on the outstanding debt balance from the Balance Sheet and the assumed interest rate.

Earnings Before Tax (EBT):

EBIT - Interest Expense.

Tax Expense:

EBT * Tax Rate. This is adjusted for any tax shields or loss carry-forwards.

Net Income:

EBT - Tax Expense. This is the final “bottom-line” profit attributable to the owners.

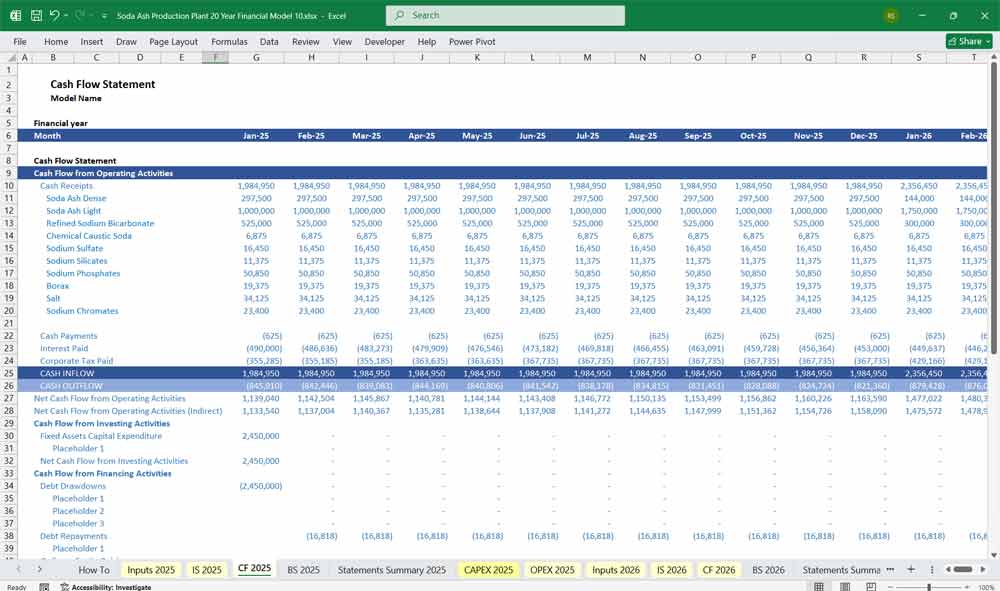

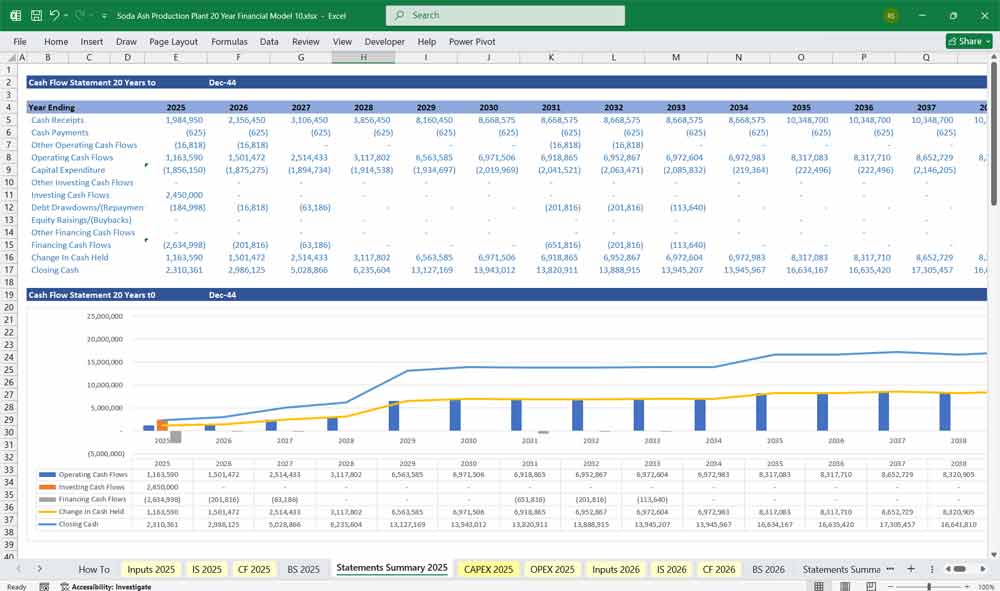

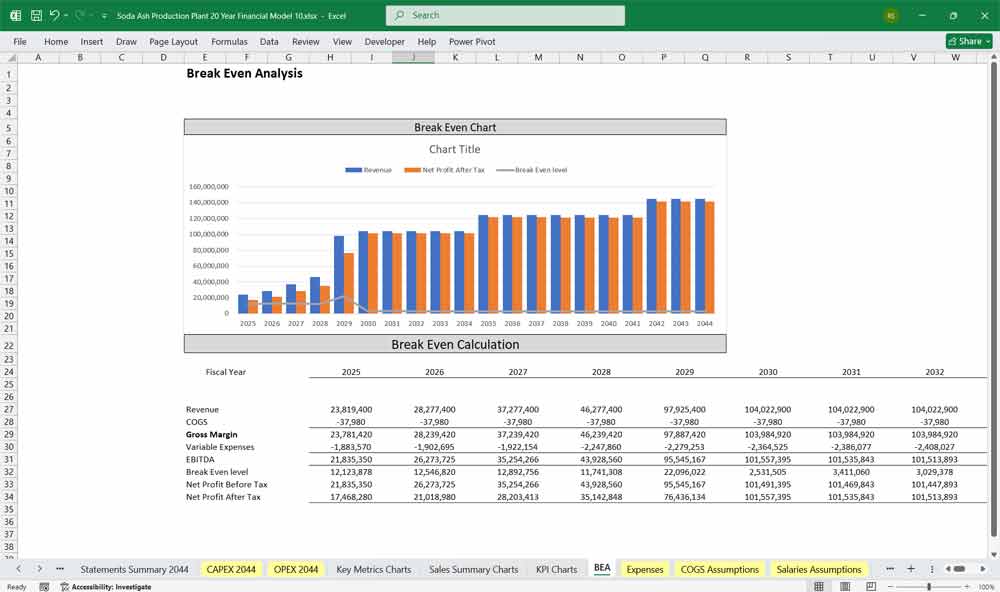

Soda Ash Production Plant Cash Flow Statement

This statement tracks the actual movement of cash, broken down into three activities.

Cash Flow from Operating Activities (CFO):

Starts with Net Income.

Add back non-cash expenses like Depreciation & Amortization.

Adjust for changes in Working Capital (calculated using DSO, DIO, DPO):

Increase in Accounts Receivable (use of cash).

Increase in Inventory (use of cash).

Increase in Accounts Payable (source of cash).

This gives the net cash generated from core business operations.

Cash Flow from Investing Activities (CFI):

This is almost always a negative number (cash outflow) for a capital-intensive project.

It consists of Total Capital Expenditures (Initial + Sustaining), as per the CAPEX schedule.

Cash Flow from Financing Activities (CFF):

Inflows: Proceeds from issuing Debt and Equity.

Outflows: Repayment of Debt principal (scheduled amortization) and payment of Dividends (if any).

Net Change in Cash:

CFO + CFI + CFF.

Closing Cash Balance:

Opening Cash Balance + Net Change in Cash. This closing balance links directly to the Balance Sheet.

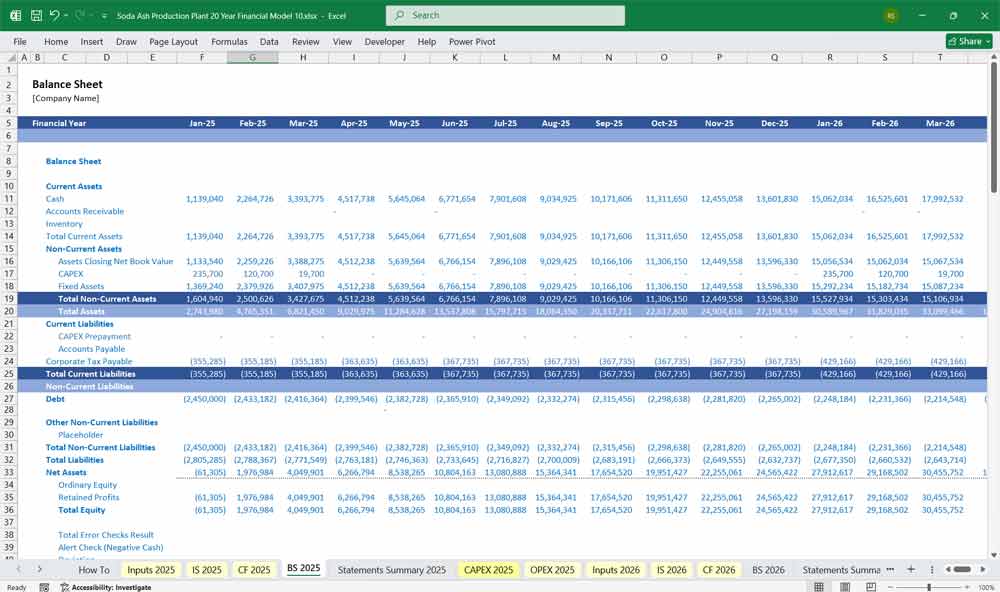

Soda Ash Production Plant Balance Sheet

This is a snapshot of the company’s financial position at a specific point in time (end of the year).

Assets:

Current Assets: Cash & Equivalents (from the Cash Flow Statement), Accounts Receivable, Inventory.

Non-Current Assets:

Property, Plant & Equipment (PP&E): Calculated as

Prior Year PP&E + Capital Expenditures - Depreciation.Other Fixed Assets (e.g., Land).

Liabilities:

Current Liabilities: Accounts Payable, Short-Term Debt (the portion of long-term debt due within the year).

Non-Current Liabilities: Long-Term Debt (the outstanding principal, calculated as

Prior Year Debt + New Drawdowns - Principal Repayments).

Equity:

Paid-In Capital: The initial and any subsequent equity investments.

Retained Earnings: Calculated as

Prior Year Retained Earnings + Current Year Net Income - Dividends Paid.

The Accounting Equation must always hold:

Total Assets = Total Liabilities + Shareholders’ Equity.

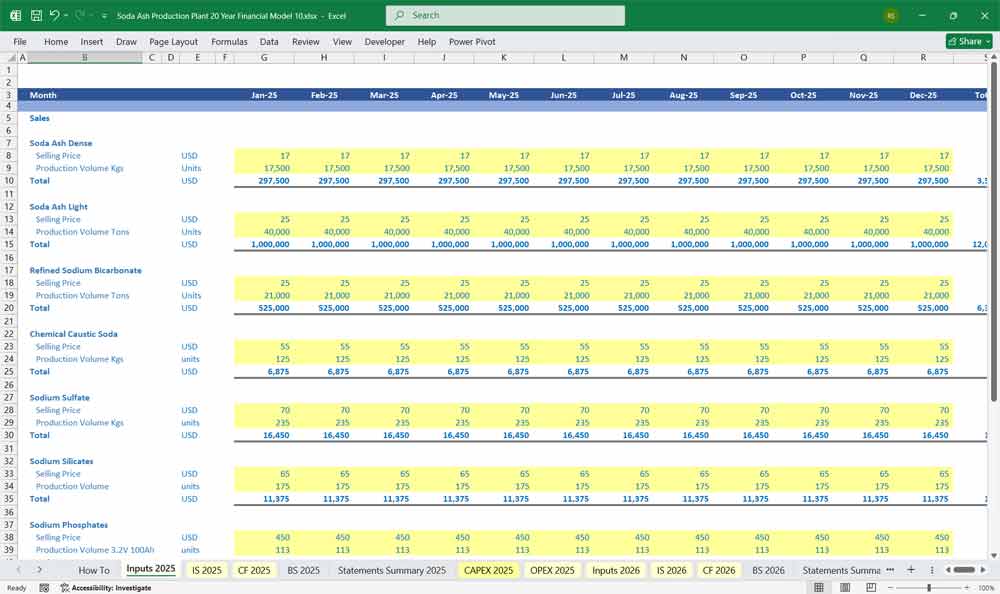

Key Assumptions & Drivers For A Soda Ash Production Plant

This is the “engine room” of the model. All other sections draw their data from here.

Production & Capacity:

Nameplate Capacity: Total theoretical annual production (e.g., 500,000 metric tons).

Ramp-Up Period: A schedule showing how production increases from 0% to a stable percentage (e.g., 90-95%) over the first few years.

Plant Availability: Accounts for planned and unplanned shutdowns.

Revenue:

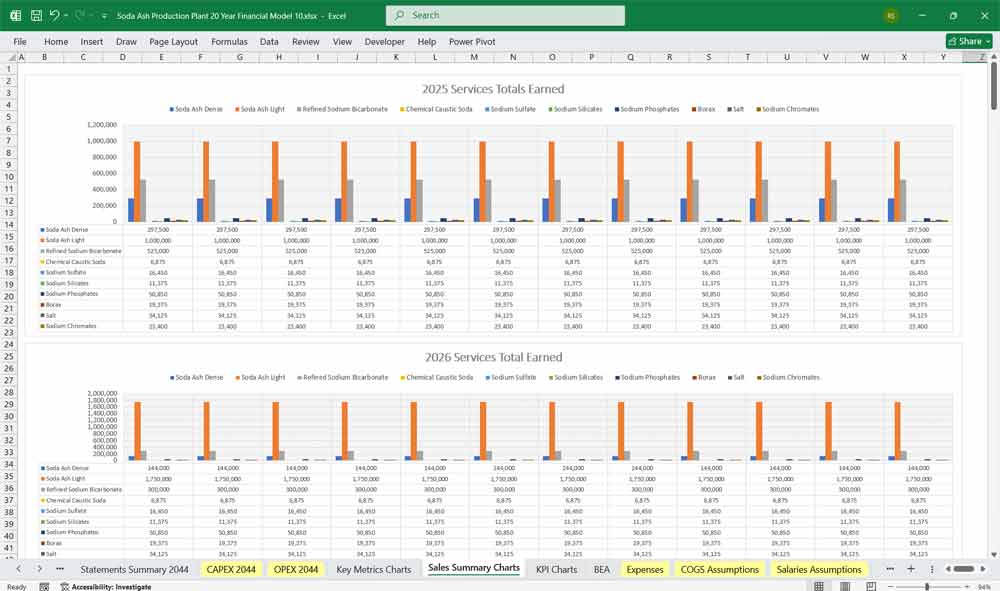

Soda Ash Sales Price: Can be broken down by market and product grade (dense vs. light). This can be a key variable for sensitivity analysis.

By-Product Sales: Revenue from Calcium Chloride or Ammonium Chloride, including volume and price assumptions.

Direct Costs (Cost of Goods Sold – COGS):

Raw Materials: Consumption rates and prices for key inputs: Salt (Brine), Limestone, Ammonia (as a makeup cost, since most is recycled), and Energy (Coke, Natural Gas).

Utilities: Cost of power (purchased electricity), process water, and other utilities.

Variable Labor: Operating staff directly involved in production.

Consumables & Maintenance Materials.

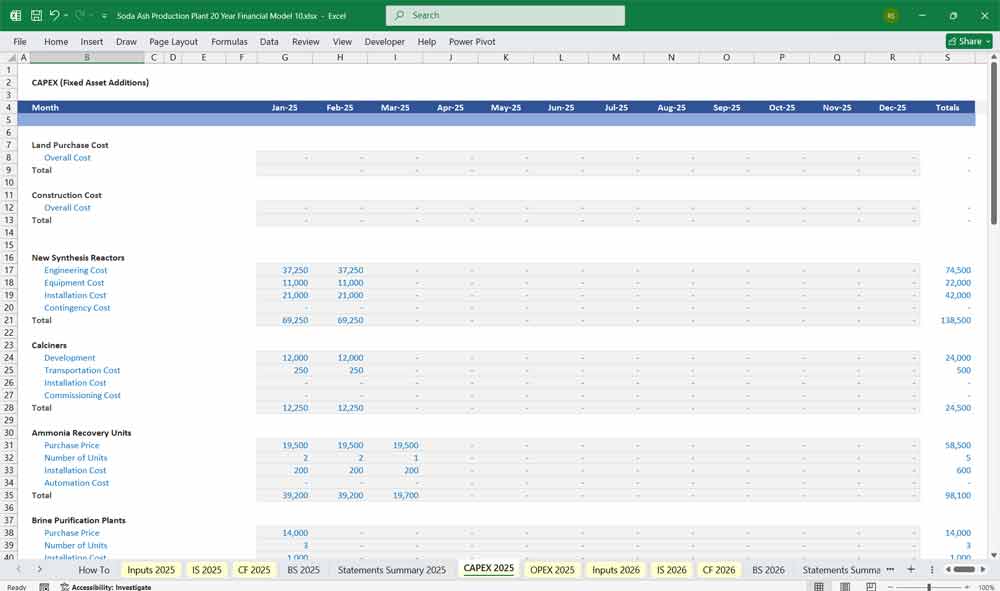

Capital Expenditure (CAPEX) Schedule:

Initial CAPEX (Pre-Production): The total investment required to build the plant before operations begin. This is broken down into categories like Land, Process Units, Utilities, Engineering & Construction, and Contingency.

Phasing of Initial CAPEX: A detailed annual or quarterly schedule of how the initial CAPEX will be spent during the construction period.

Sustaining CAPEX: Annual capital expenditures required to maintain the plant’s operational capacity (e.g., 2-4% of initial CAPEX per year).

Expansion/Replacement CAPEX: Major investments in future years for debottlenecking or equipment replacement.

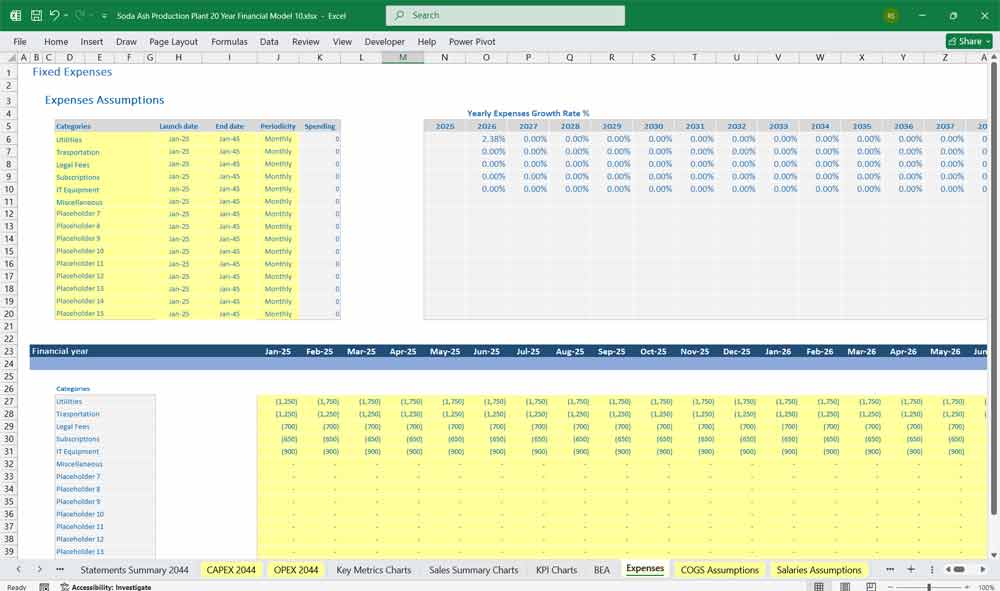

Operating Expenses (OPEX):

Fixed Labor: Salaries for management, administration, and fixed operating staff.

Maintenance Contracts & Repairs.

Selling, General & Administrative (SG&A): Salaries for sales and admin staff, marketing, insurance, office expenses.

Royalties & Licensing Fees (e.g., for the Solvay process technology).

Working Capital Assumptions:

Days Inventory Outstanding (DIO): Log raw materials and finished goods held in inventory.

Days Payable Outstanding (DPO): Log the time it takes a company to pay.

Financing & Tax:

Debt Financing: Total debt amount, interest rate, term, and grace period.

Equity Financing: Amount of equity invested by shareholders.

Depreciation Schedule: The method (e.g., Straight-Line) and useful life for different asset classes (Plant & Machinery, Buildings, etc.).

Tax Rate: The applicable corporate income tax rate. Includes assumptions on tax-loss carry-forwards.

Integration and Key Outputs

The model is integrated, meaning a change in an assumption automatically flows through all three statements. For example, a higher sales price increases Revenue (Income Statement), which increases Net Income and thus CFO (Cash Flow), which boosts Retained Earnings and the Closing Cash Balance (Balance Sheet).

The final outputs and analyses derived from this model include:

Projected Financial Statements for the entire forecast period.

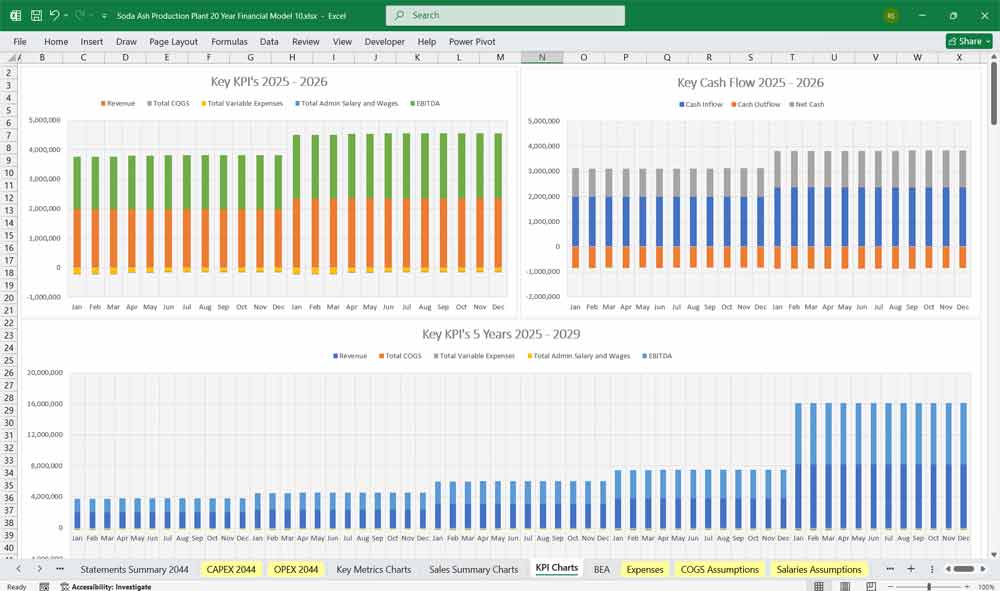

Key Performance Indicators (KPIs):

Net Present Value (NPV) of the project.

Internal Rate of Return (IRR).

Payback Period (how long to recover the initial investment).

Debt Service Coverage Ratio (DSCR) (ability to service debt).

Loan Life Coverage Ratio (LLCR).

Sensitivity Analysis: How NPV and IRR change with variations in key assumptions like Soda Ash price, raw material costs, or CAPEX overruns.

Scenario Analysis: Comparing a “Base Case” with a “Downside Case” and an “Upside Case.”

Final Notes on the Financial Model

This 20 Year Soda Ash Production Plant Financial Model must focus on balancing capital expenditures with steady revenue growth from diversified subscription-based services. By optimizing operational costs and power efficiency and maximizing high-margin services like Soda Ash Dense, and Light Sales, and Refined Sodium Bicarbonate producton, this model ensures sustainable profitability and cash flow stability.

Download Link On Next Page