Garden Machinery Financial Model

20 Year Financial Model for a Garden Machinery Manufacturer

This very extensive 20 Year Garden Machinery Model involves detailed revenue projections, cost structures, capital expenditures, and financing requirements. This model provides a thorough understanding of the financial viability, profitability, and cash flow position of the machinery business. Including: 20x Income and Cash Flow Statements, Balance Sheets, CAPEX and OPEX Spreadsheets, Statement Summary Sheets, and Revenue Forecasting Charts with the specified revenue streams, BEA charts, sales summary charts, employee salary tabs and expenses sheets. Over 120 Spreadsheets of financial data to monitor.

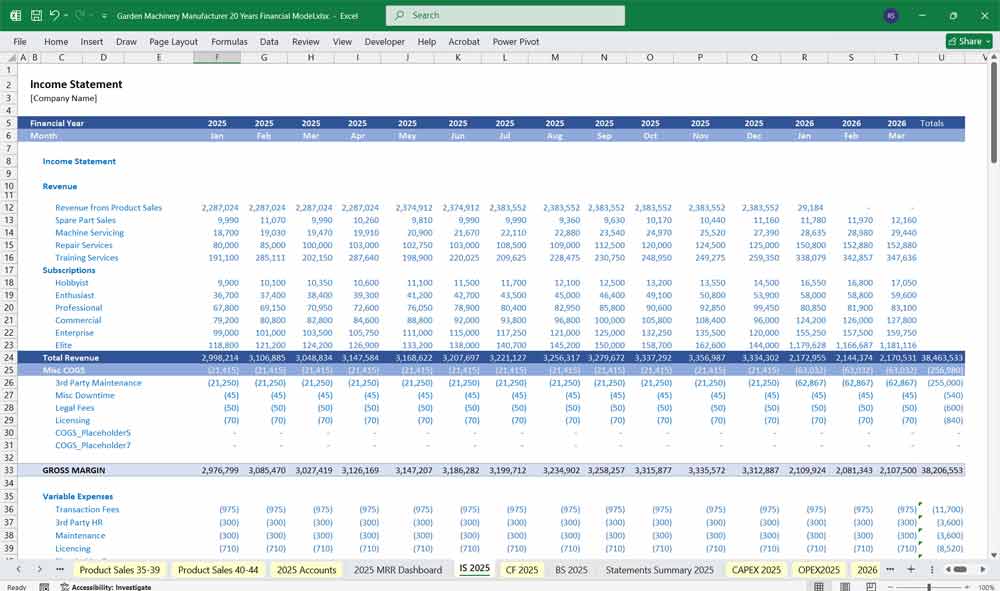

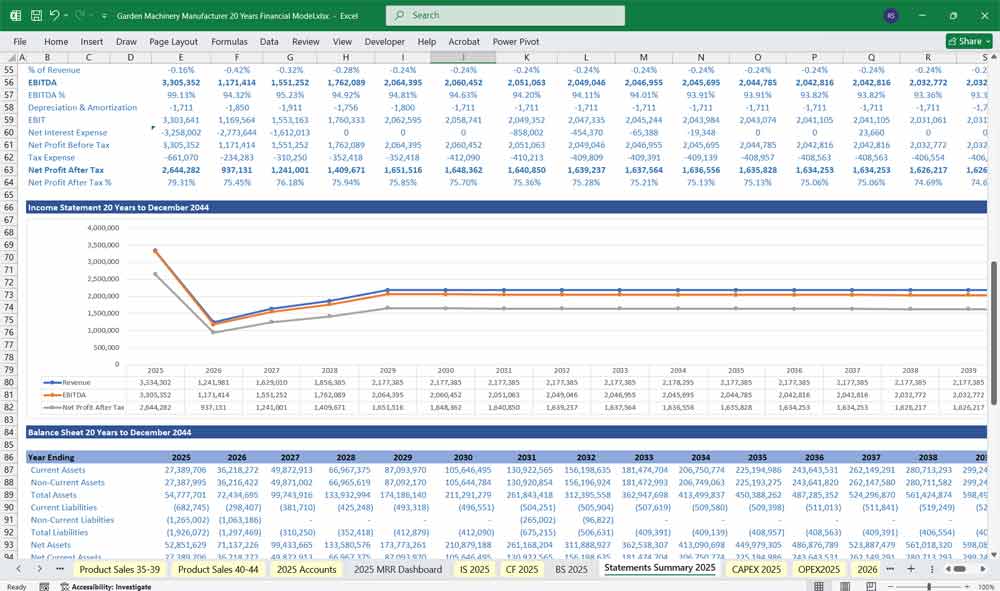

Income Statement (Profit & Loss – P&L)

This statement shows profitability over a period (e.g., quarterly or annually).

A. Revenue (Top Line):

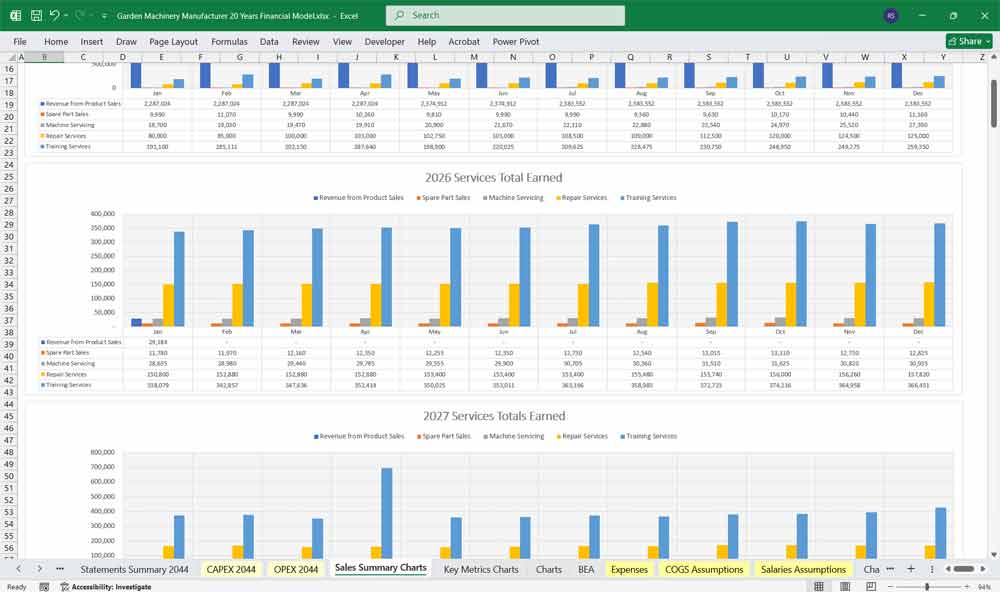

Sales of Equipment: (Units of Product A * Price A) + (Units of Product B * Price B) + …

Sales of Parts & Attachments: A crucial recurring revenue stream.

Service & Warranty Income: Revenue from repair services and extended warranty programs.

Total Revenue = Sum of all revenue streams.

B. Cost of Goods Sold (COGS):

Raw Material Cost: Linked directly to the BOM assumptions and sales volume.

Direct Labor Cost: Linked to production volume and labor assumptions.

Manufacturing Overhead: Allocated fixed costs of running the production facility.

Depreciation of Manufacturing Equipment: Calculated from the CapEx schedule.

Total COGS = Sum of the above.

Gross Profit = Total Revenue – Total COGS.

Gross Margin % = (Gross Profit / Total Revenue) * 100. A key health metric.

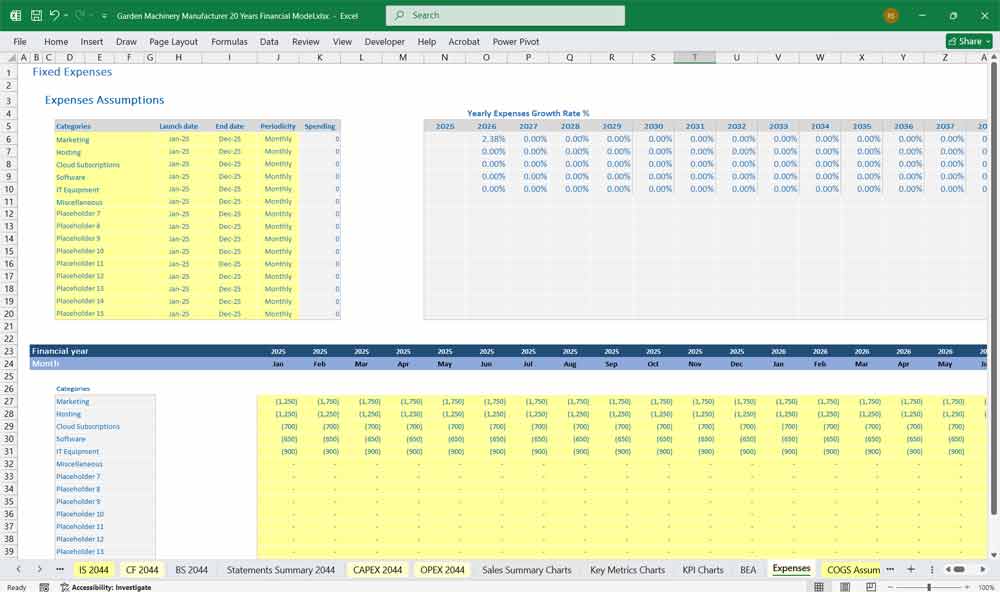

C. Operating Expenses (OPEX):

Research & Development (R&D): Salaries for engineers, prototyping costs.

Sales & Marketing (S&M): Advertising budgets, sales team salaries and commissions, trade show costs.

General & Administrative (G&A): Executive salaries, finance/HR/legal costs, office rent, utilities.

Depreciation (non-manufacturing): For office equipment, etc.

Total Operating Expenses = R&D + S&M + G&A.

Operating Income (EBIT) = Gross Profit – Total Operating Expenses.

EBIT = Earnings Before Interest and Taxes.

D. Other Income/Expenses:

Interest Expense: On outstanding debt balances (linked to the Balance Sheet and debt schedule).

Interest Income: From cash reserves.

Pre-Tax Income = EBIT – Interest Expense + Interest Income.

E. Taxes and Net Income:

Income Tax Expense: Pre-Tax Income * Corporate Tax Rate.

Net Income = Pre-Tax Income – Income Tax Expense.

This is the famous “Bottom Line.”

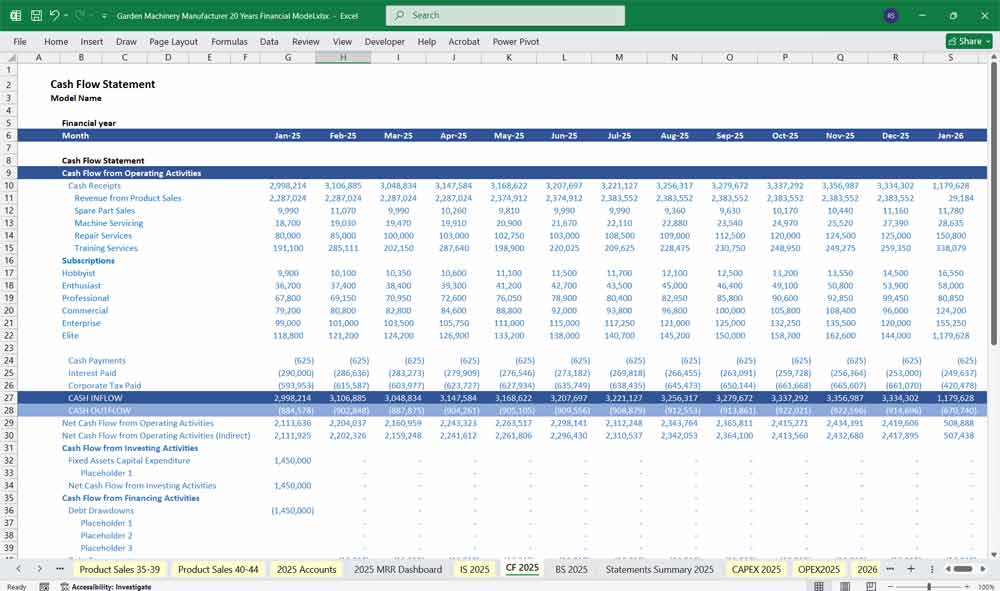

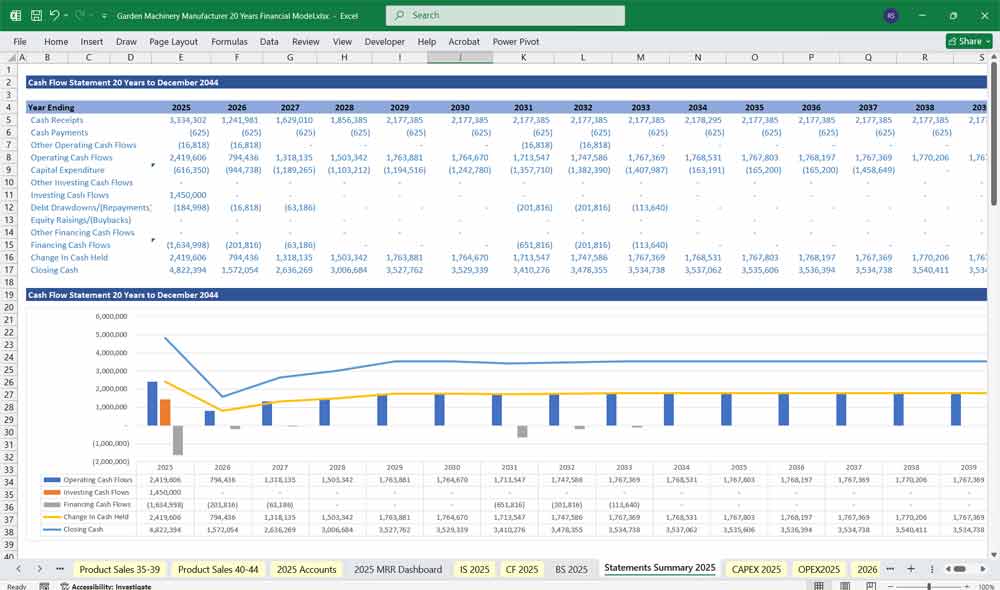

Garden Machinery Cash Flow Statement

This statement explains the change in cash from the beginning to the end of the period. It is broken into three sections.

Cash Flow from Operating Activities (CFO) – The Core Business

Start with Net Income.

Add back non-cash expenses: Depreciation & Amortization.

Adjust for changes in Working Capital:

Increase in Accounts Receivable is a use of cash (subtract).

Increase in Inventory is a use of cash (subtract). Critical for a manufacturer ramping up production.

Increase in Accounts Payable is a source of cash (add). You’re delaying payment to suppliers.

Net CFO = Net Income + D&A – Change in Working Capital.

Investing in the Business. Cash Flow from Investing Activities (CFI) –

Capital Expenditures (CapEx): Cash spent on new equipment, tooling, etc. (a use of cash, so it’s negative).

Net CFI = – Total CapEx (typically).

Cash Flow from Financing Activities (CFF) – Raising & Repaying Money

Proceeds from Debt: Cash received from taking out new loans (source of cash).

Repayment of Debt Principal: Cash used to pay down loans (use of cash).

Dividends Paid: Cash distributed to shareholders (use of cash).

Issuance of Stock: Cash from investors (source of cash).

CFF Net = Sum of all financing activities.

Net Change in Cash:

Net Change in Cash = Net CFO + Net CFI + Net CFF.

Ending Cash = Beginning Cash + Net Change in Cash.

This Ending Cash figure must match the Cash figure on the Balance Sheet.

Integration and Outputs

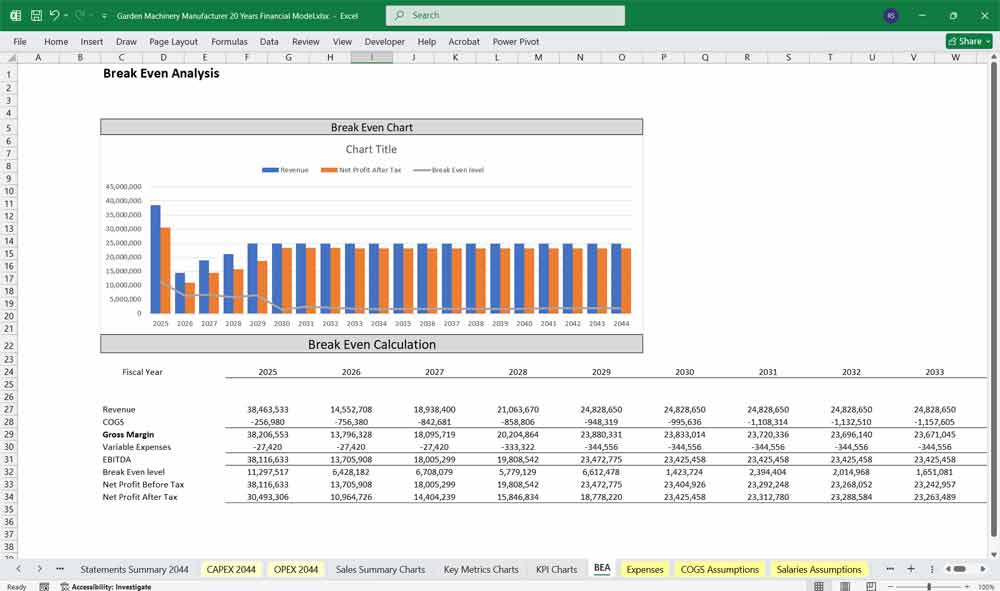

Scenarios: The model should allow for Sensitivity Analysis and scenario planning (e.g., Base Case, Worst Case, Best Case). Key levers to test: sales volume, material costs, interest rates.

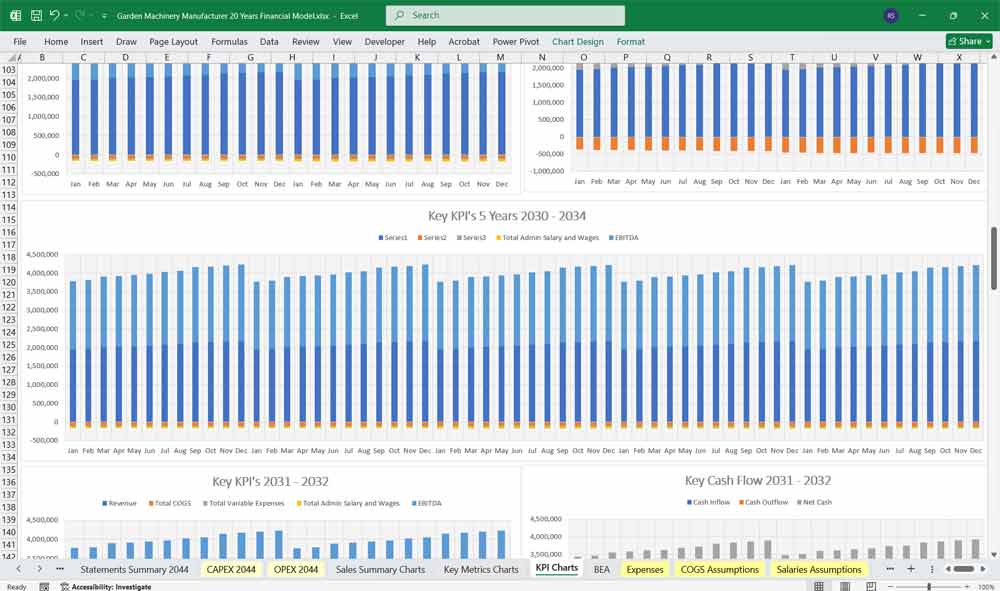

Key Outputs & KPIs:

Revenue Growth Rate: Year-over-Year growth.

EBITDA: Earnings Before Interest, Taxes, Depreciation, and Amortization. A proxy for operational cash flow.

Net Profit Margin: (Net Income / Revenue).

Working Capital Cycle: DSO + DIO – DPO. The number of days cash is tied up.

Leverage Ratios: Debt-to-Equity, Debt-to-EBITDA.

Liquidity Ratios: Current Ratio (Current Assets / Current Liabilities).

Return on Equity (ROE): (Net Income / Shareholders’ Equity).

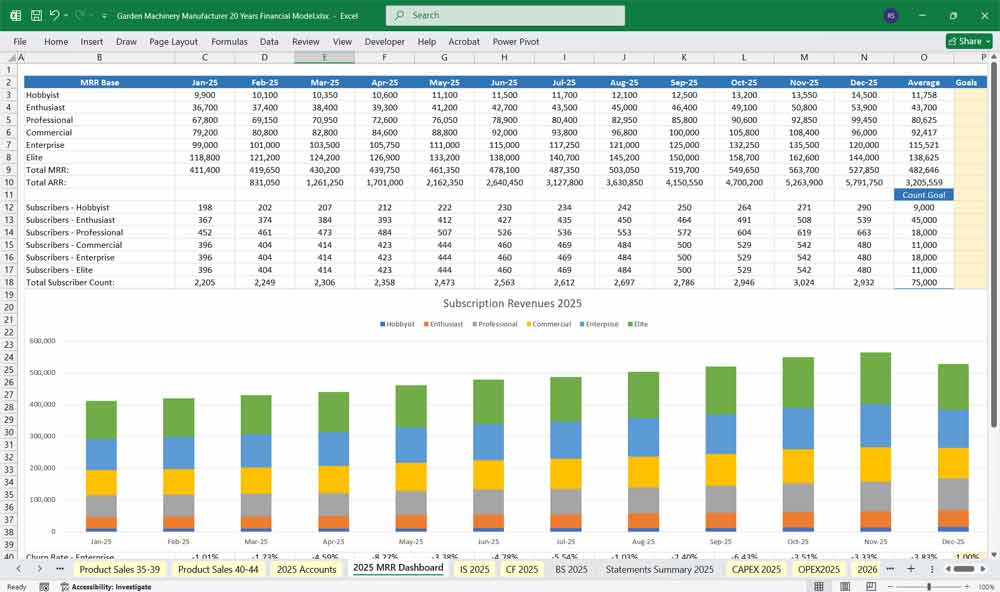

Dashboard: A summary tab with charts and graphs visualizing revenue by product, profitability trends, cash flow, and key ratios is essential for presenting to management and investors.

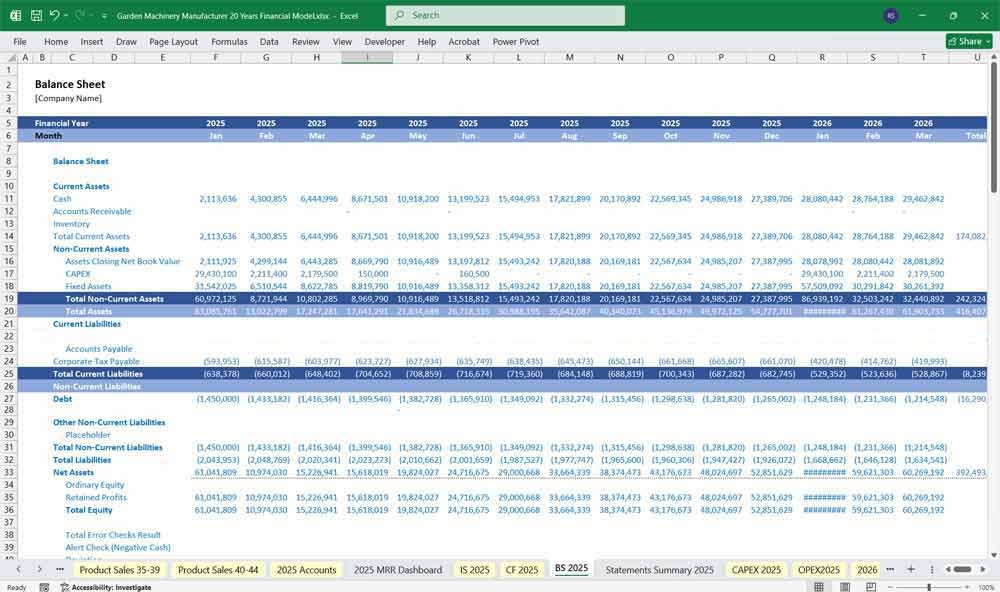

Garden Machinery Balance Sheet

This is a snapshot of the company’s financial position at a specific point in time (e.g., end of Q4). It must balance: Assets = Liabilities + Shareholders’ Equity.

ASSETS (What the Company Owns)

Current Assets:

Cash & Cash Equivalents: The ending cash balance from the Cash Flow Statement. This is the plug figure that makes the Balance Sheet balance.

Accounts Receivable: Calculated using DSO assumption. (Revenue / 365) * DSO.

Inventory: Calculated using DIO assumption. (COGS / 365) * DIO. This is a major asset for a manufacturer.

Prepaid Expenses: e.g., Insurance paid in advance.

Non-Current Assets:

Property, Plant & Equipment (PP&E): Factory, land, manufacturing equipment. Calculated as: Prior Period PP&E + Capital Expenditures – Depreciation.

Intangible Assets: Patents, trademarks (if acquired).

LIABILITIES (What the Company Owes)

Current Liabilities:

Accounts Payable: Money owed to suppliers for raw materials. Calculated using DPO. (COGS / 365) * DPO.

Accrued Expenses: Wages, utilities, taxes owed but not yet paid.

Short-Term Debt: The portion of long-term debt due within the year.

Non-Current Liabilities:

Long-Term Debt: The principal amount of loans outstanding. Calculated in a debt schedule: Prior Period Debt + New Debt – Debt Repayments.

SHAREHOLDERS’ EQUITY (Net Worth)

Common Stock: Par value of invested capital.

Retained Earnings: The cumulative profits kept in the business. Calculated as: Prior Period Retained Earnings + Net Income – Dividends Paid.

Key Financial Model Drivers & Assumptions.

Market & Sales:

Market Growth Rate: Expected annual growth of the overall market.

Market Share: Company’s projected share of the market.

Product Portfolio: List of key products (e.g., Lawn Mowers (ride-on, push), Tractors, Trimmers, Blowers, Tillers).

Pricing Strategy: Average Selling Price (ASP) per product, with assumptions for annual price increases.

Sales Volume: Units forecasted to be sold per product per month/quarter.

Sales Seasonality: Percentage of annual sales occurring in each quarter (e.g., Q2 and Q3 will be highest for a garden company).

Cost Structure:

Direct Costs (COGS):

Bill of Materials (BOM): Cost per unit for raw materials (steel, aluminum, plastics, engines, batteries).

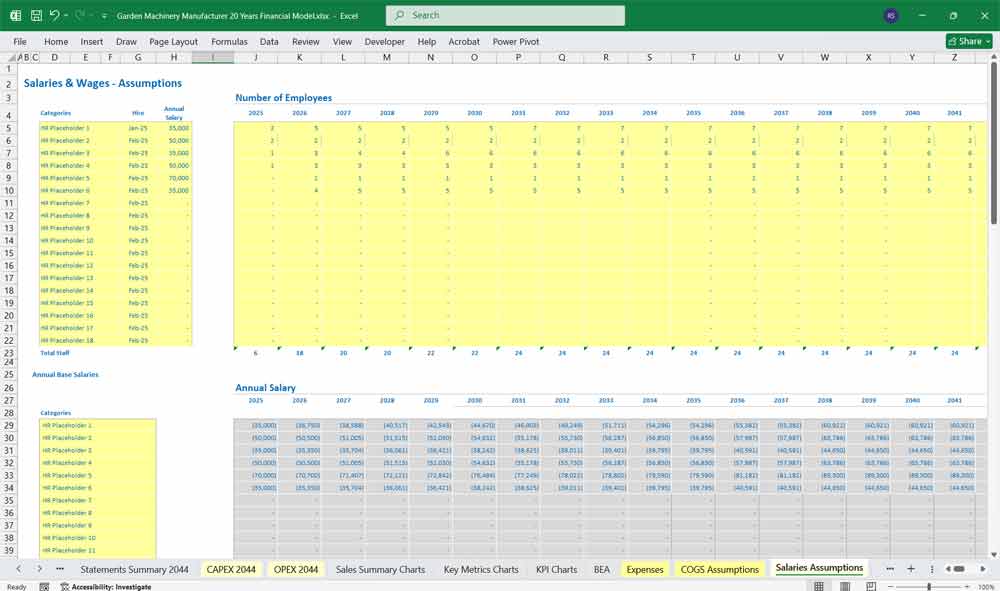

Direct Labor: Cost per hour * hours per unit.

Manufacturing Overhead: Allocation of utilities, factory rent, depreciation of manufacturing equipment.

Operating Expenses (OPEX):

R&D Expenses: % of revenue allocated to new product development.

Sales & Marketing: % of revenue or fixed budget for advertising, trade shows, commissions.

General & Administrative (G&A): Salaries for HQ staff, office rent, software, insurance, professional fees.

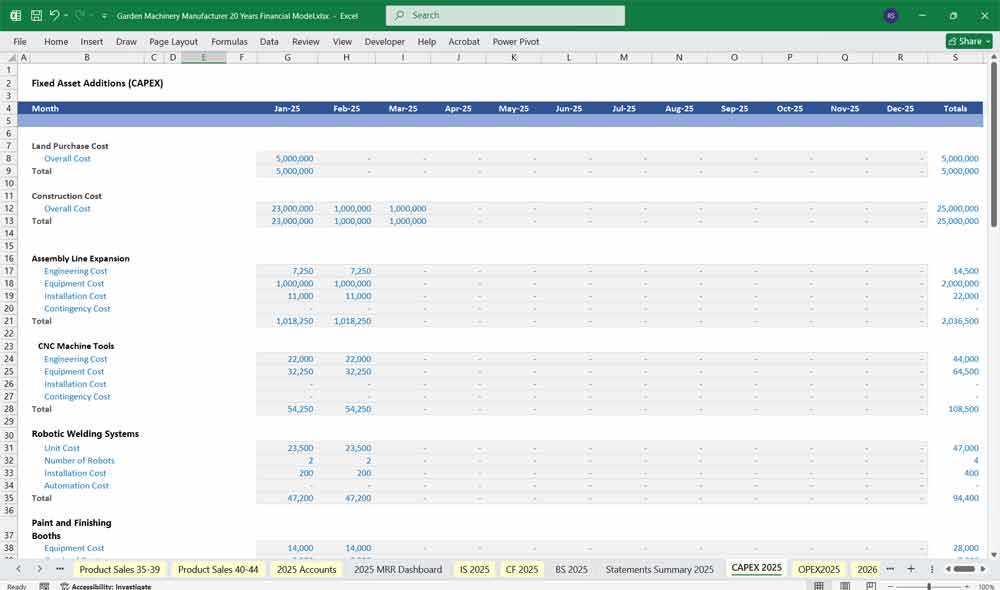

Capital Expenditures (CapEx):

Machinery & Equipment: Schedule for purchasing new manufacturing robots, stamping machines, assembly line upgrades.

Tooling & Molds: High-cost items for new product lines.

Vehicles: For delivery and service.

Working Capital:

Days Sales Outstanding (DSO): How many days it takes to collect payment from dealers (e.g., 45 days).

Days Inventory Outstanding (DIO): How many days of inventory are held on hand (e.g., 90 days). Critical for a manufacturer.

Days Payable Outstanding (DPO): How many days the company takes to pay its suppliers (e.g., 60 days).

Financing:

Debt: Existing loan terms (interest rate, maturity period), assumptions for new debt.

Equity: Any planned equity injections from owners or investors.

Dividend Policy: Will the company pay dividends? If so, how much?

Benefits Of a 20-Year Garden Machinery Model

A 20-year financial model offers an advantage in strategic planning, and provides a long-term roadmap for sustainable growth. For a garden machinery manufacturer, it forces management to look beyond annual budgets and consider multi-year product cycles, major capital investments in new manufacturing equipment, and the gradual expansion into new geographic markets. This long-view perspective is crucial for making informed decisions today that will shape the company’s competitive position and market share for decades to come.

Long-Term Garden Machinery CAPEX And Cash Flow Monitoring

This extended timeframe is vital for accurately assessing the feasibility of significant capital expenditures, such as building a new factory or developing a completely new product line, like electric autonomous mowers. The model helps determine if the projected long-term cash flows and profits from these major investments will justify their substantial upfront costs. It ensures the company does not jeopardize its financial stability by demonstrating how and when these large projects will eventually become profitable and generate a positive return.

Garden Machinery Long-Term Viability

Furthermore, a 20-year model is essential for sophisticated succession planning and ownership transition. Whether preparing for a future sale, merger, or passing the business to the next generation, this model provides a clear, data-driven valuation of the company based on its long-term earnings potential. It showcases the business’s future viability and growth trajectory to potential acquirers or heirs, and therefore making the transition smoother and more profitable for all stakeholders involved.

Long-Term Garden Machinery Manufacturing Financing Overview

Finally, this comprehensive model is a powerful asset for securing long-term financing and attracting strategic investors. Banks and private equity firms require a deep understanding of a company’s long-term prospects before committing substantial capital. A robust 20-year forecast demonstrates rigorous planning, a clear vision for the future, and a mature understanding of the market dynamics and financial discipline required to succeed over the long haul.

Final Notes on the Financial Model

This 20 Year Garden Machinery Financial Model must focus on balancing capital expenditures with steady revenue growth from diversified sales and services. By optimizing operational costs, and power efficiency, and maximizing high-margin services like parts and servicing, and even subscription offerings, the model ensures sustainable profitability and cash flow stability.

Download Link On Next Page