Ferroalloy Production Plant Financial Model

This 20-Year, 3-Statement Excel Ferroalloy Production Plant Financial Model includes revenue streams from Ferromanganese (FeMn), Ferrovanadium, and Ferroniobium, to Ferrosilicon (FeSi) sales, etc, cost structures, and financial statements to forecast the economic health of your Ferroalloy production.

20-Year Financial Model for a Ferroalloy production plant.

This very extensive 20 Year Ferroalloy Excel Model involves detailed revenue projections, cost structures, capital expenditures, and financing needs. This model provides a thorough understanding of the financial viability, profitability, and cash flow position of your manufacturing company. Includes: 20x Income Statements, Cash Flow Statements, Balance Sheets, CAPEX sheets, OPEX Sheets, Statement Summary Sheets, and Revenue Forecasting Charts with the revenue streams, BEA charts, sales summary charts, employee salary tabs and expenses sheets. Over 130 Spreadsheets in 1 Excel Workbook.

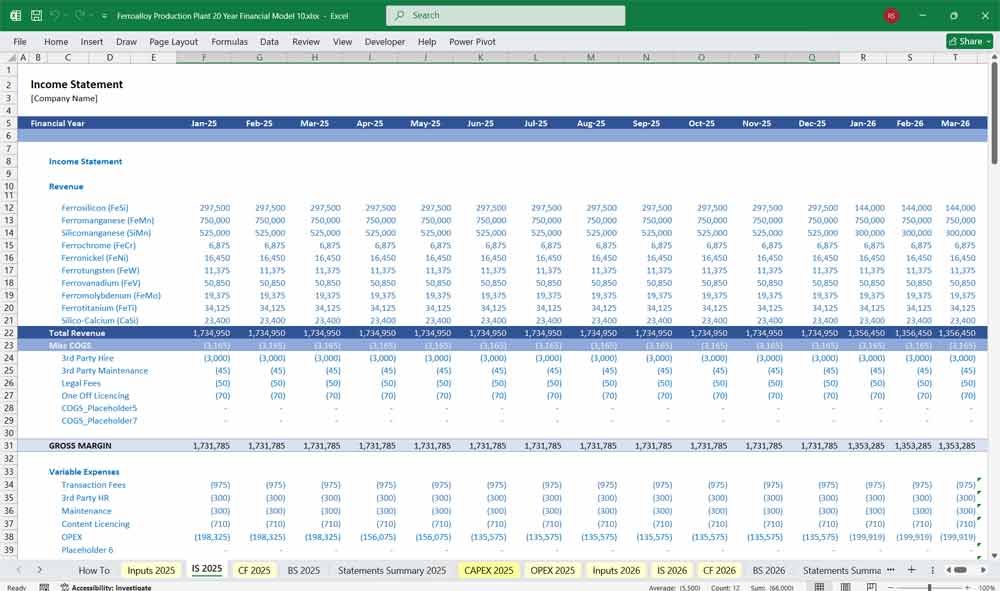

Income Statement

The Income Statement, also known as the Profit and Loss Statement, shows how the plant’s revenues are transformed into net profit. It is usually presented on an annual basis.

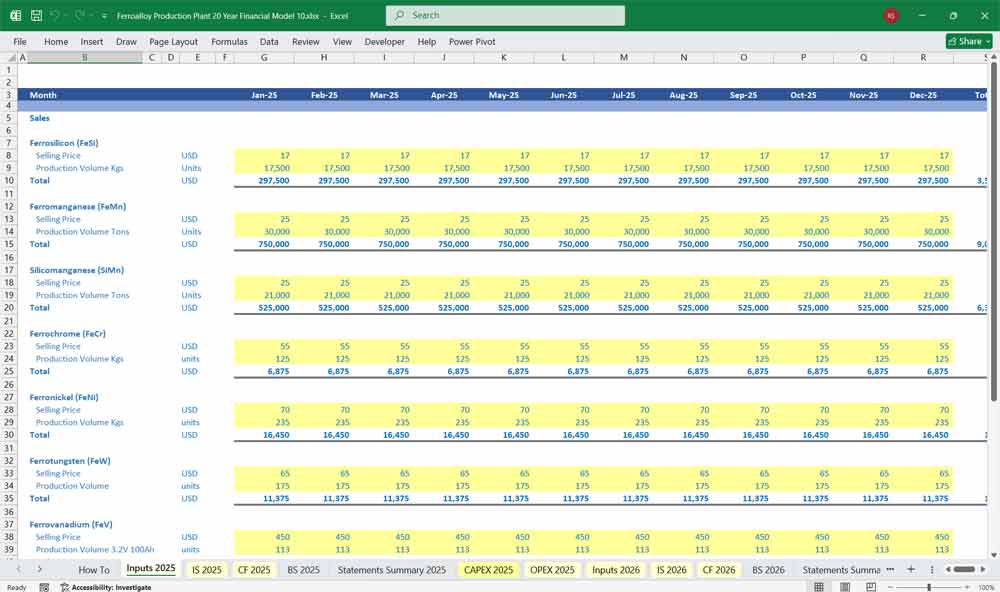

a. Revenue

Revenue is derived from the total volume of ferroalloy sold multiplied by its average selling price. Additional income may come from:

By-product sales (e.g., slag, waste heat recovery).

Scrap sales.

Miscellaneous operating income (e.g., interest from working capital deposits).

b. Cost of Goods Sold (COGS)

COGS includes all direct production costs:

Raw materials consumed, based on production volume and consumption ratios.

Power and fuel costs, determined by electricity usage and tariff.

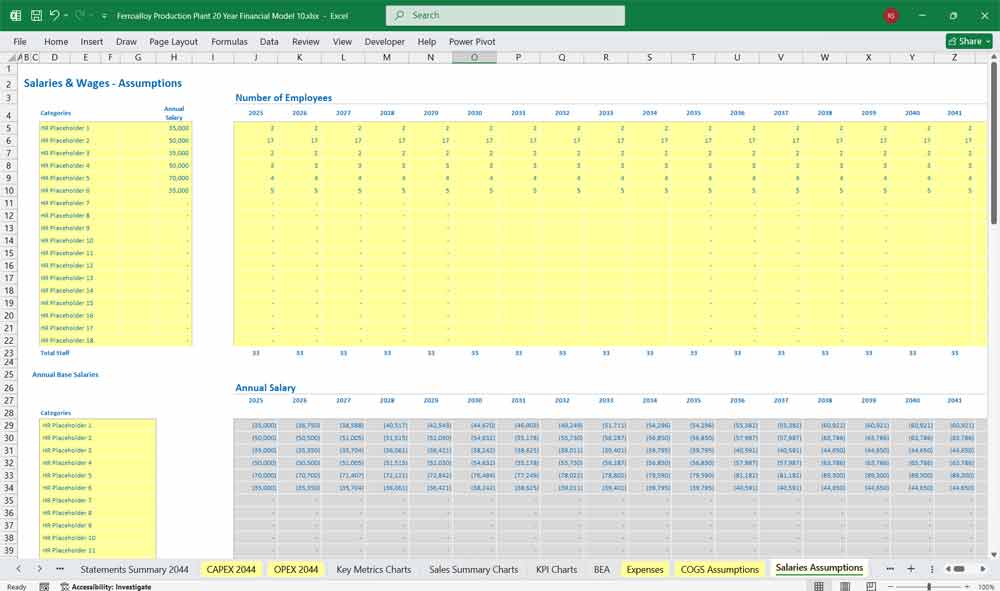

Direct labor.

Maintenance and consumable costs.

Factory overheads.

This yields Gross Profit, representing the margin from production activity.

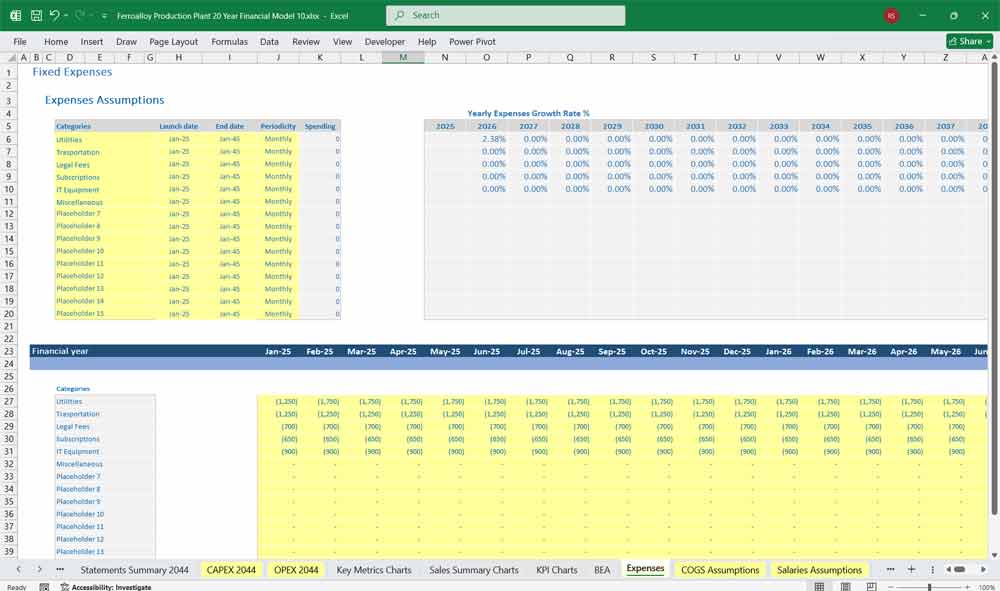

c. Operating Expenses

Operating expenses (OPEX) consist of:

Administrative and general expenses.

Salaries of management and support staff.

Selling, marketing, and distribution costs.

Research, quality control, and safety expenditures.

d. Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA)

EBITDA measures the plant’s operating performance before accounting for non-cash and financial costs.

e. Depreciation and Amortization

Depreciation represents the periodic allocation of capital costs over the asset’s useful life. It is non-cash but affects taxable profit.

f. Earnings Before Interest and Taxes (EBIT)

EBIT reflects the plant’s true operational profitability after accounting for asset wear and tear.

g. Interest Expense

Interest is computed from the debt schedule, which tracks principal outstanding, new drawdowns, and repayments.

h. Profit Before Tax (PBT)

Calculated as EBIT minus interest expense.

i. Tax Expense

Tax is determined based on statutory rates, adjusted for depreciation differences, carried-forward losses, and any tax holidays or credits.

j. Profit After Tax (PAT)

PAT, or net income, is the bottom line of the income statement. It represents the return available to shareholders.

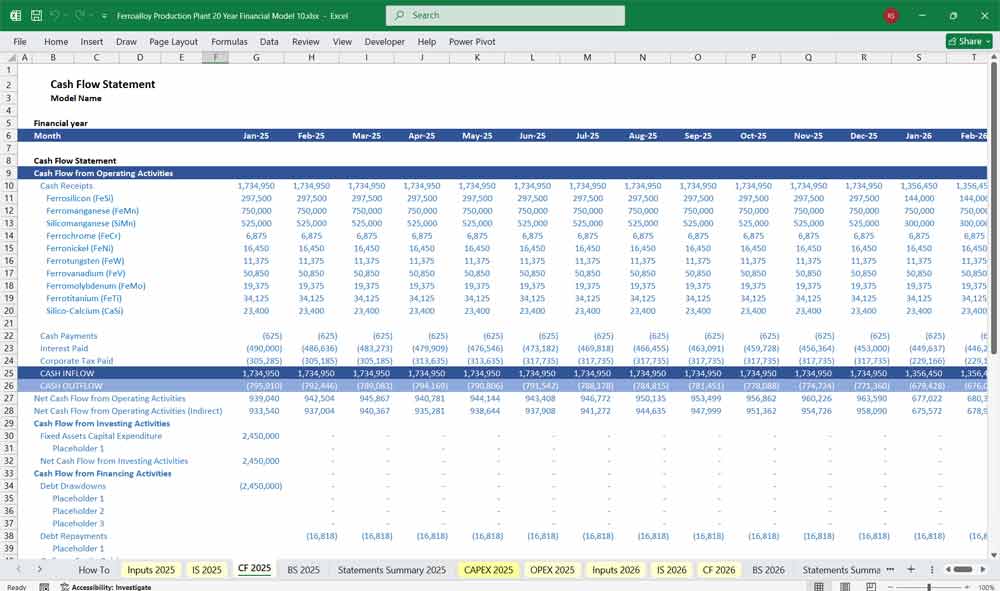

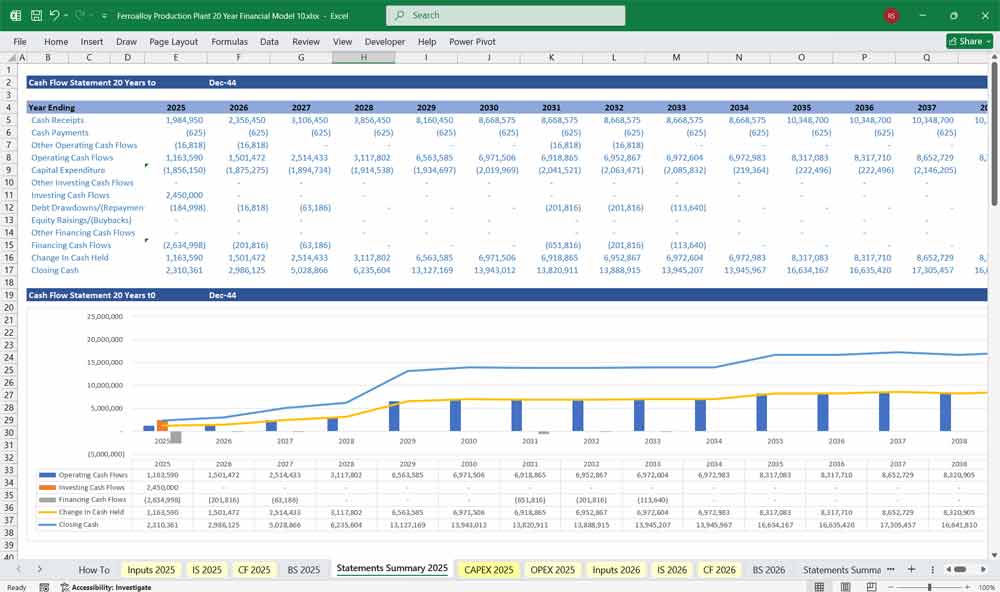

Ferroalloy Production Plant Cash Flow Statement

The Cash Flow Statement provides a view of how cash moves in and out of the business, classified into three main sections.

a. Cash Flow from Operating Activities (CFO)

Operating cash flow starts from net profit and adds back non-cash items such as depreciation. It adjusts for changes in:

Accounts receivable (customer payments outstanding),

Inventory (stock of raw materials and finished goods),

Accounts payable (supplier credits).

The result shows the net cash generated (or used) by regular business operations.

b. Cash Flow from Investing Activities (CFI)

Investing cash flows reflect capital expenditures and asset-related transactions:

Cash spent on acquiring new machinery or plant expansion.

Cash received from the sale of fixed assets or scrap.

Interest or dividends received from investments.

In the early years, this section is typically negative due to heavy capital spending during construction and commissioning.

c. Cash Flow from Financing Activities (CFF)

Financing cash flow records all movements related to capital structure:

Loan drawdowns during the construction or expansion phase.

Loan repayments as per the debt amortization schedule.

Interest payments to lenders.

Equity infusions from shareholders.

Dividend payments to shareholders (once the project generates profit).

The sum of all three sections gives the net change in cash balance, which reconciles the opening and closing cash positions each year.

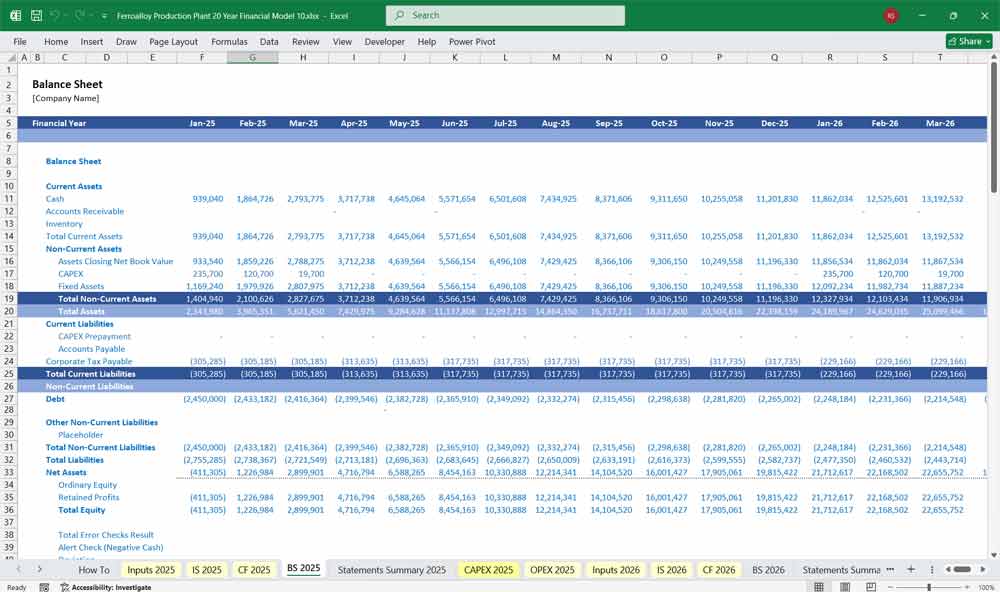

Ferroalloy Production Plant Balance Sheet

The Balance Sheet shows the company’s financial position at a specific point in time, summarizing what it owns (assets), what it owes (liabilities), and the residual interest (equity).

a. Assets

Non-current assets include:

Tangible assets: land, buildings, plant, and equipment, shown at cost less accumulated depreciation.

Intangible assets: licenses, technology, or goodwill.

Long-term deposits and deferred tax assets.

Current assets include:

Inventory of raw materials, work-in-progress, and finished goods.

Accounts receivable (customer balances).

Cash and bank balances.

Other short-term advances and prepayments.

b. Liabilities

Current liabilities include:

Trade payables and accrued expenses.

Short-term loans and working capital borrowings.

Current portion of long-term debt due within one year.

Non-current liabilities include:

Long-term debt and lease obligations.

Deferred tax liabilities (if temporary differences exist).

c. Equity

Equity consists of:

Paid-in capital from shareholders.

Retained earnings, which accumulate profits not distributed as dividends.

Reserves and surplus, including revaluation or capital reserves.

The Balance Sheet equation must always hold true:

Assets = Liabilities + Equity.

Assumptions and Input Framework For Ferroalloy Production

All calculations in the model are driven by a set of clearly defined assumptions, which can be grouped as follows:

a. Production and Capacity

The plant’s designed capacity

The relationship between raw material input and final product output.

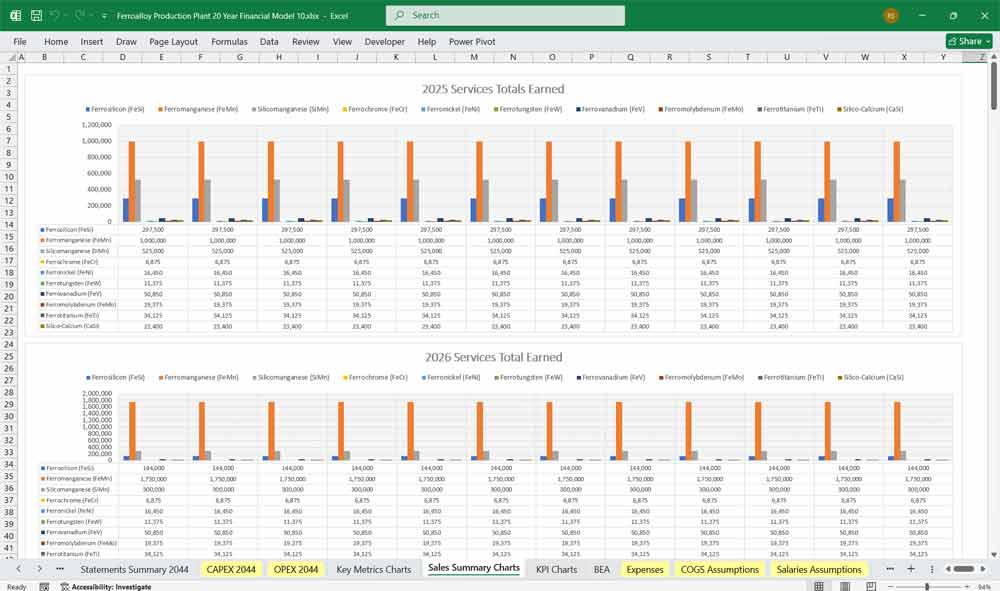

The mix of ferroalloy types — for instance, ferrochrome, ferromanganese, or ferrosilicon — is defined as percentages of total production.

b. Raw Materials and Consumables

The model includes the specific consumption rates of each raw material (e.g., kilograms of manganese ore, coke, quartz, or flux per ton of alloy).

Unit purchase costs and escalation factors reflect expected market trends.

Freight, handling, and import duties are included as additional cost components.

c. Power and Utilities

Electricity consumption (measured in kWh per ton of alloy) is one of the largest cost elements.

The power tariff and annual escalation rate are key assumptions.

Other utilities — water, oxygen, nitrogen, maintenance materials, and refractories — are included based on consumption norms.

d. Labor and Overheads

Direct and indirect labor costs are modeled separately.

Administrative overheads include office expenses, insurance, training, and maintenance contracts.

e. Sales and Pricing

The selling price for each alloy type is based on international market benchmarks or local prices.

Sales volumes are adjusted for scrap, rejects, and losses.

Revenue also includes by-products such as slag, dust, or recovered metals.

Selling expenses and logistics costs (e.g., transport to port or buyer) are accounted for separately.

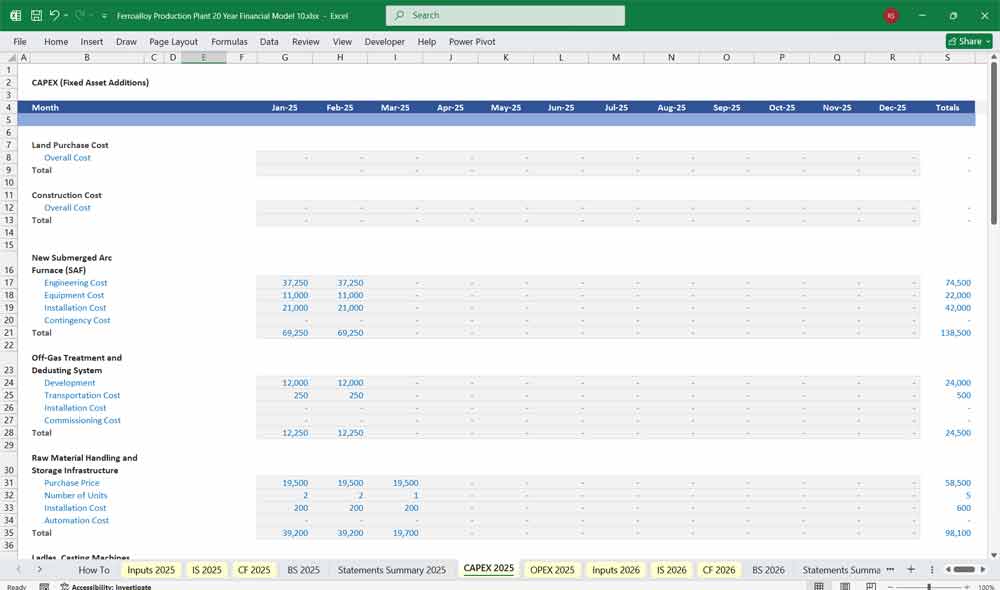

f. Capital Expenditure (CapEx)

Initial investment includes cost of land, civil works, machinery, electrical systems, and auxiliary infrastructure.

Preoperative expenses (consulting, engineering, interest during construction) are capitalized.

Contingency allowances (typically 10–15%) cover cost overruns.

Depreciation is calculated based on asset categories and useful life.

g. Financing and Taxation

The financing structure (debt-to-equity ratio) determines interest and repayment obligations.

Loan terms define interest rate, grace period, and tenure.

Tax parameters include corporate tax rates, depreciation allowances, and potential tax holidays.

Supporting Schedules

To make the statements internally consistent, several supporting schedules are maintained:

Fixed Asset and Depreciation Schedule – tracks the movement and depreciation of each asset class.

Debt Schedule – details drawdowns, interest, and repayments over the loan term.

Working Capital Schedule – projects inventory, receivables, and payables based on turnover ratios.

Tax Schedule – reconciles accounting and taxable profits.

CapEx Schedule – outlines project and expansion expenditures.

Equity Schedule – shows paid-up capital, retained earnings, and dividend distributions.

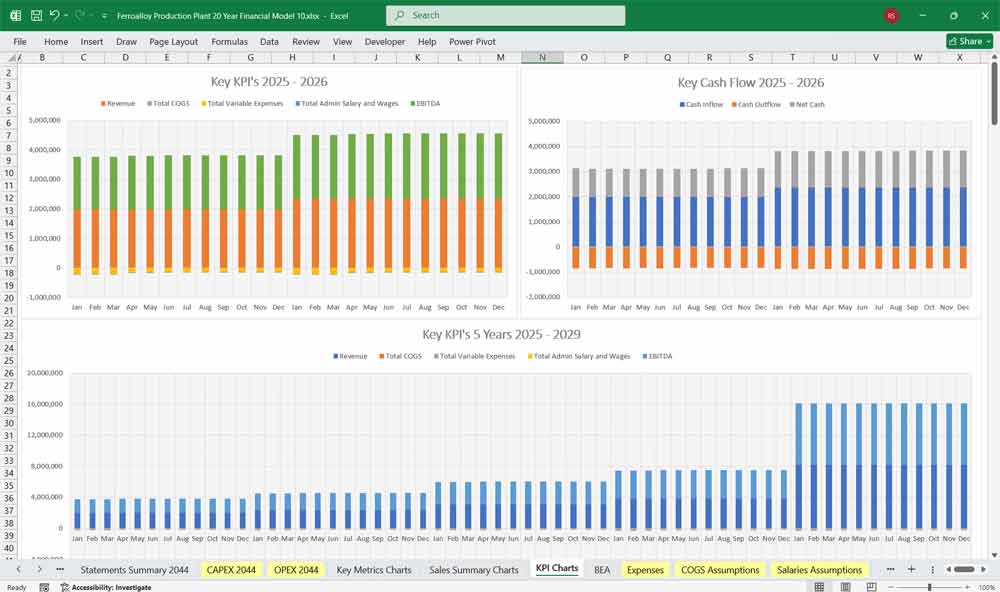

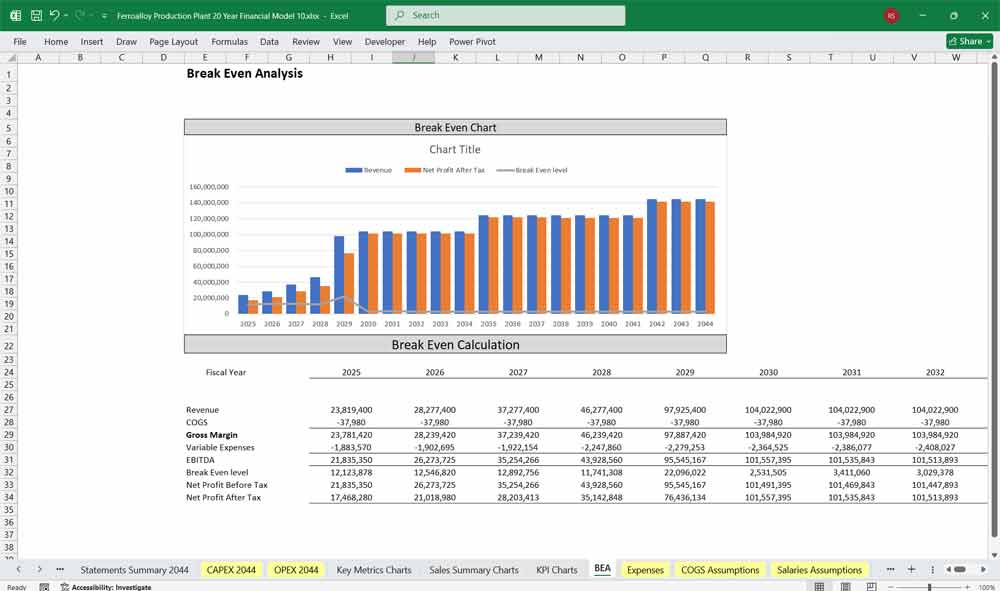

Key Financial Indicators

The model concludes with a summary of key performance and return metrics, including:

Gross Margin and EBITDA Margin

Net Profit Margin

Debt Service Coverage Ratio (DSCR)

Return on Equity (ROE) and Return on Assets (ROA)

Net Present Value (NPV) and Internal Rate of Return (IRR) for the project

Payback Period and Break-even Capacity Utilization

Interpretation and Use

This 20-year model allows stakeholders — investors, lenders, and management — to test how changes in market conditions (such as ore prices, electricity tariffs, or alloy selling prices) affect profitability and cash flow. Sensitivity and scenario analyses can be used to measure project resilience.

Final Notes on the Financial Model

This 20 Year Ferroalloy Production Plant Financial Model focuses on balancing capital expenditures with steady revenue growth from a diversified product line. By optimizing operational costs, and power efficiency, and maximizing high-margin services, the models ensure sustainable profitability and cash flow stability.

Download Link On Next Page