Green Hydrogen Desalination DCF Financial Model Template

DCF Financial Model for Desalination To Green Hydrogen

This Discounted Cash Flow (DCF) Financial Model for a Desalination to Green Hydrogen Plant is a comprehensive financial planning and valuation tool used to evaluate the economic feasibility and long-term profitability of an integrated hydrogen production facility that utilizes desalinated seawater and renewable electricity to produce green hydrogen.

The model forecasts the project’s financial performance over its 20-year lifecycle, including construction, commissioning, and operational phases. By projecting revenues, costs, capital expenditures, financing structures, and working capital requirements, the model calculates the present value of the project’s expected cash flows using a discount rate that reflects project risk and capital costs.

Revenue Model

Revenue in the model is primarily generated from hydrogen sales, though additional income streams may also be included.

Hydrogen Sales

Revenue is calculated using:

Hydrogen Production × Hydrogen Selling Price

Hydrogen prices may be based on:

Long-term offtake agreements

Market-based hydrogen price forecasts

Indexed pricing structures

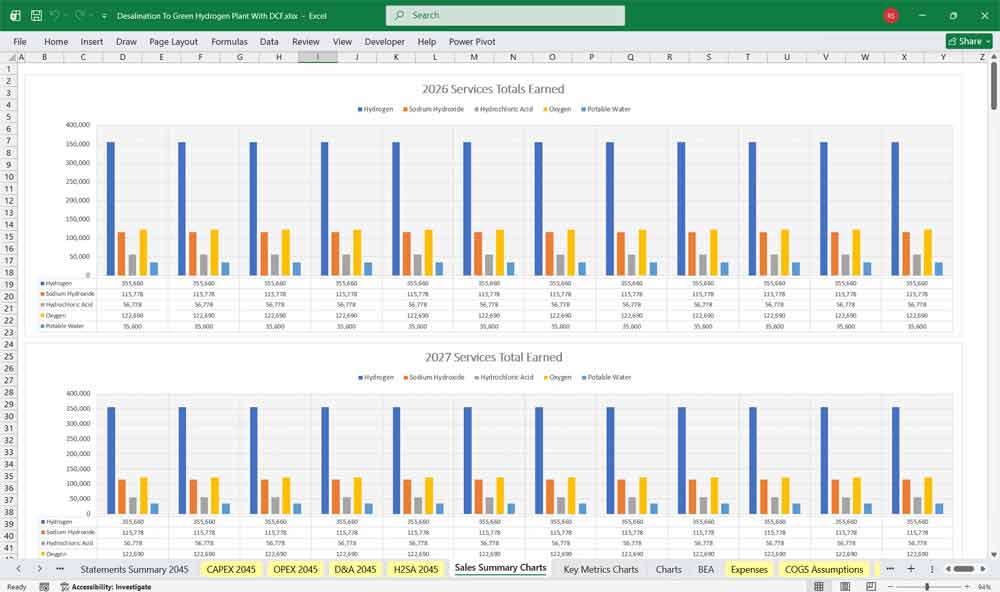

Additional Revenue Streams

Depending on the project design, the model may include:

Oxygen byproduct sales

Carbon credits

Renewable energy certificates

Government subsidies or production tax credits

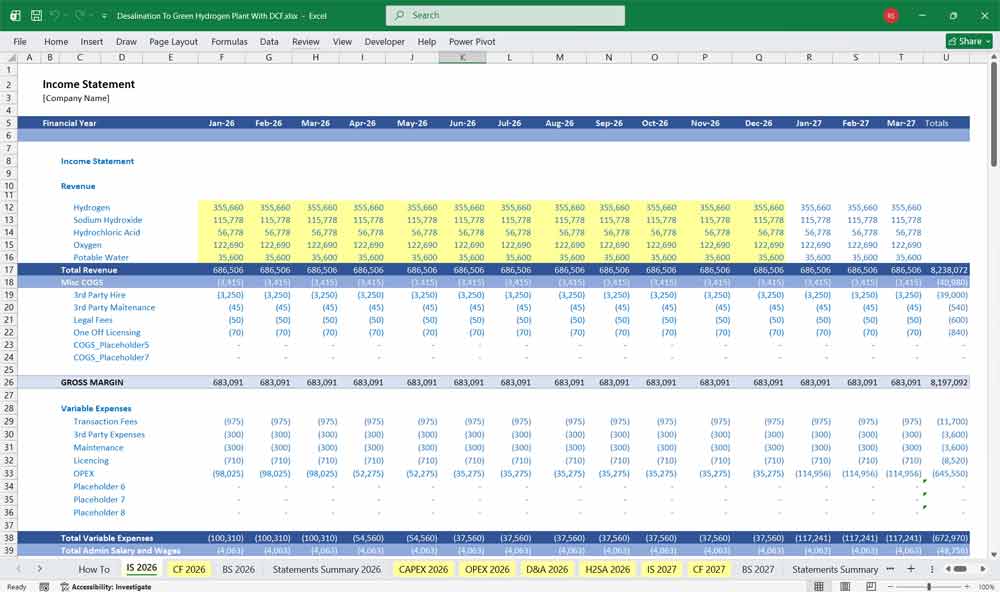

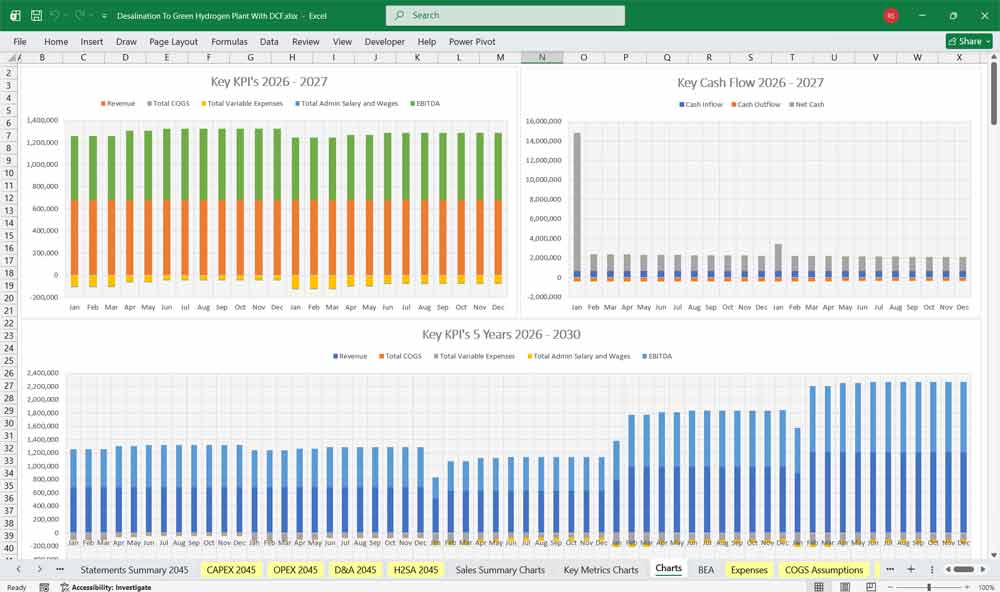

Income Statement

The Income Statement presents the operational profitability of the hydrogen plant over time.

Revenue

Total revenue is driven primarily by hydrogen sales.

Components include:

Hydrogen production volumes

Contracted hydrogen price

Additional revenue streams

Annual revenue is calculated based on projected production volumes and price escalation assumptions.

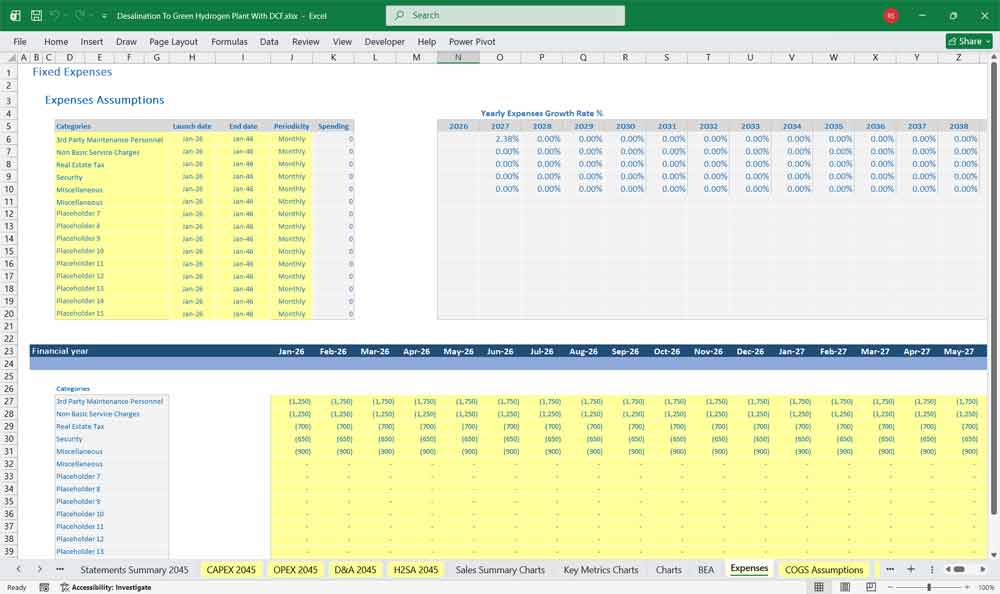

Operating Expenses (OPEX)

Operating costs include both variable and fixed expenses associated with plant operations.

Electricity Costs

Electricity represents the largest operating cost in most green hydrogen projects.

Costs include:

Electricity for electrolysis

Electricity for desalination

Electricity for hydrogen compression and storage

Electricity may be sourced from:

Dedicated renewable energy assets

Grid electricity

Power purchase agreements (PPAs)

Water and Desalination Costs

Water-related costs include:

Seawater intake

Reverse osmosis desalination

Water purification

Brine disposal

Energy consumption for desalination is also included in electricity costs.

Maintenance and Operations

Maintenance costs include:

Electrolyzer maintenance

Stack replacements

Mechanical and electrical maintenance

Spare parts

Labor and Administrative Costs

Personnel expenses include:

Plant operators

Engineers

Maintenance staff

Management and administration

Additional costs include insurance, regulatory compliance, and monitoring systems.

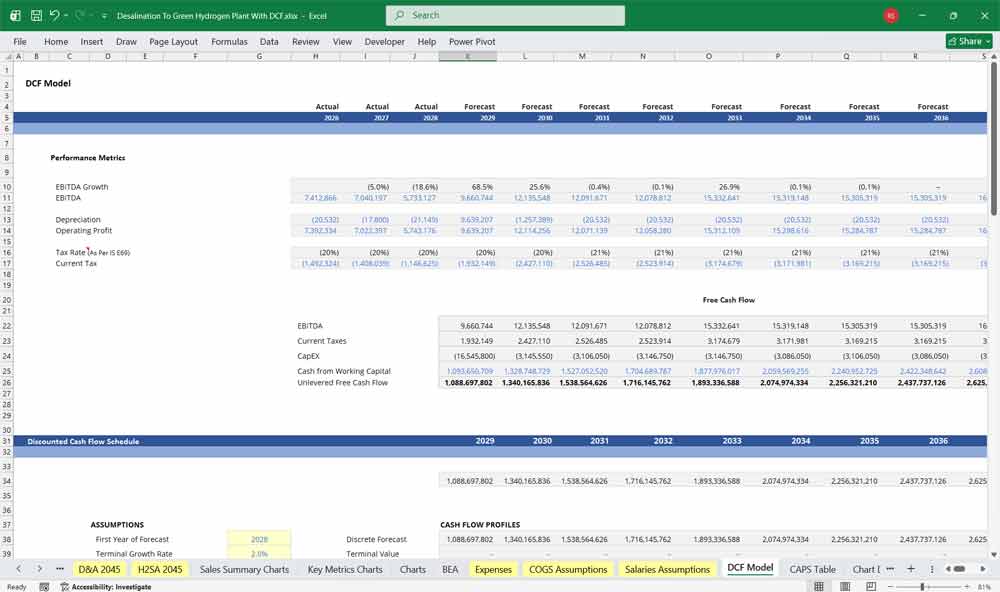

EBITDA

EBITDA represents the project’s operational earnings before depreciation, interest, and taxes.

EBITDA =

Revenue − Operating Expenses

This metric measures operational performance independent of financing and accounting adjustments.

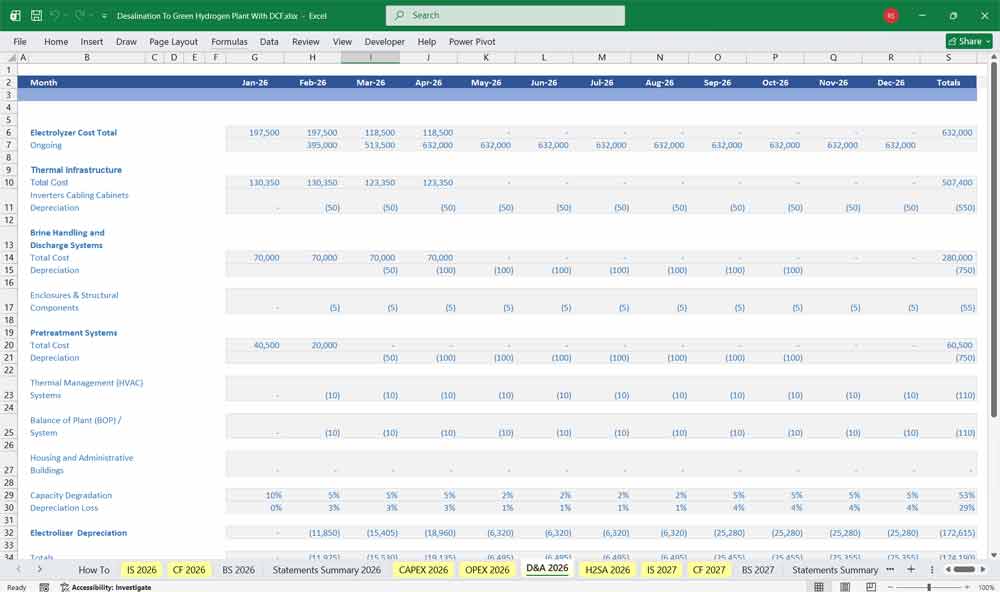

Depreciation

Capital investments in the hydrogen facility are depreciated over the useful life of the assets.

Typical asset lifetimes include:

Electrolyzers: 10–15 years

Desalination plant: 20–25 years

Compression and storage systems: 20 years

Infrastructure: 25–30 years

Depreciation may follow:

Straight-line depreciation

Tax depreciation schedules

EBIT

EBIT (Earnings Before Interest and Taxes) is calculated as:

EBIT = EBITDA − Depreciation

This reflects the plant’s operating profitability after accounting for asset wear and tear.

Interest Expense

Interest expenses are derived from the project’s financing structure, which may include:

Senior project debt

Construction loans

Green bonds

Infrastructure financing

Interest during construction is often capitalized as Interest During Construction (IDC).

Taxes

Corporate income taxes are calculated based on taxable income after accounting for:

Depreciation tax shields

Interest deductibility

Tax loss carryforwards

Government incentives

Net Income

Net income represents the final profit available to equity investors after all expenses.

Net Income =

EBIT − Interest − Taxes

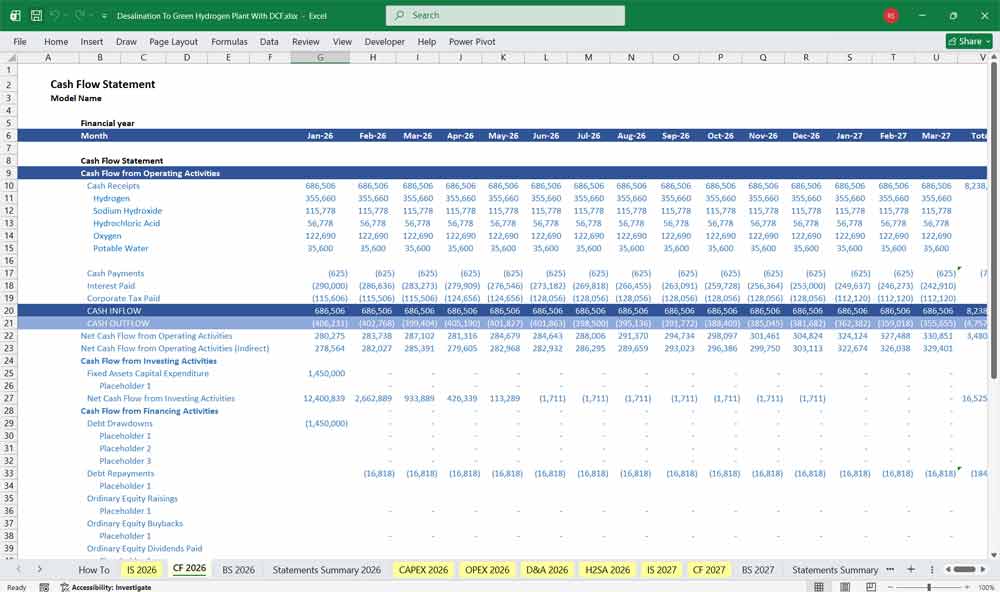

Desalination To Green Hydrogen Plant Cash Flow Statement

The Cash Flow Statement tracks the actual movement of cash into and out of the project company.

It is divided into three sections:

Operating Cash Flow

Investing Cash Flow

Financing Cash Flow

Operating Cash Flow

Operating cash flow reflects cash generated from plant operations.

It is calculated as:

Net Income

Depreciation

− Changes in Working Capital

Working capital components may include:

Accounts receivable from hydrogen buyers

Inventory (stored hydrogen)

Accounts payable to suppliers

Investing Cash Flow

Investing cash flow captures capital expenditures related to the project.

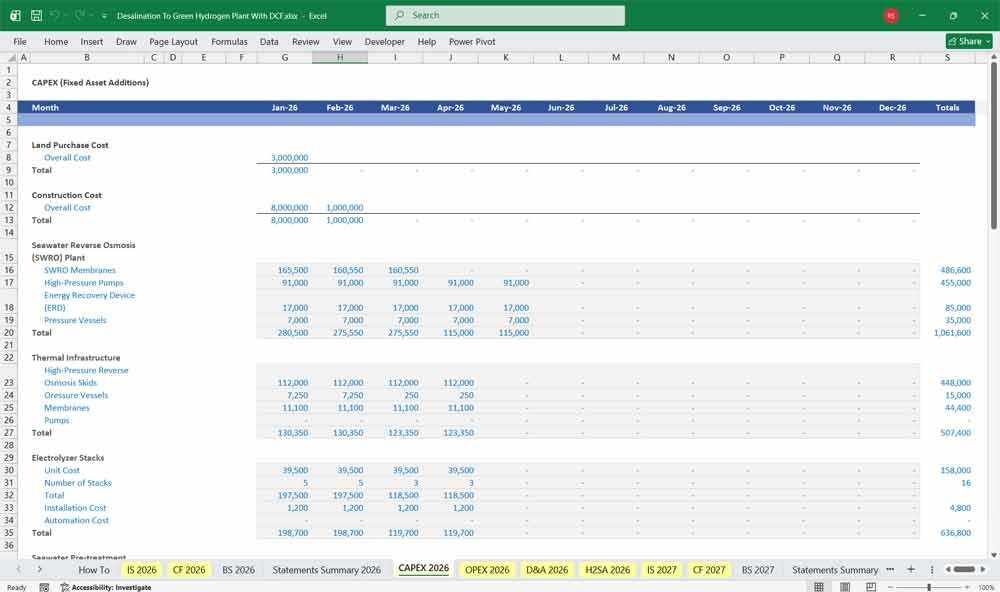

Construction CAPEX

Major capital investments include:

Electrolyzer systems

Desalination plant

Hydrogen compression systems

Storage tanks

Pipelines and export infrastructure

Balance-of-plant equipment

CAPEX is typically distributed over the construction period according to a development schedule.

Replacement CAPEX

Electrolyzer stacks typically require replacement every 7–10 years, which is modeled as periodic replacement capital expenditure.

Financing Cash Flow

Financing cash flows reflect how the project is funded and how capital is returned to investors.

Debt Drawdowns

During construction, debt is drawn to finance capital expenditures.

Debt Service

During operations, the project repays debt through:

Principal repayments

Interest payments

Equity Contributions

Equity investors contribute capital to finance construction costs and maintain target leverage ratios.

Dividend Distributions

After meeting debt service requirements and reserve accounts, excess cash may be distributed to equity investors as dividends.

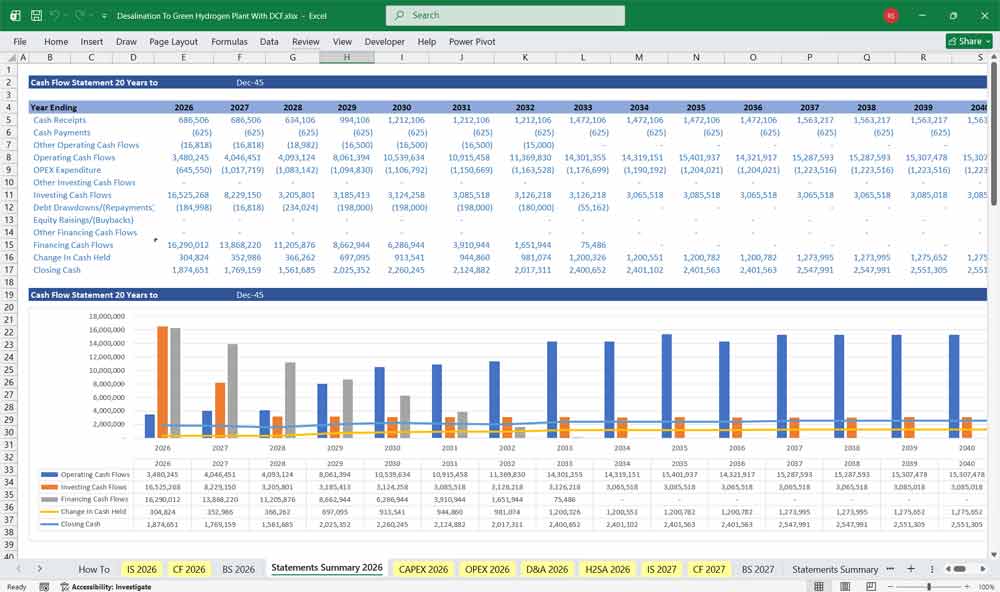

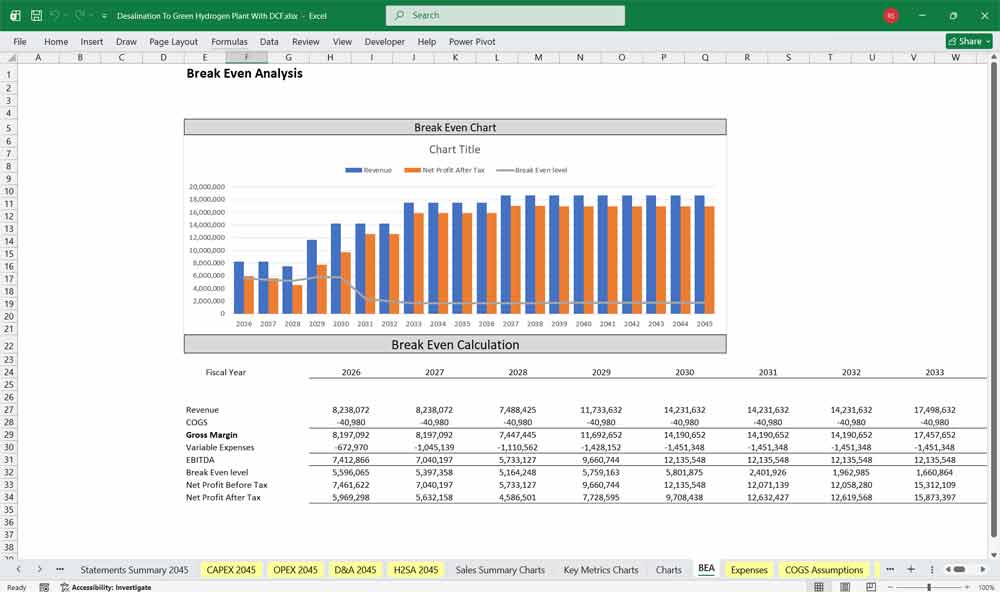

Free Cash Flow

The DCF model calculates free cash flow, which forms the basis for valuation.

Free Cash Flow to Firm (FCFF):

Operating Cash Flow − Capital Expenditures

These cash flows are discounted to present value using the project’s Weighted Average Cost of Capital (WACC).

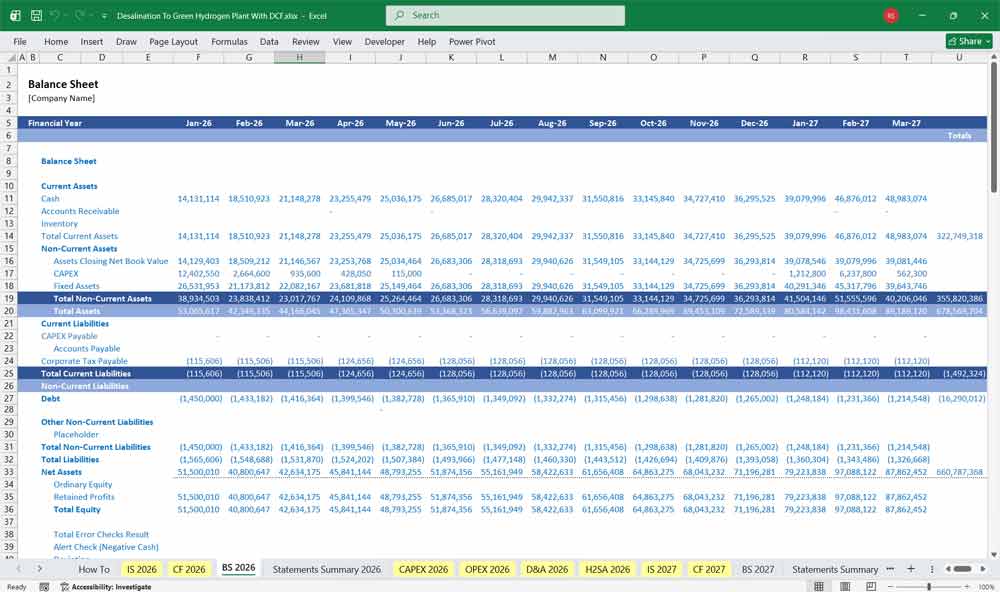

Desalination To Green Hydrogen Plant Balance Sheet

The Balance Sheet provides a snapshot of the project company’s financial position over time.

Assets

Fixed Assets

Fixed assets represent the capital investments in the hydrogen production facility.

These include:

Electrolyzers

Desalination plant

Hydrogen compression systems

Storage infrastructure

Power integration equipment

Buildings and land improvements

Net fixed assets are calculated as:

Gross Assets − Accumulated Depreciation

Current Assets

Current assets include:

Cash balances

Accounts receivable

Hydrogen inventory

Prepaid expenses

Liabilities

Long-Term Debt

Long-term liabilities include project financing instruments such as:

Senior project loans

Infrastructure debt

Green bonds

Debt balances decrease over time through scheduled principal repayments.

Current Liabilities

Short-term obligations include:

Accounts payable

Accrued operating expenses

Short-term portions of long-term debt

Equity

Equity represents the ownership interest in the project company.

Equity components include:

Initial equity contributions

Retained earnings

Additional equity injections

Dividend distributions

Balance Sheet Identity

The balance sheet ensures that:

Assets = Liabilities + Equity

This accounting identity ensures the financial integrity of the model.

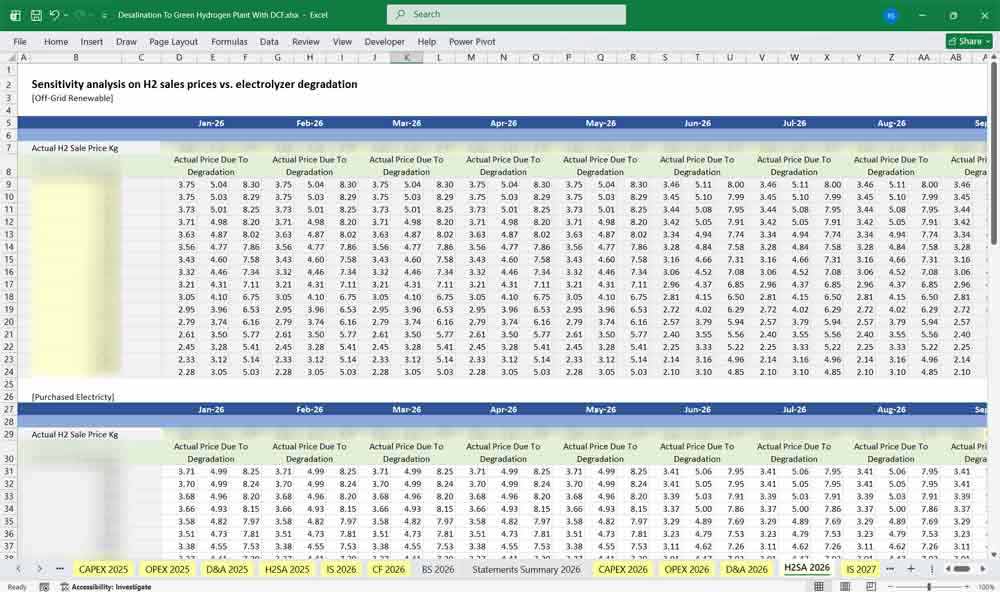

Desalination To Hydrogen Plant Sensitivity analysis on power prices vs. electrolyzer unit degradation

Sensitivity analysis in a desalination-to-green-hydrogen financial model is used to evaluate how changes in key technical and economic variables impact project profitability and cost of hydrogen production. Two of the most critical drivers are power prices and electrolyzer unit degradation, as electricity is typically the largest operating cost while electrolyzer efficiency directly affects hydrogen output. By varying these inputs within realistic ranges, the model can identify how sensitive metrics such as Net Present Value (NPV), Internal Rate of Return (IRR), and Levelized Cost of Hydrogen (LCOH) are to operational conditions.

Desalination To Hydrogen Plant Economics

Changes in power prices have a substantial impact on project economics because electrolysis requires significant electricity consumption. In a desalination-based hydrogen plant, electricity costs also include energy used for seawater desalination, purification, compression, and hydrogen storage. Sensitivity analysis often tests scenarios where electricity prices increase or decrease by a defined percentage (for example ±10–30%). Higher power prices significantly increase operating costs and the LCOH, potentially reducing project margins, while lower renewable electricity costs improve profitability and project competitiveness.

Desalination To Hydrogen Plant Electrolyzer Efficiency

Electrolyzer unit degradation represents the gradual decline in electrolyzer efficiency and hydrogen production capacity over time. As degradation increases, the electrolyzer requires more electricity to produce the same quantity of hydrogen, raising energy costs per kilogram of hydrogen. Sensitivity analysis typically models different degradation rates and replacement cycles for electrolyzer stacks. When degradation occurs faster than expected, hydrogen output declines and operating costs rise, negatively affecting cash flows and valuation metrics. Understanding the combined impact of power price volatility and electrolyzer degradation he

Valuing Your Desalination To Green Hydrogen Plant With A DCF

This Discounted Cash Flow (DCF) analysis is a core valuation method used to assess the economic viability of a desalination to green hydrogen plant. The DCF model estimates the present value of future cash flows generated by the project over its typical operational life, of 20 years. These cash flows are driven by hydrogen production volumes, hydrogen sales prices, electricity costs, desalination operating costs, and capital expenditures. By discounting projected free cash flows back to their present value, the DCF model allows investors and developers to determine whether the project generates sufficient returns relative to its initial investment.

Desal To H2O WACC

The Weighted Average Cost of Capital (WACC) represents the discount rate used in the DCF model and reflects the blended cost of financing from both debt and equity. In hydrogen infrastructure projects, WACC incorporates factors such as project risk, financing structure, interest rates on debt, and required returns from equity investors. Because desalination-to-hydrogen facilities involve large upfront capital investments in electrolyzers, desalination units, and supporting infrastructure, the cost of capital plays a significant role in determining project valuation. A lower WACC increases the present value of future cash flows and improves project economics, while a higher WACC reduces the overall project value.

Desalination To Green Hydrogen Plant Electrolyzer Analysis

Sensitivity analysis is used alongside the DCF model to evaluate how changes in key assumptions affect project returns. For a desalination to green hydrogen plant, important variables include electricity prices, hydrogen market prices, electrolyzer efficiency, plant capacity factor, and capital costs. By testing different scenarios and adjusting these inputs, developers can understand which variables have the greatest impact on Net Present Value (NPV) and Internal Rate of Return (IRR). This analysis helps identify key risks, supports investment decisions, and improves strategic planning for long-term hydrogen project development.

Final Notes On The DCF Financial Model

The model allows users to test how changes in key assumptions impact project returns.

Hydrogen selling price.

Electricity price.

Electrolyzer efficiency.

- Capacity factors

- Financing terms.

This 20-Year Desalination To Green Hydrogen Plant Financial Model helps to focus on balancing capital expenditures with steady revenue growth from diversified distribution services. By optimizing operational costs, power efficiency, and maximizing high-margin services, the model ensures sustainable profitability and cash flow stability.